ReArming the European market outlook

Europe is known to move little in good times and fast in times of crises. This week, European fiscal spending seems to be making a return as recent proposals from the European Commission and Germany suggest that a large fiscal push to boost defence and infrastructure spending is on its way. Markets have reacted strongly; here, we take a look at what it all means

European defence spending set to increase materially but don’t expect an economic miracle

The Commission’s plan to ‘rearm’ Europe and to unlock extra defence spending largely hinges on invoking the national escape clause of the Stability and Growth Pact again. According to the plan, this could potentially unlock €650 billion if countries allocate an extra 1.5% of GDP to defence, raising average EU defence spending to 3.5% of GDP. This approach would enable countries to exceed the 3% of GDP deficit threshold without triggering the Excessive Deficit Procedure.

The proposal includes creating a €150 billion fund from which countries can borrow specifically for defense purposes. This would be particularly beneficial for countries that face higher interest rates, as it would provide them with more favourable borrowing conditions compared to borrowing independently. However, borrowing from this fund would not be considered additional defence spending because it is intended to help countries meet the target of increasing defence spending by 1.5% of GDP.

The plan also allows cohesion funds to be used for defence spending, but it falls short of creating a shared fund for joint spending. The fact that the plan does not involve a hard target for spending, but more an estimate of what would happen if Europe used the escape clause to increase spending by 1.5% of GDP, makes it uncertain whether the €800bn mentioned by the Commission will be reached.

The question remains as to whether markets will be as benign as the Commission when fiscal spending increases

While the plan gives leeway for extra fiscal spending from the Commission’s perspective, this would still result in significant increases in government deficits and debt. With countries like France and Italy already expected to have deficits exceeding 3% this year and high debt levels, the question is whether markets will be as benign as the Commission when fiscal spending increases. Some countries may therefore still limit spending on defence or cut spending elsewhere to accommodate, much like the British plan for additional defence spending.

The economic impact could, in turn, be more muted in countries with high debt levels and spreads. Besides that, a lot of extra defence spending will likely come from imports as defence equipment is mainly bought abroad. Europe will likely expand its own capacity, but in the early stages of additional spending, it is likely that a significant amount goes to imports. That means that the expected sizeable increase in defence spending will be dampened by multiple factors when it comes to the GDP impact. Think of 0.1-0.2% for the coming years.

Germany delivers a stunning U-turn

As for Germany, this week marked a historic U-turn with the country's decision to (probably) ditch its fiscal debt brake to allow for additional defence spending and to come up with a €500bn fund for infrastructure investments. However, there are still a few stumbling blocks – the most important being the challenge of obtaining a two-thirds majority in parliament for the proposals to change the debt brake and start an infrastructure investment fund. The next government wants to use the ‘old’ parliament next week – before the newly elected parliament holds its constituent meeting – to get a two-thirds majority together with the Greens.

The political challenge now is selling the concept of historical shifts taking place under the 'old' parliament

Not everyone within the Christian Democratic Union (CDU) will be happy with the move towards large fiscal stimulus, leaving it unclear whether all of its MPs will really vote in favour next week. Finally, the political challenge now lies in how to sell it to voters that historic shifts are happening under the ‘old’ parliament when a new parliament has just been voted in. All in all, it isn't a strategy without risks. Let's also not forget that there currently is no new government and that even official coalition talks have not started just yet.

Turning to the potential fiscal stimulus, the €500bn infrastructure investments spread over 10 years will definitely boost German growth. The multiplier of such investments should be around one, and there might even be some positive spill-over effects to the rest of the eurozone. What remains unclear at the current stage, however, is whether any incoming government would make expenditure cuts elsewhere and what possible crowding-out effects from more government spending could look like. But just a simple partial analysis shows that the €500bn fiscal stimulus could boost German growth by more than one percentage point per year – an impact we had already pencilled in prior to the elections. As for defence spending, the incoming government hasn’t made any announcements on actual spending targets, only that it would do “whatever it takes” to increase the ability of both Germany and Europe as a whole to defend themselves.

All of this leaves us with a hugely symbolic and signalling effect that Europe has finally woken up. How much of this week’s headline numbers will really make it into the eurozone economy, however, remains – at least for now – uncertain. That said, we now see the terminal rate for the ECB easing cycle at 2.25%.

