Real estate EUR bonds: Strong supply meets strong demand

- 30 June 2025

- Credit Real estate

Real estate EUR bond supply has picked up in the first half, already topping all of 2023. Once unloved, the sector is now recovering well, with strong investor demand despite increasingly tight pricing. Supply should be manageable in the second half, with issuers shifting focus to refinancing 2026 maturities, should market conditions remain favourable

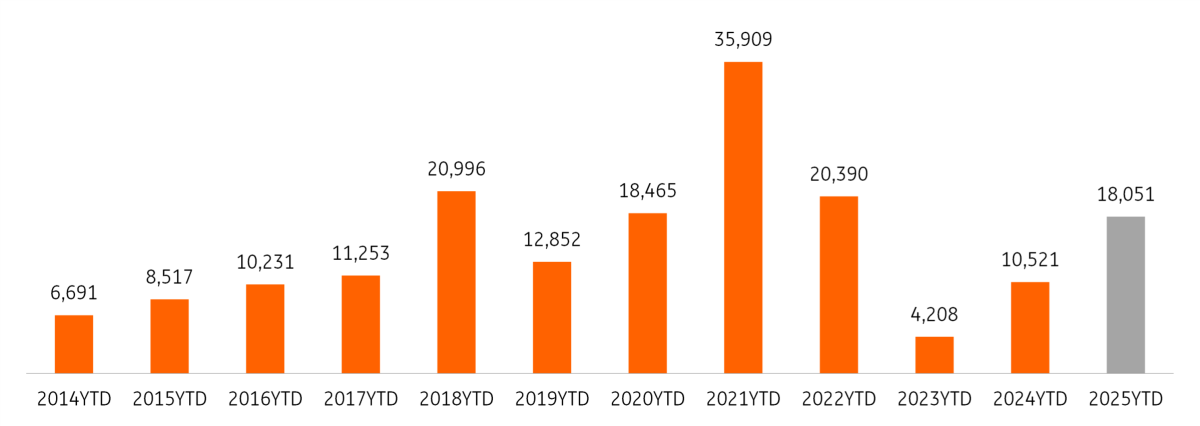

Real estate EUR supply has trended upward so far in 2025

Real estate EUR-denominated supply has increased in the first half of 2025 compared to the last few years. Supply has reached around €18bn so far, compared to €4bn and €10bn in the same period in the previous two years. In fact, year-to-date supply already exceeds total supply in 2023 by more than double, despite only being at the mid-year point. However, this is still below some of the record years for bond supply, including 2018, 2020 and 2021. Furthermore, recent months have seen an increase in the pace of supply, with €4.5bn and €5bn printed in May and June, as the market has well and truly reopened.

Year-to-date bond supply has clearly picked up (EURm)

Bond supply has been well absorbed by the market, with average books remaining in excess of 4x. This is despite many bond deals coming with relatively small new issue premiums or even with spreads pricing inside of where existing bonds are trading. A few of the reasons why supply has gone down well this year:

- Real estate spreads still offer more value compared to most other sectors, as the credit asset class as a whole is quite compressed

- Limited bond supply in 2023 and 2024

- Many investors are still underweight the real estate sector, and with an improving sector outlook, are now increasing their exposures

- Geopolitical risk and (direct) tariff exposure are limited

- Interest rate cuts benefit the sector

- Cash levels in general remain significant for credit investors

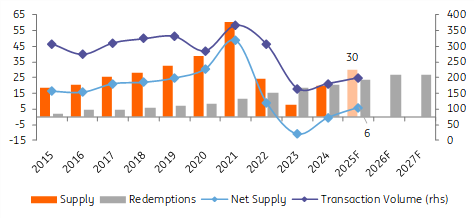

We maintain our supply expectation of at least €30bn for the full year for real estate, and supply is likely to continue to be absorbed well by the market. We do expect a bit of a slowdown in the level of supply for the second half compared to the first, as is usually the case. Also, redemptions are slightly lower in 2H compared to 1H (€10bn vs €13bn, respectively). At these levels, net supply remains modest - at least €6bn -and while positive, this is lower than most other sectors, which is a supportive technical for the real estate bond market.

