Romania ratings: No time to become complacent

Ahead of scheduled rating reviews this week and next, we provide an update on our views for the sovereign rating and address the near- and medium-term challenges coming from politics, rising external deficits and EU fund absorption. We believe that recent political jitters won't have a long-lasting impact on the leu and expect EUR/RON stability from here

Reconfirming our growth forecasts but political turmoil comes at a bad time

Following a stellar year-end, with the economy expanding by 4.8% in 4Q20 vs 3Q20, a slowdown was to be expected in the first quarter of 2021. The limited high frequency data we have so far for 1Q21 points to small but still positive sequential growth. This could have been driven by the still-expansionary fiscal stance, with the budget gap already reaching 1.14% of GDP after two months of 2021, likely fuelling public consumption and possibly investment.

We maintain our above-consensus GDP growth forecast of 5.5% in 2021, although the restrictions which came with the third wave of coronavirus infections were not fully factored into our base case back in February when we upgraded our forecast. At that time, we were anticipating a stricter enforcement of the existing measures rather than additional ones. In addition, the recent political turmoil does not look negligible but the dynamics and any resolutions will likely be better reflected in the financial markets rather than in the real economy.

The firing of the health minister by the premier sparked a political clash between the two main coalition partners, PNL and USR-PLUS. The developments certainly came at an unfortunate time, just ahead of the rating reviews this and next Friday. The importance of the political stability post-December elections was a topic that agencies have underlined, mostly in relation to the much-needed budget consolidation process and the medium-term fiscal planning in general. The events pose a setback and might lead to some policy delays, but we do not anticipate a coalition breakdown.

External deficit starts to be troublesome

Although at heart, Romania’s main issues revolve around fiscal consolidation, we are turning more anxious about Romania’s external imbalances. Both the trade deficit and the current account deficit have expanded in 2020 – a year of economic contraction! – and the first months of 2021 do not look any better. While we generally accept the idea that the fiscal deficit is mainly to blame for the external one, we believe that fundamental competitiveness issues are also starting to surface.

In the short-to-medium term, we are not necessarily concerned regarding the financing side of the C/A deficit due to better prospects for FDIs and, crucially, inflows from the Next Generation EU Fund. It is the structural nature of the C/A deficit that could give rise to concern - and 2020 developments certainly have not helped. Add on top, the prospects for another year of a relatively overvalued leu and the odds for the C/A deficit to rebalance remain rather distant.

Current account deficit is far from correcting

Investment prospects dependent on EU funds

Particularly constrained by the high share of rigid spending over the past few years, Romania's 2021 budget plans incorporate a 15.8% increase in investment spending, to take the investment-to-GDP ratio to around 5.5% - a new historic high. The multi-annual investment proposals focus on improved EU funds absorption which is seen as ‘a central element of budget sustainability’. While a focus on EU funds is certainly welcome, the projections underline a relatively high dependence on EU money for Romania’s investment projects (which are also needed -at least partly- for balancing the current account). It also suggests that if projected EU-financed investments do not materialise, the country could swiftly move from historic highs to historic lows in terms of the investment-to-GDP ratio.

Scheduled public investments 2021-2024

Ratings: No time to become complacent

Only six months ago, fears of a more imminent downgrade were at the peak, with a looming 40% pension hike and election uncertainties posing further downside risks in addition to the Covid-19 impact on the economy and public finances. Rating agencies however chose to look through the political cycle and the above-mentioned risks were largely averted. Moreover, the 2021 budget, while not overly ambitious, should sufficiently please the rating agencies as it indicates a medium-term fiscal consolidation towards a budget deficit below 3% of GDP by 2024. Lastly, with the pandemic weakening fundamentals globally, Romania’s public debt has held up relatively well.