Rate markets are fundamentally revising their long-term outlook

The large rise in Bund yields is much more than just an issuance story and reflects an overhaul of markets’ economic outlook further in the future. Historically, long-term interest rates have been anchored around future expectations of GDP growth and inflation. In the US, this relation can be backtracked to the 1960s, and in the eurozone, it held firmly in the years before the global financial crisis (see figure below).

So far markets have been sceptical about Europe’s ability to avoid a return to the secular stagnation environment from before Covid. Surveys by the European Central Bank from January this year suggest a long-term nominal growth expectation of around 3.3%, well above the current 10Y swap rate of 2.7%. A decomposition of the survey results highlights the tilt towards downside risks; around a third of all forecasts do not see the eurozone growing by 1% or more.

If markets gain confidence that eurozone real growth can trend north of 1% and inflation around 2%, then swap rates can still rise significantly. More importantly will be markets’ perception of the downside risk. With Europe showing a willingness to spend big over the coming years, a secular stagnation scenario of growth rates below 1% and inflation failing to meet its target becomes considerably less likely.

The 10Y swap rate could start converging closer to 3.5%

In the case of a broad revision in nominal growth expectations, we can see the 10Y euro swap rate increasing to 3.5% in an optimistic scenario. In this case, markets maintain the belief that Germany will follow up on its promises and a secular stagnation scenario is discounted heavily. Markets would see the ECB cut to 2.25% and stay there. Once the ECB lands at 2.25%, rates would slowly position for a possible hike as growth numbers improve. The 2Y rate would therefore remain well above the ECB deposit rate. Meanwhile, the 10Y rate gradually converges towards the nominal growth anchor.

Euro rates have significant upside potential in an optimistic scenario

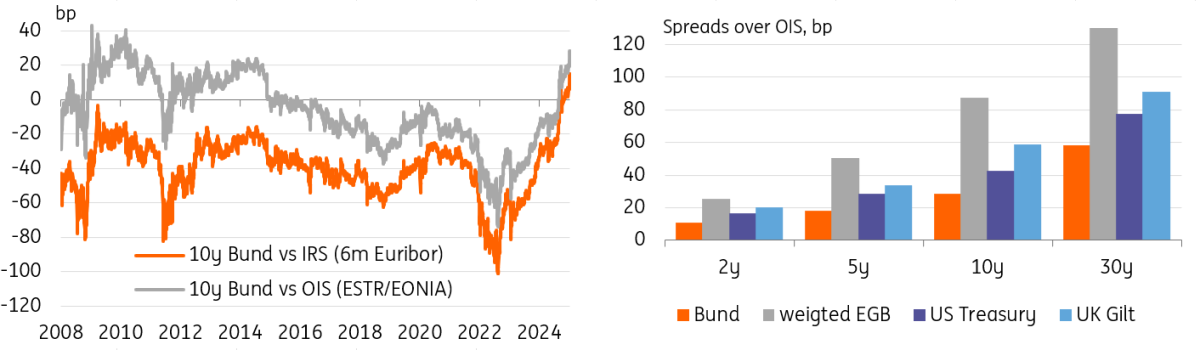

German Bunds at the epicentre of supply pressures

Bund yields were at the epicentre of market repricing following the fiscal regime shift. Following the surge higher, 10y Bunds are now yielding around 28bp above overnight indexed swap (OIS) rates, up from an average of 20bp for much of February.

Historically speaking, these are not the cheapest levels, however. 20bp was the average seen prior to the ECB embarking on quantitative easing, and 40bp over was seen following the global financial crisis when German deficits rose above 4% and debt to GDP surged to 80%. Those elevated levels were short-lived, though, as Germany then introduced the debt brake and balanced its budget by 2014.

The market is now looking at the possibility of German deficits running again at 4% and the debt ratios tracking towards 90% within a decade, as the opponents of the current plans in Germany caution – the point of orientation for markets is past levels over OIS and still cheaper levels of government bonds abroad. Unless markets can be convinced otherwise by the upcoming negotiations around the package and during the government formation talks, Bunds are unlikely to meaningfully perform versus swaps again. In the longer run, it gives rise to the possibility of pushing 10y Bund yields into the 3.5-4% range.

German Bunds aren't looking so special any more

FX: Re-assessing the euro

As in the rates space, FX markets have seen substantial moves as the euro’s prospects have been re-assessed. EUR/USD has had its largest five-day move since November 2022 and one-week realised volatility also sits close to the highest levels seen in two and a half years.