Real estate supply is still forecast to reach at least EUR30bn this year

Focusing on 2H25 and 2026 bond maturities

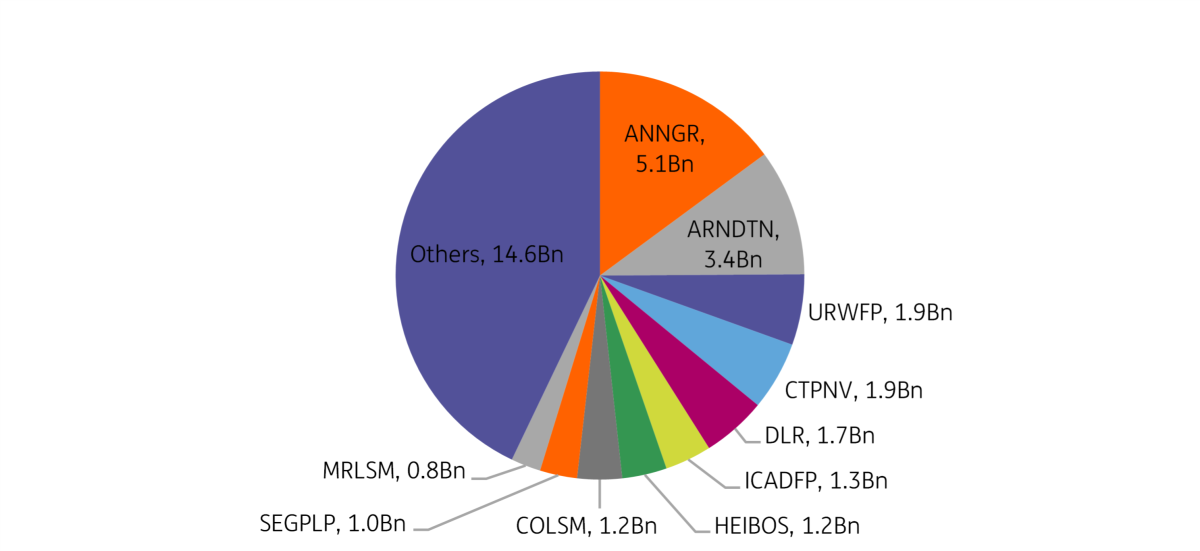

Looking ahead at upcoming bond maturities, roughly €10bn of bonds mature in 2H25, which is quite a manageable level. It picks up in 2026, with a total of €25bn in redemptions, of which nearly €17bn is in the first half of 2026.

EUR-denominated bonds maturing in 2H25 and 2026 (EURbn)

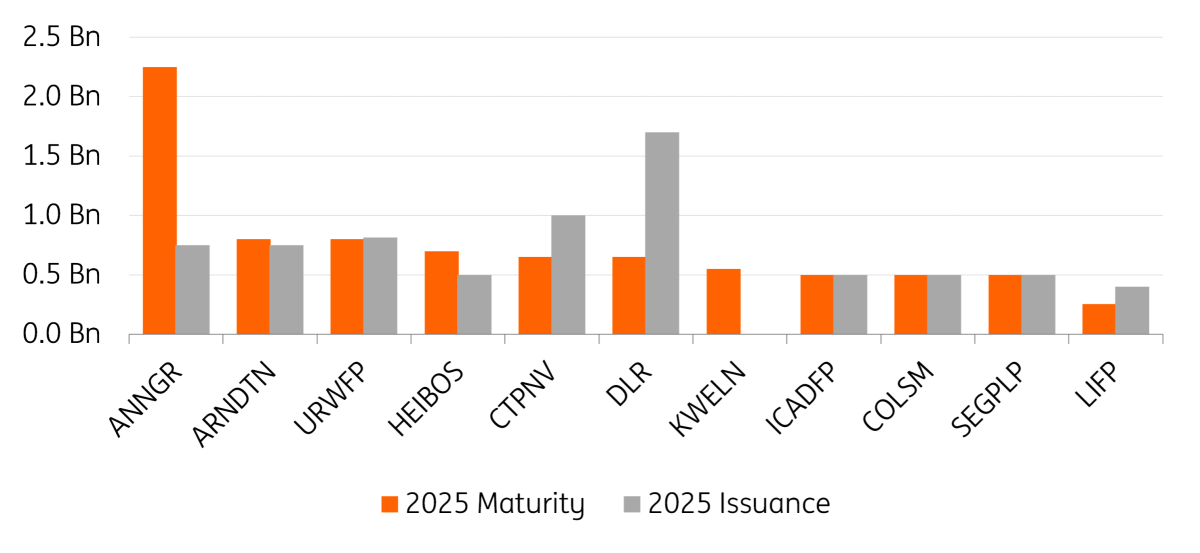

What we have seen with issuance so far this year is that most issuers with maturities in 2025 have now, by and large, already (partly) refinanced these, as the chart below shows. Of the larger issuers in the Euro real estate space, most have already come to the market this year. This suggests the focus could now start to shift to upcoming maturities in 2026 for the remainder of the year, as 2025 maturities are now less of a burden.

