What the Red Sea crisis could mean for commodity markets

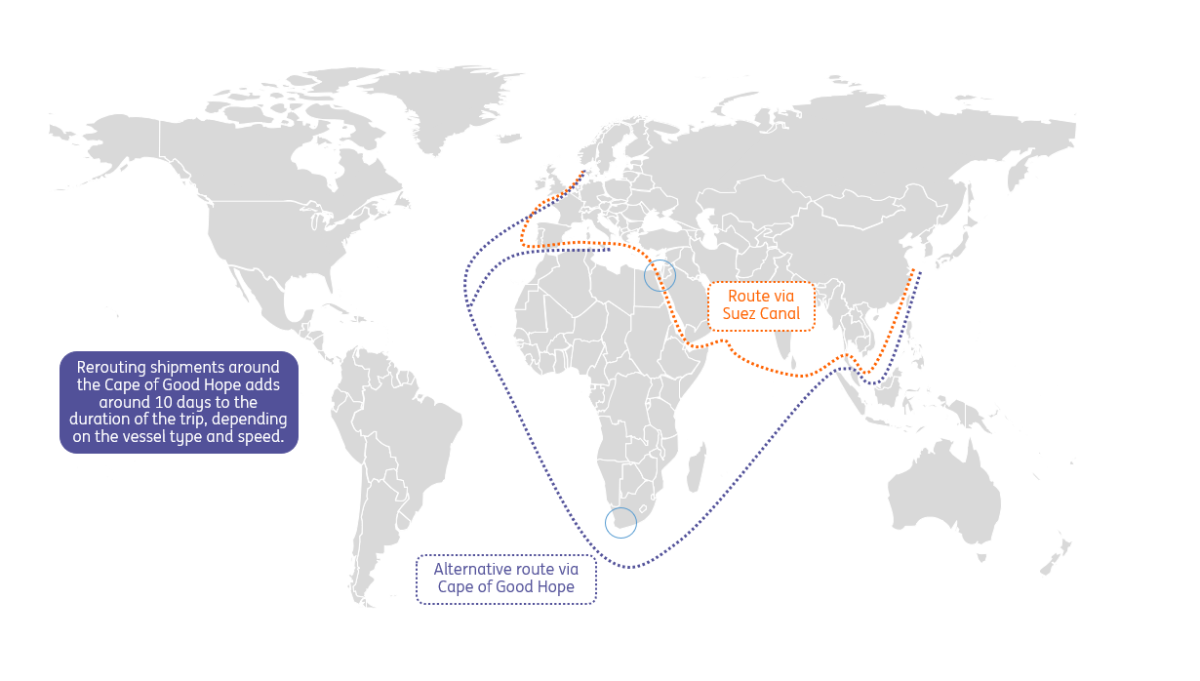

Attacks by Iranian-backed Houthis from Yemen on commercial vessels passing through the Red Sea have made some shipowners reluctant to sail via the Suez Canal and Red Sea. Instead, they're choosing the longer and more expensive route via Southern Africa. So, what does this all mean for commodity markets?

Attacks on commercial shipping in the Red Sea have recently intensified – and there doesn't appear to be any sign of tensions easing just yet. We have also seen retaliation from the US and UK in the form of carrying out airstrikes against the Houthis in Yemen. It remains unclear how the Houthis will respond to these attacks and whether they risk dragging in other actors within the region. But clearly, escalation raises both the risk of disruptions to flows and the likelihood that more shippers will reroute around Southern Africa.

For commodity markets, the increased tension poses supply risks, with energy markets most vulnerable. However, for oil and LNG, we are not seeing any fundamental impact on supply yet. Refiners and consumers could initially face some tightness as supply chains adjust to the longer route. Given the uncertainty and the risk of a spillover, oil prices are likely to remain relatively well supported. In order to see oil prices breaking significantly higher, we will need to see even further escalation and/or a meaningful loss in oil supply.

Red Sea conflict increases shipping times

Global oil flows

It is unsurprising that oil flows via the Red Sea are significant given the level of oil production in the region. Around 12% of total global seaborne oil trade goes through the Red Sea, alongside large flows of both crude oil and refined products. And this applies to northbound flows towards the Med and Europe, as well as southbound flows which ultimately go towards Asia.

According to the EIA, in the first half of 2023, 9.2m b/d of oil (both crude and refined products) went through the Suez Canal and SUMED pipeline. Meanwhile, 8.8m b/d went through the Bab el-Mandeb Strait, the chokepoint between Yemen and Djibouti. Volumes through the Suez and SUMED are larger, given that there will be some Saudi flows exported from the Red Sea (via the East-West crude oil pipeline) to Europe.

