Resilience of US job creation set to be tested

The US economy added 151k jobs in February, but with DOGE’s influence increasingly being felt on the economy the risk is that we start to see renewed softness in the months ahead

| 151,000 |

US jobs added in February |

| As expected | |

Jobs report suggests no pressing need for additional Fed support

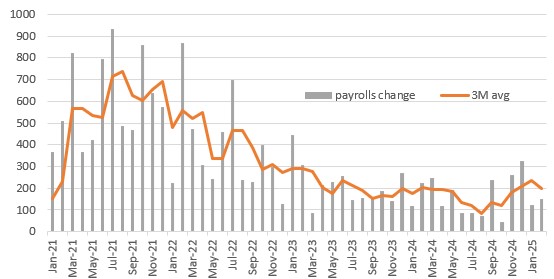

In terms of the headlines from the jobs report, US non-farm payrolls rose 151k in February versus the 160k consensus while there were 2k of downward revisions to the past two months. The unemployment rate ticked higher to 4.1% from 4% (consensus 4%) while hours worked remained at a very subdued 34.1 hours. Wages came in-line at 0.3% month-on-month/4% year-on-year. As such this report is modestly softer than expected, but in general the labour market remains in decent shape and suggests no pressing need for further imminent support via Federal Reserve interest rate cuts.

Monthly change in non-farm payrolls (000)

In terms of the details, federal government jobs fell 10k, which is the biggest drop since an 11k decline in June 2022, but there are obviously downside risks for coming months given the Department for Government Efficiency’s (DOGE) efforts to trim spending. Private payrolls rose 140k with trade & transport adding 21k and financial services also adding 21k. Private education and healthcare services continues to be the main engine of job creation, rising 73k, but leisure and hospitality fell for a second consecutive month. This may well be weather related after a cold snap in the early part of the year hit the hospitality industry.

Quality of jobs remains a concern

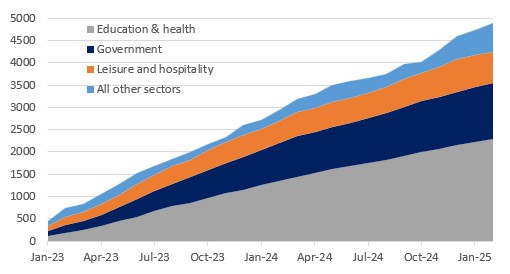

Our chief concern about the US jobs market is the quality of jobs that are being added. Since January 2023 only 13% of jobs created have been outside of leisure & hospitality, government and private education & healthcare services. These sectors tend to be lower paid, less secure and more part time in nature, a point borne out by the fact that the average working week in America remained at just 34.1 hours, down from 35 hours in 2021. We would feel much happier if it was technology, construction, manufacturing, business services, transport and logistics etc that was leading job creation – sectors that are typically associated with a strong and vibrant economy.

Cumulative jobs creation by industry (000s)

DOGE's influence set to weigh on future job creation

With next week's CPI report expected to post yet another "hot" 0.3% MoM print – we need to average 0.17% MoM over time to deliver 2% YoY inflation – and huge uncertainty over the economic impact of President Trump's policies this will keep the Fed on the sidelines with the March FOMC set to be a non-event. However, as DOGE effects become more apparent we expect to see the number of Federal government jobs being lost mounting. The bigger risk though is that private sector contractors working for the Federal government are trimmed much more. With tariffs also likely to result in some price rises, putting a squeeze on spending power, we continue to look for rate cuts to resume from the third quarter.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article