Retaliation inevitable as Trump slaps tariffs on metals, again

President Trump has signed an executive order imposing an additional 25% tariff on steel and aluminium imports into the US, effective March 12, 2025. With four weeks until the tariffs take effect, there is still room for negotiation. But with many countries ramping up their trade defence, further trade escalation seems inevitable

During his first term as US president, Donald Trump announced tariffs of 10% on aluminium and 25% on steel imports, effective March 23 2018, under Section 232, citing national security concerns. Initially, only Mexico and Canada were exempt, but they, along with the EU, were hit with these tariffs two months later. Multiple deals eventually ended tariffs for many countries.

Under former President Joe Biden, tariffs on Chinese steel and aluminium were tightened. On July 10 2024, Biden imposed a 25% tariff on Mexican steel melted or poured outside North America and a 10% tariff on Mexican aluminium containing metal smelted or cast in China, Belarus, Iran, or Russia.

Now, President Trump has reintroduced steel and aluminium tariffs without exceptions, citing a surge in imports and a decrease in US capacity utilisation. He stated that the previous deals, often in the form of quotas, have become redundant and hurt US manufacturers.

How much does the US produce and where do US steel and aluminium imports come from?

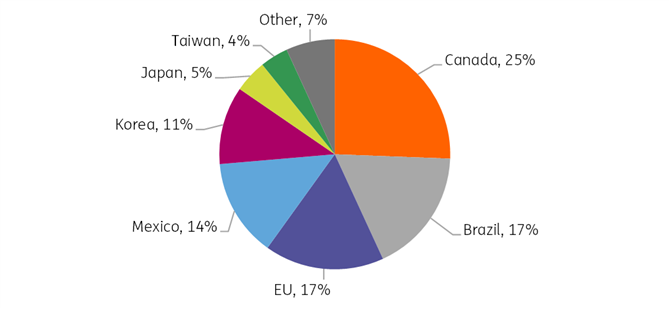

While the US produced some 79.5 million tons of steel in 2024, it still imported about 28.9 million tons, i.e. a quarter. China, the world's largest steel producer, produced 1,005.1 million tons in the same year. Regarding steel imports into the US, around 25% came from Canada, followed by Brazil at 17%, Mexico at 14%, and South Korea at 10%.

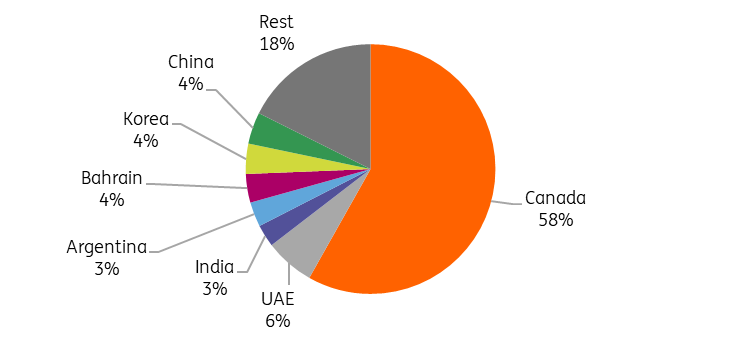

Likewise, the US imports roughly half of its aluminium from abroad, with Canada the biggest supplier, accounting for 58% of imports, followed by 6% from the United Arab Emirates. The US also relies on Mexico and Canada for around 90% of its aluminium scrap imports.

China, on the other hand, only accounts for around 4% of US aluminium imports. Tariffs and trade actions in recent years have reduced China’s desirability as a trading partner for aluminium products. A 25% rise in US tariffs on Chinese aluminium might have little impact on China’s aluminium industry. Many Chinese aluminium semi-finished product producers have already reduced exports after China cancelled an export rebate in December, retaining more material for domestic use. You can read about the potential impact of tariffs on aluminium here.

Aluminium supply to US

Steel supply to US

Aiming for jobs and production, but facing declining trends

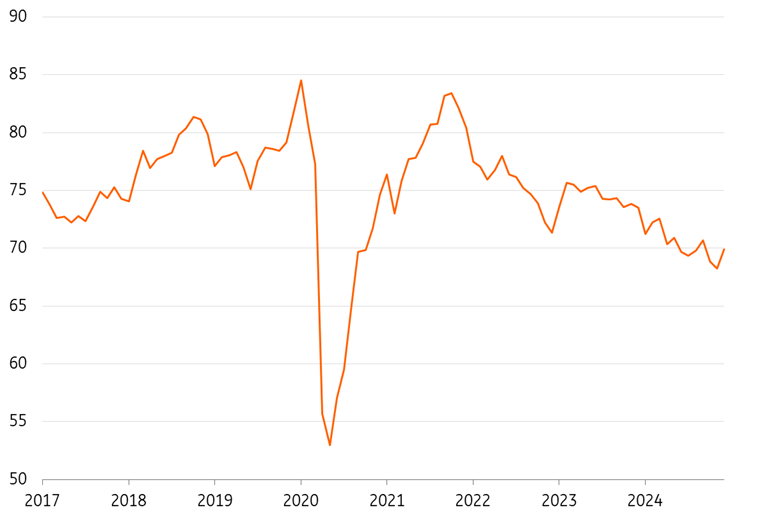

Trump said the new duties are meant to crack down on the efforts of countries like Russia and China to circumvent existing duties, bolster domestic production and bring more jobs back to the US. However, previous tariffs did not lead to increased domestic production of the two metals. Although US capacity utilisation for iron and steel briefly rebounded to 80% during Trump's first term, it has been declining since late 2021 and is currently at 69.9%.