The potential seismic shift, particularly in the German fiscal position, has been the game changer this week. This has been sufficient to reprice the ECB terminal rate some 25bp higher. This comes at a time when US growth rates are being re-priced lower on the back of softening consumption. The ‘Atlantic’ spread (two-year EUR/USD swap rate differentials) has narrowed 25bp over the last week and has been a pivotal factor driving EUR/USD higher.

But there’s a whole lot more to the story. On the debatable assumption that the German infrastructure fund does not get watered down substantially and delivers a European renaissance, what could this be worth to the euro? Indeed, some are arguing that EUR/USD could be set for a 2017-style rally, when Europe was positively re-assessed after the Dutch and French elections.

The chart below looks at the relationship between equity inflows to the eurozone and the ECB’s trade-weighted euro. 2017 did indeed see significant interest and the euro rallied. The thing is that the eurozone has already been witnessing some decent inflows over the last 12 months, and the trade-weighted euro is already strong. The big problem, however, has been that the dollar is even stronger. This suggests that a much higher EUR/USD forecast may require as much of a negative re-assessment of the dollar as it does a re-rating of the euro.

Eurozone equity inflows have helped the euro

Our current forecasts for 1.02 and parity later this year heavily relied on the view that the ECB would cut rates below 2% due to the absence of material fiscal stimulus in the euro area. Not only has that notion now been overturned, but the activity outlook for the US has deteriorated and the market sees the Federal Reserve on a more dovish path compared to our previous baseline assumptions.

Based on new assumptions for the ECB's terminal rate at 2.25% and using the market's current pricing for the Fed cycle to generate a new EUR-USD short-term swap rate differential profile suggests EUR/USD could end this year around 1.08 and end next year around 1.10.

However, we still think there are downside risks to the euro this second quarter stemming from tariffs. Certainly, the rapidly changing macro and geopolitical environment still warrants great caution, and we will be working with colleagues to deliver a formal new FX profile. But we have seen a historic shift in the German fiscal approach, and that strongly argues for a 1.05-1.10 EUR/USD range as opposed to the previous 1.00-1.05 – even when accounting for US tariffs.

To gauge how EUR/USD performs in the medium term, we will also be using our Behavioural Equilibrium Exchange Rate (BEER) model, which provides an indication of fair value in real terms based only on economic factors (trade, productivity, government spending) and excluding interest rate differentials.

The most important driver of EUR/USD in the medium term is the terms of trade differential, on which the impact of a US-EU trade war is still unclear. However, higher domestic government consumption is a positive input for the euro, as is potentially higher productivity. These two factors can lift the EUR/USD medium-term equilibrium levels, more than offsetting the negative impact of a shrinking eurozone current account surplus.

EUR/USD medium-term fair value is around 1.10

CEE FX: Clear risk of stronger currencies in the medium term

The CEE region is once again at the centre of geopolitical events, this time on the positive side. Any boost in the German outlook would mean a significant boost for the CEE region – and that's the clear direction. On the economic side, typically the Czech Republic and Hungary show the highest beta to German GDP momentum. The main reason for this is the openness of these economies and the interconnectedness through the automotive sector, where roughly a third is directly interconnected through German industry. The Czech Republic also shows the highest share of exports to Germany (33%), followed by Poland (28%), Hungary (25%) and Romania (20%).

At the same time, both the Czech and Hungarian economies are in the recovery phase of the cycles. A boost from Germany could further accelerate the current momentum in these countries, but also in the region as a whole. Infrastructure investment should mainly support the Czech Republic given the geographic interdependence of the two countries, and defence spending should find a match in the Czech Republic and Poland, which have the largest share of military production within the CEE region.

In terms of market implications, if we take Ukraine and US tariffs off the table for a moment, the German fiscal impulse is clearly positive for the CEE region. In the short term, the way in which central banks handle this issue will be key. They currently stand on the hawkish side, and German stimulus may support this narrative and reduce the scope for rate cuts. All countries except the Czech Republic are currently on hold in their respective cutting cycles. For the Czech National Bank, this may mean less room for rate cuts, and the risk to our forecast is one cut instead of two by the end of the cycle in May. Other central banks may therefore extend the wait for rate cuts or end the cutting cycle altogether.

In the FX space, key to watch will be the dynamics in the rate differential in the short term. In the long term, a GDP boost should support FX. In the near term, however, we see a more complicated picture. The spike in EUR rates over the last two days shows CEE rates outperforming, leading to a narrower differential, which has been a less important driver in recent weeks. In periods where the market largely follows sentiment, it is only a matter of time before rates come into play again, implying weaker CEE FX for the time being. It will also take a while for central banks to get their views together and send out hawkish signals.