Since Russia’s invasion of Ukraine, there has been an increase of oil flows southbound towards Asia. This is a result of the EU’s ban on imports of Russian oil, which has seen Russian shipping to alternative destinations, particularly India and China. Some Middle Eastern countries have also taken larger volumes of Russian refined products, particularly Saudi Arabia.

Europe will also be pulling in more middle distillates from Asia and the Middle East via this route since the Russia-Ukraine war. According to Refinitiv shipping data, in 2021, middle distillate (gasoil/jet fuel) flows from the Middle East and Asia to Europe averaged a little over 490k b/d, whilst in 2023, these flows averaged almost 860k b/d. A large share of this would go via the Red Sea.

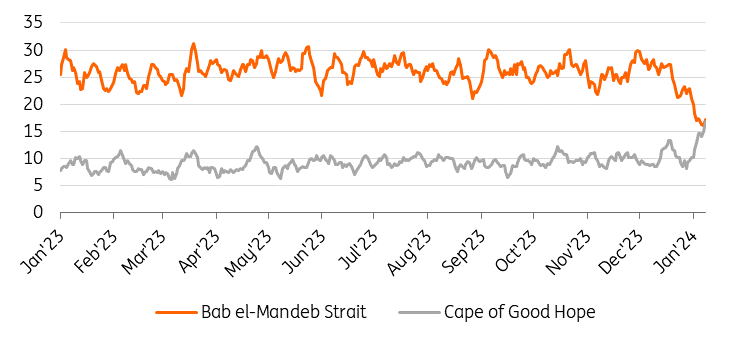

There have been announcements from a growing number of shippers that they will avoid shipping through the region and instead go around the Cape of Good Hope. While tanker traffic through the Red Sea in December held up well, it started coming under pressure in January, particularly after the US and UK airstrikes in Yemen. This obviously means longer voyage times, which could lead to some tightness in oil and products as the market adjusts. It would also reduce tanker availability and push up rates.

7-day moving average of daily tanker transit calls

The risk to oil flows through this region will be a concern for some importers, particularly those who rely on a large volume of crude oil via this route. India stands out with its growing dependence on Russian oil. While we think that Russian flows will be able to travel through the region without the risk of facing attacks, India may still feel it is prudent to diversify supplies – especially given the more recent escalation. If this were the case, there could be potential that we see the discount on Urals widen.

For now, it is important to note that whilst the current situation is leading to a growing number of tankers being diverted, we are not seeing oil unable to move to destination or oil supply declining. Initially it may lead to some tightness for refiners as their supply chains adjust to the longer shipping times. We will also need to see if tanker capacity is adequate to deal with longer voyages. For now, the Red Sea attacks do not change our oil balance.

A bigger risk for the oil market is if the situation spreads, leading to disruptions of oil flows going through the Strait of Hormuz. While we believe the risk of this is low, it needs to be monitored, particularly after Iran recently seized an oil tanker in the Gulf of Oman. A little more than 20m b/d of oil flows via the Strait, which is equivalent to around 20% of global consumption. Only Saudi Arabia and the UAE have pipeline capacity to avoid the Strait of Hormuz. Between them, they have capacity of around 6.5m b/d.

Clearly, an escalation which puts Persian Gulf oil flows at risk will be much more of a concern for the oil market and global economy. Ships can avoid the Red Sea by going around the Cape of Good Hope. Unfortunately, aside from some Saudi and UAE flows via pipeline, there are no alternative routes for the bulk of flows from the Persian Gulf. The Strait of Hormuz is the only option.

Red Sea has become increasingly important for LNG flows

LNG flows through the Red Sea have increased recently. Around 8% of global LNG trade now passes through the region.

As US LNG export capacity has grown, we have seen more LNG going via this route towards Asia. This is particularly the case currently given the constraints over shipping through the Panama Canal due to dry weather. Given the stoppage of Russian pipeline gas to Europe, Europe is relying increasingly more on LNG, which leaves the European market more vulnerable to developments in the LNG market.

In the Middle East, Qatar is the largest supplier of LNG to Europe. In 2023, Qatar sent a little more than 20bcm of LNG to Europe, which makes up in the region of 16% of total European LNG imports. There are also some marginal volumes from Oman and the UAE. These flows would all pass through the Red Sea and Suez Canal.