Most issuers may have dealt with their 2025 maturities (EURbn)

Bond market conditions have improved for real estate companies

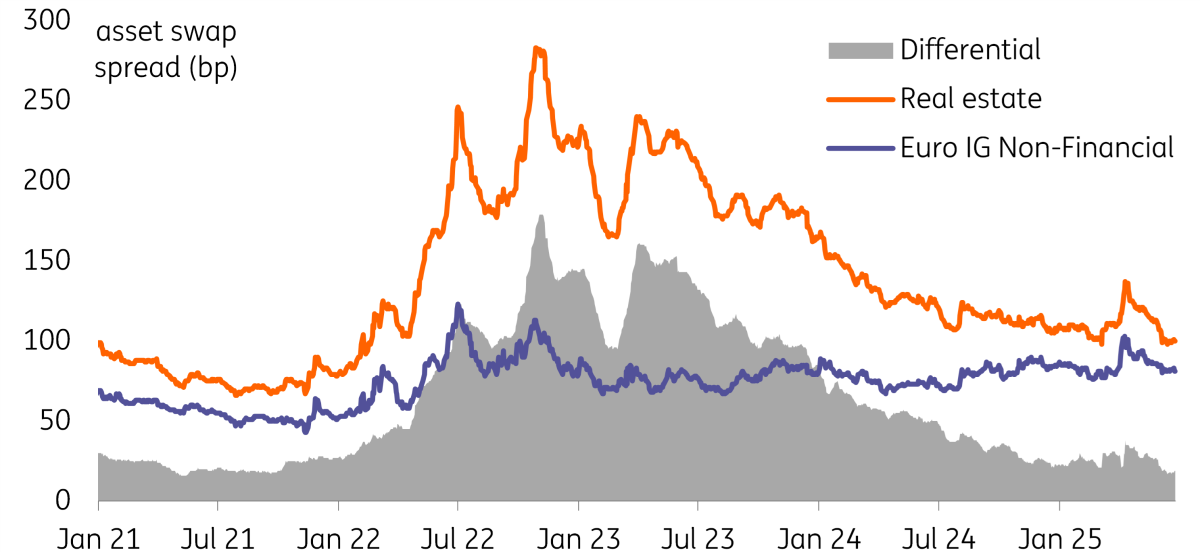

Funding conditions have improved further in 2025, with policy rate cuts from major central banks resulting in lower yields and swap rates. In addition, spreads have declined significantly for the sector and for most issuers. The real estate index asset swap spread is currently trading around 100 basis points, placing it only about 17bp wide to the overall IG Index, and 30bp tighter than the post-'Liberation Day' sell-off.