Comparison of ING, IMF and rating agency forecasts

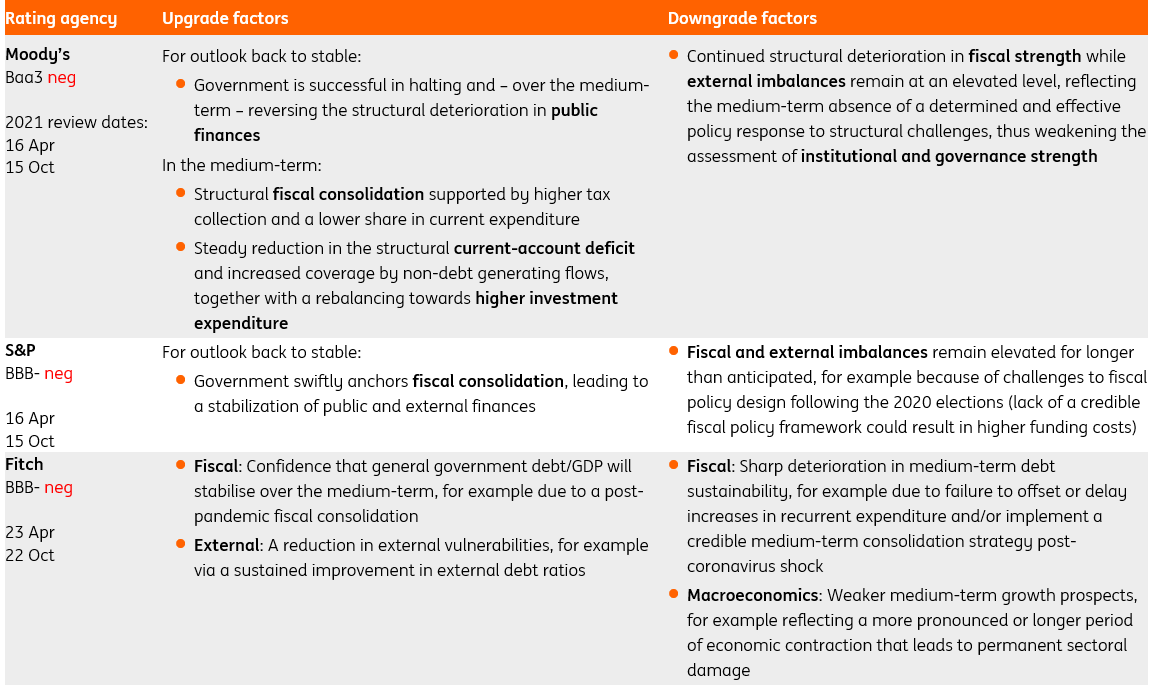

In 2021, rating event risk is clustered around the review dates in April and October, with time frames for the resolution of the negative outlooks largely coming to a close and views across rating agencies closely aligned (see table below). This leaves three options, those being (1) a downgrade, (2) a change in the outlook, or (3) new triggers that warrant the negative outlook to remain in place. Recent developments have averted imminent downgrade pressure in April. However, unaddressed risks, notably regarding the medium-term fiscal consolidation and a widening C/A deficit, as well as lingering political uncertainties mean that we shouldn’t become too comfortable with an outlook stabilisation in October just yet.

Going forward, budget execution and more details on how to address social spending rigidities will be in focus. We also believe that the Next Generation EU recovery fund and the EU budget will be key, with absorption serving as a test for institutional effectiveness but also mitigating external financing risks and providing upside risks to medium-term growth. Meanwhile, the viability of the coalition government will remain in focus given the need for policy momentum and tough political choices.

All in all, our base case is for Moody’s and S&P to revise the outlook back to stable as their time frames end by October. Meanwhile, we believe that Fitch could well make use of a two-year horizon, meaning that we might only see a decision by early 2022. Below, we provide a summary and our view for each rating agency:

- Moody’s revised the outlook on the Baa3 rating to negative a year ago due to the structural deterioration in public finances and increased susceptibility to event risk from a worsening external balance sheet. In the press release then, Moody’s said that it plans to resolve the negative outlook within 12-18 months absent further severe shocks. This means that we should see a rating action either this week or in six months’ time. Our base case is for Moody’s to revise the outlook back to stable on the 15 October review date. In our opinion, a credible budget (Moody’s said the government’s stance appears “measured”) and consistent policy communication to stakeholders go some way in returning the outlook back to stable. However, uncertainties regarding spending rigidities (notably from public pensions and wages), public sector reforms and EU fund absorption capacity (including NextGen EU) remain. Meanwhile, the political backdrop remains challenging owing to the government’s small majority in parliament and a low voter turnout in December. The next six months therefore could provide some more evidence. We also note that Moody’s forecast on government debt/GDP appears relatively optimistic (with a peak at 51% in 2021 before declining below 50% in 2022).

- S&P’s negative outlook, in place since December 2019, reflects risks to the fiscal and external balances which would likely materialise if policymakers fail to produce a credible plan to tackle the imbalances. The rating agency is looking to resolve the negative outlook this year absent of any new triggers, and we thus expect an outlook revision back to stable on 15 October (ie, for this Friday, we expect a rating affirmation with the negative outlook remaining in place). Positively, downside risks late last year did not materialise, and the focus therefore has shifted back to the medium-term fiscal outlook, with S&P’s base case for net government debt to be stabilised below 60% of GDP. The next months will allow S&P to monitor budget implementation and credibility as well as EU fund absorption, with some focus on the stability of the government coalition.

- It has also been a year ago since Fitch placed Romania’s BBB- rating on outlook negative due to worsening public finances which were exacerbated by the pandemic against significant challenges in medium-term fiscal consolidation. Fitch didn’t provide a specific timeframe for the negative outlook, but usually those are resolved within one to two years. With many uncertainties and risks still unresolved, we believe that Fitch might conclude its outlook review only by early 2022. Regarding the 2021 budget, Fitch acknowledged the policy focus shift towards medium-term public debt sustainability. Nonetheless, it remains unclear how some underlying challenges coming from spending rigidities – particularly regarding wages, subsidies and social benefits – will be addressed, with hopes for more details in the next months. Moreover, the focus will also be on institutional effectiveness, owing to a “very weak fiscal record” in pre-pandemic years and risks to the “cohesion of the coalition” from politically difficult policy choices.

Rating drivers/sensitivities, factors that could lead to an upgrade or downgrade

FX: Political jitters no game changer for EUR/RON stability

We don’t expect the recent political jitters and the coalition infighting to have a long-lasting impact on RON. As we discuss above, a solution should eventually be found while from a monetary policy perspective, the recent political developments do not change much in terms of the reasons behind the expected EUR/RON stability from here.

First, with CPI above the 2.5% target and set to remain so (but inside the 1.5-3.5% corridor) throughout the year and the adjustment in EUR/RON so far this year being already non-negligible (close to 6 big figures), the case for further meaningful managed RON depreciation is limited from here, due in part to the fact that RON has the highest regional FX pass-through into inflation.

Second, we expect EUR/RON to stabilise for most of the year and pencil in EUR/RON at around 4.92 by year-end, largely a reflection of the inflation differential between Romania and the eurozone. The move higher in EUR/RON, justified by the CPI differential, has already taken place this year, suggesting limited scope for further RON weakness from here. Importantly, in the prior two years, the bulk of adjustment in the EUR/RON corridor higher also happened in 1Q. We don’t think 2021 should be any different. The non-negligible FX reserves (18% of GDP as of February-2021) and upcoming inflows of EUR via the EU funds also mean that the National Bank of Romania has plenty of firepower to keep the EUR/RON well behaved.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article