Over the coming days, we will be more range trading depending on political headlines. Looking further ahead, the GDP boost and hawkish stance from central banks create a clear risk of stronger currencies than our forecast.

Credit moves prove short-lived

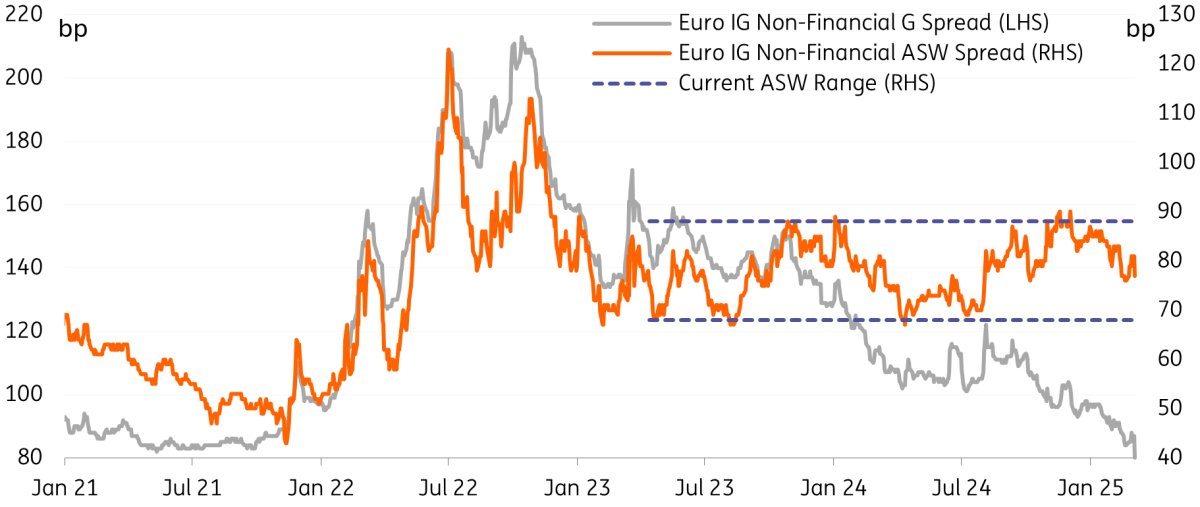

Credit was not immune to the turbulence seen in markets, but the reaction was perhaps a bit underwhelming and certainly short-lived. An initial widening of 6-8bp across the board in EUR IG credit was pencilled in late last week, followed by another round of just 2-3bp widening on Tuesday. This was, however, short-lived, and cash spreads began to retrace yesterday with tightening to the tune of 5-6bp. The credit space continues to be a highly demanded, technically strong market, where any little widening of spreads immediately opens up opportunities for buying. These hiccups in spreads are therefore generally very short-lived. Furthermore, as rates begin moving upward, yields become increasingly attractive in credit. This amplifies the buy-and-hold strategy to lock in yields, driving up demand for holding credit.

Currently, credit spread valuations can be described as challenged from various angles. Credit spreads over government bonds are particularly unfavourable, trading below the tight levels seen in 2021. The widening of Govie spreads makes credit look particularly rich and unattractive against Supranational, Sovereign, and Agency bonds (SSAs).

Slightly more value appears on an asset swap spread basis for corporates, as we trade in the middle of the range. Regardless, we don’t see much tightening potential in asset swap spreads as we expect spreads will stay elevated within the range.

EUR Non-Financial Spreads

As highlighted above, the swap rate curve is still set to see some steepening. While the credit spread curve has been steepening over the past year, we still see a bit more room for this to continue – particularly in lower-quality credit. As such, the yield curve is still set to see more steepening from here, despite already having a decent shape to the curve. As such, we see the best positioning currently in the three to five-year area of the curve.

The secondary market is looking a touch on the light side in general, with liquidity not being anything to write home about, and in turn, the primary market is receiving a lot of attention. Even during times of slight weakness and wobbles in spreads, new issues are still able to comfortably come to the market. Supply can only be described as plentiful so far this year, as outlined in further detail in our report.

Despite this large supply, the demand for new issues is very strong, as illustrated in the significant oversubscription levels and remarkably consistently low new issue premiums, with many deals even pricing through the curve. Even during the recent widening and volatile times in markets, deals are getting priced with strong demand.

EUR credit yield curves

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article