While LNG carriers have managed to avoid recent attacks, a growing number of carriers are already avoiding the Red Sea. This would be the case for US LNG, and recent reports suggest Qatar would also avoid shipping its LNG through the Red Sea.

If the situation deteriorates, it may lead to some disruptions and longer shipping times in the short term – but where there is flexibility, it's expected that we'd see shifts in trade flows. This could include US LNG which was destined for Asia being rerouted to Europe, and Middle Eastern (Qatari) LNG moving into Asia rather than Europe. In doing this, these flows will avoid the Red Sea and will not have to take the longer route around South Africa.

Where this becomes more of an issue for the LNG market is if we were to see disruptions in the Strait of Hormuz, as this would put Qatari LNG flows at risk. Qatar shipped an estimated 108bcm of LNG in 2023, making it the third largest supplier with about 20% of global LNG supply.

Tensions increase metal shipping times and costs

For metals shipped in containers, the Red Sea conflict poses an upside risk. Container freights are the most affected by rerouting, increasing shipping times, delaying shipments and boosting freight costs.

Roughly half of the shipped tonnage crossing the canal are containerised goods, making it the most important artery for container trade. In the three weeks after mid-December, some 80% of the container vessels on the Suez route have been forced to change course, a level which reached 90% in the first week of January (according to Clarksons). Market leaders MSC and Maersk have diverted over 60 container vessels around the Cape in just three weeks. Other larger container liners – Hapag Lloyd, Cosco, ONE, Evergreen, HMM and ZIM – have followed suit.

This is increasing freight rates, with container rates already more than tripling. It's also adding weeks to delivery times. The higher shipping costs will need to be eventually passed through to the end-selling price for metals.

For aluminium, this is bullish for prices – particularly for premiums, rather than the LME price. Primary aluminium premiums in Rotterdam have increased by around 10-15% since the beginning of December after months of decline, according to Fastmarkets data.

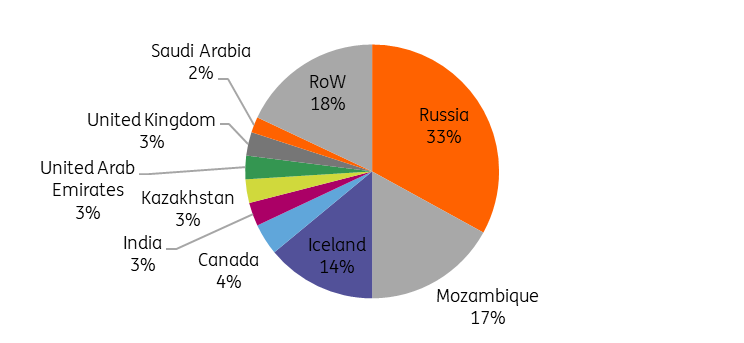

LME forward spreads remain in a wide contango, providing further support to premiums. The aluminium cash/three-month spread was last at $48.50 per tonne contango. The Middle East is one of the key markets for Europe when it comes to sourcing aluminium and any disruptions there are likely to support the premiums.

Europe relies heavily on aluminium imports with nearby supply constrained. The shipping disruptions come at a time when Western European aluminium production is the lowest this century. Several output cuts have taken place in Europe since December 2021, accounting for 2% of the global total. Soaring energy costs following Russia’s invasion of Ukraine have squeezed producers’ margins, with energy-intensive metals like aluminium in particular being affected.

Low premiums over the past few months have also weakened incentives to ship material to Europe, which has left many in the aluminium market without buffer stocks should demand improve more than expected in the coming months.

European primary aluminium imports by country (2022)

Agri flows less concerning

Agricultural flows are less likely to be significantly disrupted by developments in the Red Sea. Saying that, however, we have been seeing increased volumes of US grain taking the longer route via the Suez Canal and onwards to Asia, rather than through the Panama Canal. These increased flows have come about due to the ongoing restrictions at the Panama Canal. Obviously, voyage times will increase further if these shipments now have to avoid the Suez Canal and go around the Cape of Good Hope.

In addition, there are several standalone sugar refineries in the Red Sea, which may find it more difficult to export containerised refined white sugar due to container ships avoiding the region. This could potentially lead to some tightness in several domestic markets within the region and parts of Africa. Obviously, this is not only applicable to sugar. A number of containerised agri commodities could see disruptions as a result.

There are also potential indirect impacts from the Red Sea attacks on agri markets. If they persist and lead to increased delays, farmers could see their input costs increasing. This would materialise in the form of higher diesel prices and potentially higher fertiliser prices.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article