Real estate spreads show resilience in tariff sell-off

Europe's real estate spreads have not been immune from recent credit market turmoil, but have performed better than other sectors with only mild widening. The sector is somewhat insulated in a recession and benefits from lower interest rates. Companies with a higher exposure to development or the US are more affected, but the impact should be manageable

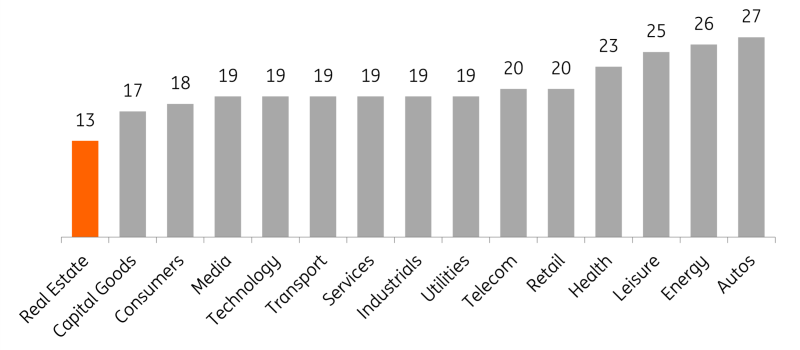

Real estate spreads seeing less aggressive widening

European credit spreads have been widening significantly since last week’s tariffs announcement, but for the real estate sector, the moves have been less aggressive than for other sectors. Real estate spreads are around 13bp higher on average than last week and widened by 6bp yesterday. This compares to a widening of 19bp for Euro corporate credit over the last week, with a strong risk-off move yesterday of 6bp.

Euro real estate spreads have outperformed in the recent credit wobble (bp)

Tariff risk is largely limited to secondary impacts

The relative outperformance of real estate bond spreads since US President Donald Trump’s tariff announcements is driven by several factors, including:

- Rents will continue to be paid – More limited exposure to and impact from US tariffs. Most real estate companies operate domestically, and the proportion of revenues from the US (excluding US companies) is relatively limited. In addition, despite rising recession concerns on both sides of the Atlantic, real estate should be relatively insulated as people and companies tend to continue paying their rent and lease costs during downturns.

- Rates compression – Market interest rates compressed last week, and the curve bull flattened. Markets are also now pricing in a higher level of cuts from the European Central Bank this year (around 80bp or just over three rate cuts) compared to around 60bp at the start of last week. Lower rates and a flatter rates curve are positive for the real estate sector, given the sensitivity of the sector to market rates.

- Coming from a lower base – The real estate sector remains in recovery mode, and spreads were already more elevated than other sectors. Furthermore, property valuations have already seen steep declines in recent years, while property yields are also still elevated. This may have helped cushion the blow in the current credit risk-off environment.

- Rebalancing of supply chains – Relocation of capital to Europe and ‘nearshoring’ options for European business, industry and defence manufacturing may have offset some of the tariff concerns – particularly for some affected subsectors, including logistics and retail. German infrastructure spending plans also help here.

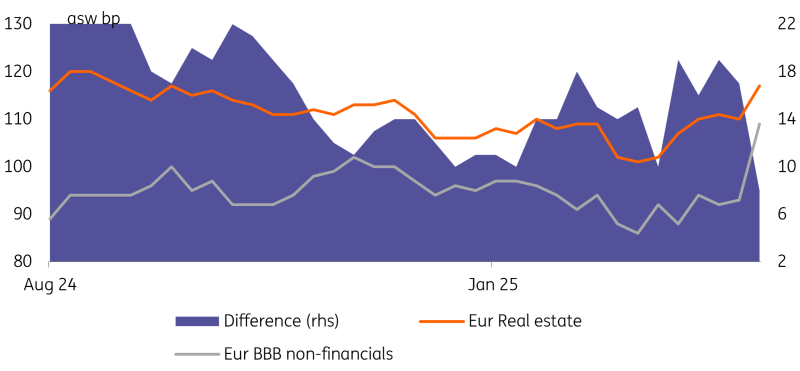

European real estate 'outperforms' Corporate BBB's

Peeking at equity markets, the EPRA Developed Europe Real Estate Index is down 6% since the start of last week, compared to the EURO STOXX 50 Index down by 11%. This indicates that the financial markets view real estate as a relatively safe haven compared to (most) other sectors.

A good place to hide

To be clear, we still expect European real estate credit markets will continue to face upward pressure on spreads, in line with the broader market (as our Credit Strategy team outlines HERE), but so far real estate has been a good place to hide.