Real estate bond spreads now trade close to the broader market

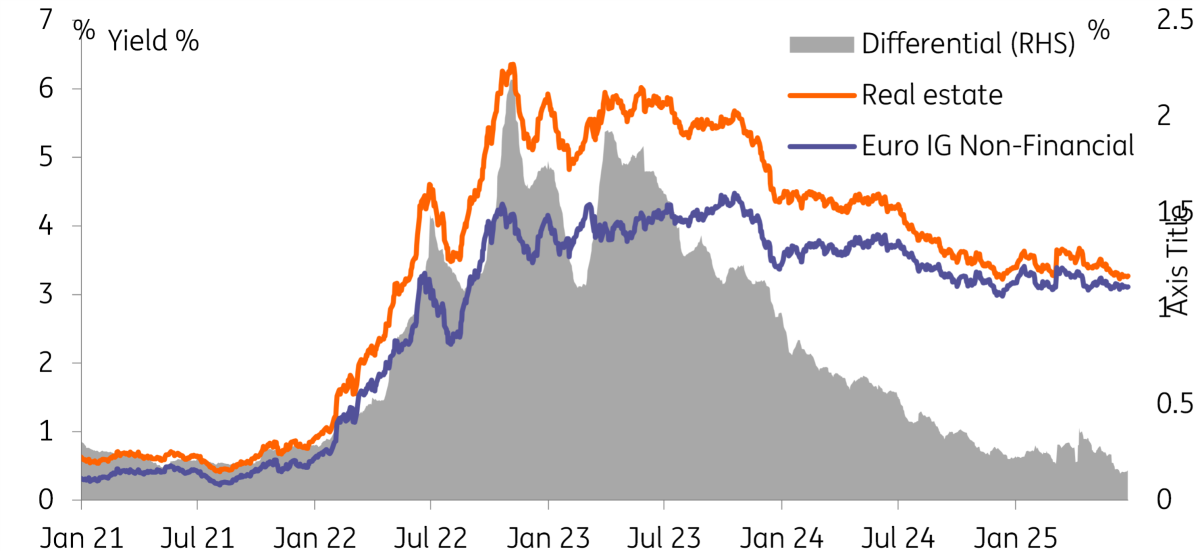

All-in yields (and thus average funding costs) remain quite elevated compared to the longer term, with the real estate index average yield standing around 3.25%. However, this is still a lot lower than the roughly 4.5% average yield since March 2022 as funding costs declined. However, real estate as a sector remains sensitive to higher interest rates, and many issuers will need funding costs to continue to improve in the coming years.

Real estate bond yields remain high, but have decreased significantly from the peaks in recent years

Solid green supply

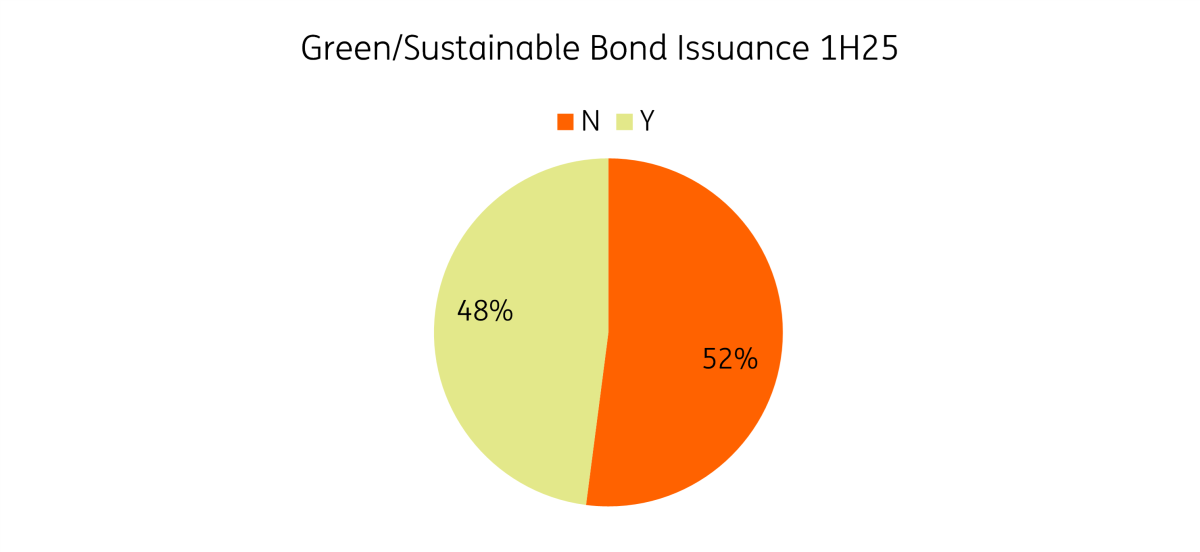

Last year, green bond supply surpassed “vanilla” bond supply for the first time. In previous years, green supply trended well below 50% of total supply but we do not think that 2024 was an outlier. And as expected, we have seen this trend continue in 1H, with roughly 50% of issuance being in a green or sustainability-linked format. This has also supported demand for bonds, as green bonds have typically come with larger order books.

Green bond supply at around 50%

Sustainability should remain a central pillar of real estate financing, driven by growing environmental concerns and evolving regulatory frameworks. An increasing share of capex is being allocated to ESG initiatives, as companies invest in energy efficiency and carbon footprint reduction across their portfolios. With investor demand for sustainable finance continuing to grow, and the sector’s strategic focus shifting toward long-term environmental performance, we see green bond issuance remaining a significant - and growing - portion of total market activity.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more