Capacity utilisation would therefore need to increase by 10 percentage points to achieve the US administration's target level of 80%.

US capacity utilisation – iron & steel (%)

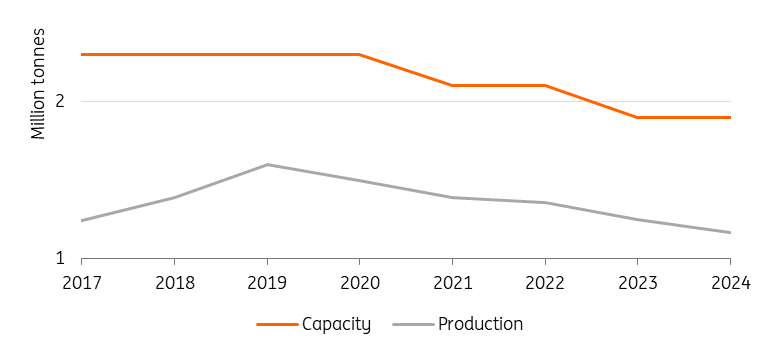

In 2024, the output of the US steel industry was 1% lower than it had been in 2017 before the introduction of the first round of tariffs by Trump, while the aluminium industry produced almost 10% less.

Despite tariffs imposed in 2018, US steel output has continued to fall

US steel production

For aluminium, the US has only four operating smelters. These four smelters together produced about 680,000 tonnes of aluminium last year, down from 741,000 tonnes in 2017, the year before Trump first introduced duties (according to data from Harbor Intelligence). In comparison, China produced around 43 million tonnes of aluminium last year.

Previous tariffs had no effect on increasing domestic aluminium production

Industries in the US like automotive and manufacturing, which heavily rely on imports of aluminium and steel and are deeply integrated with US supply chains, would face increased costs and disruptions if the proposed tariffs went ahead since many parts cross the border multiple times before becoming a final product.

In which countries will the steel industry get hurt most?

Not only would US steel and aluminium importers be affected, but steel manufacturers in Canada and Mexico would also face a significant impact, as more than 90% of their steel exports go to the US. However, the overall economic effect should be manageable for these countries, as steel exports represent only about 2% and 0.8% of their total exports to the US, respectively.

Brazil, on the other hand, would suffer more, as steel exports account for 14.5% of its total exports to the US in terms of trade value. This could lead to some economic repercussions for Brazil's steel industry but could also make a deal between the US and Brazil more likely.

Share of steel exports by selected countries

in %, by value, 2023

Additionally, we might see changes in trade flows of aluminium. Canadian exports might get redirected to Europe, where they have duty-free access. This shift could be bearish for European premiums, potentially lowering prices in the European market.

A clash with Europe is inevitable

While the US reached an agreement with South Korea, Australia, Argentina and Brazil shortly after tariffs were announced in 2018, other countries opted for retaliation. In June 2018, the EU responded to the US Section 232 tariffs on steel and aluminium with immediate retaliatory countermeasures in the range of 10-25% on motorcycles, agricultural products, bourbon, clothes, and steel, amongst others. Additional countermeasures were to be imposed after three years if no settlement was reached.

Then, on 31 October 2021, the US and the EU announced a multifaceted agreement to address the tariffs imposed during the Trump administration, replacing tariffs with a tariff rate quota (TRQ) system, allowing a certain volume of EU steel and aluminium to enter the US market duty-free. Any imports above these quotas would be subject to the original tariffs. The EU also agreed to suspend its retaliatory tariffs on various US exports, including American whiskey and motorcycles until 31 March 2025, while the US prolonged the TRQs on EU products until 31 December 2025.

This time around, even before the new tariffs were officially announced, the European Union issued a statement condemning any potential additional tariffs coming from the US. If the EU is hit by additional tariffs from March, it could simply reinstate its retaliatory tariffs on US exports.

And, if history is anything to go by, EU policymakers will not be the only ones opting for retaliation.

Aluminium prices set to rise while industrial metals demand will weaken

The prospect of a global trade war is bearish for industrial metals in terms of slowing global growth and keeping inflation higher for longer.

Aluminium is likely to be most impacted by potential tariffs on metals with the US importing significant volumes of its aluminium from abroad. Tariffs would result in higher aluminium prices in the US, representing a significant upside risk to the US Midwest premium this year. The US Midwest premium, the best indicator of tariff risk, is already up more than 30% since Trump won the US presidential election. The premiums are added to the global benchmark prices, which are set on the LME to deliver the metal to the US Midwest. However, the effects on LME prices will be minimal. US tariffs previously had little impact on LME prices. Tariffs also risk demand destruction in the US as the extra costs would most likely be passed on to end consumers.

With growth in the US likely to slow due to the tariffs, and with China already struggling to revive its economy, demand for industrial metals is likely to weaken. Benchmark steel prices were down 38% last year with higher interest rates hurting demand in steel-intensive industries like building and construction.

President Trump has laid the foundations for further trade escalations. This will not be the last tariff move. Retaliation is on, and it’s going to get nasty.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

11 February 2025

Our analysts’ views on Trump’s tariff developments this week This bundle contains 4 Articles