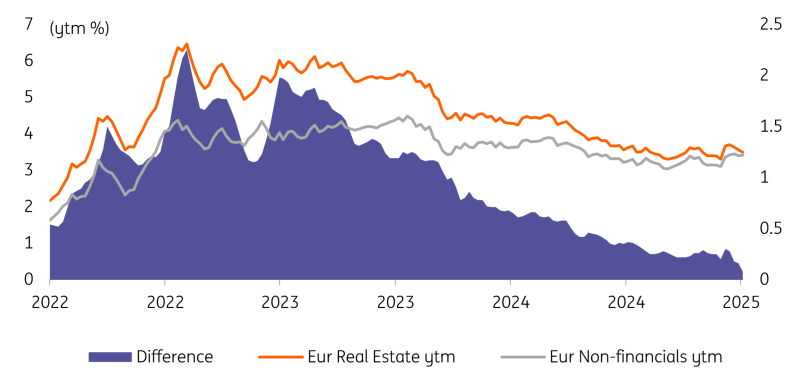

Still, we think real estate spreads can remain more resilient in the tariff-induced widening and volatility currently driving markets. The real estate spread premium over Corporate BBB’s is now just 8bp, the lowest since 2021. Additionally, as shown below, the real estate sector yield has nearly converged with Corporate BBB’s. If recession risks increase in Europe, certain subsectors are more exposed (Hotels, Retail and lower-quality Offices), although our ING economics team currently rules out a severe European recession.

Yield difference is now minimal

Tariffs and recession risks

As mentioned, we believe direct impacts from tariffs are limited for the real estate sector. However, we recognise that indirect effects such as lower exports, higher uncertainty, lower investments and weakening labour markets could slow or stall the real estate sector’s recovery. While this could put pressure on demand and occupancy rates, these effects should not really impact credit metrics.

Also, higher spreads can put pressure on funding costs, although so far this has been mitigated by the decline in interest rates. Our ING rates team also has a bullish bias in rates for now, and European rate curves are bull flattening today again as we write.

For property valuations, there is a likelihood that lower interest rates on recession concerns won’t translate into lower property yields. Further, slower growth dampening property demand and slowing rental income growth may put upward pressure on property yields. However, property values have declined by 15-30% since early 2022, and current yields are around 150-200bp higher than in 2021.

How real estate sectors might be affected by tariffs and macro weakening:

|

- |

Hotels: reduced travel and corporate spending lead to revenue weakening and declines in occupancy rates

|

|

- |

Offices: Rising unemployment, lower business investments, reduced demand for office space and increased remote working

|

|

- |

Retail: declining consumer spending, particularly on elastic and higher-end spending, combined with higher costs from reciprocal tariffs

|

|

= |

Logistics: Headwinds from supply chain disruptions and decreased consumer demand, but offset by re-routing of supply chains and shortage of available supply

|

|

+ |

Residential: (regulated) residential markets are less cyclical and benefit from stable revenue. Economic and job insecurity can lower demand, but Europe’s housing shortage remains the key driver. Also benefits most from lower interest rates

|

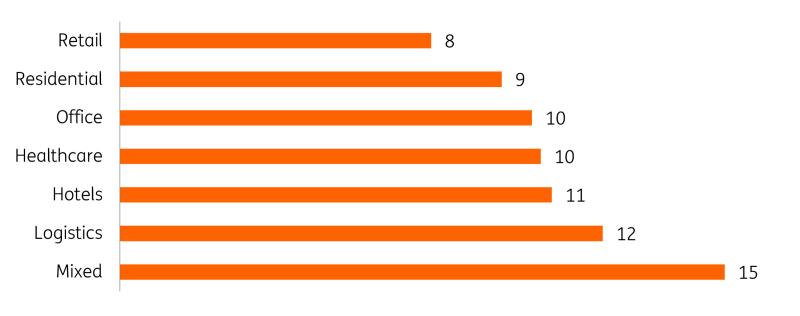

Spreads have also reflected this by subsector since the tariff announcements. Hotels, Logistics and Mixed (diversified names with main exposure in Offices & Logistics) have underperformed. While Residential and Healthcare have remained resilient. Offices has seen an average widening. Interestingly, Retail has remained relatively resilient, although this is likely to have been driven by the large, high-quality names, including Unibail (URWFP) and Klepierre (LIFP) remaining more liquid over the past couple of days.

Spread change since 'Liberation Day', by subsector

Whilst markets now seem to be regaining some confidence, tariffs are likely to continue driving volatility in spreads. Real estate has so far been more resilient, despite the headwinds the sector still faces. While uncertainty remains, including around tariff negotiations, market conditions and rising recession risk, real estate's limited impacts from tariffs could continue to support the sector in the near term.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article