Rates: Terminal levels for the US and eurozone

At the beginning of every rate hiking cycle, there are two key questions: when will it start and how high will rates go? We use the forwards to help formulate terminal rate estimates, and the 2yr to help decide on timing. We find that the timing is far from imminent, but the forwards suggest there is quite a hiking job to get done in the years ahead

Rate hikes galore, but what about the US and eurozone

It’s been a remarkable few months as markets have collectively re-calibrated rate hike expectations higher, pushed there mostly by the persistence of inflation. Central banks spanning Norway to New Zealand have already hiked rates, as have a series of Latam ones. In central Europe the likes of Hungary and Poland, having been on an official rate downtrend over the past decade, have succumbed to the need to hike. And there are many others, including the likes of Czech, while the UK remains close to pulling the trigger.

The “when do we start?” and the “how much in total?” are key issues

But what about the US and eurozone? There’s certainly been a built-in rate hike expectations. But the “when do we start?” and the “how much in total?” are key issues. We have views on both questions, but there is also a market discount that can also present some answers. A starting point is what the forwards are discounting. Forwards are backed out of the shape of the current curve in the form of break-evens. These then represent unbiased predictions of how high rates are expected to go.

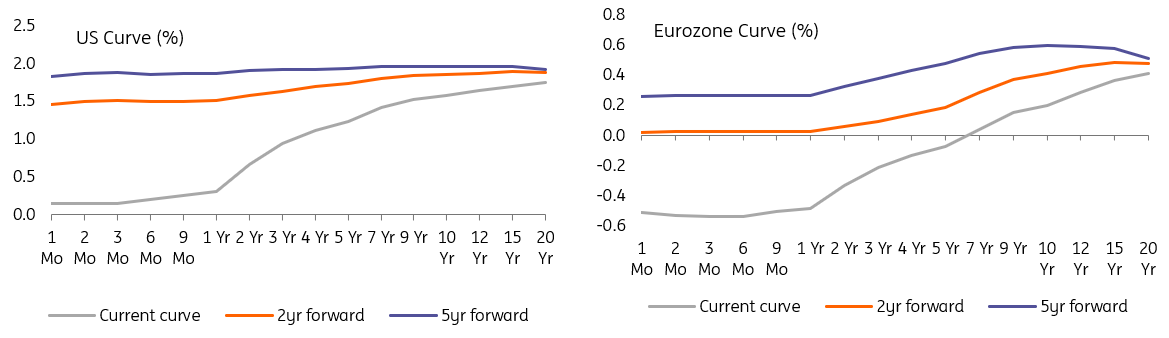

Market terminal rate for the US is 2%, and 70bp in the eurozone

There is a keen focus on the US, given how pivotal the Federal Reserve is. Here we find that the 5yr to 10yr part of the curve plateaus at around the 2% area in the forward space (chart below). The 5yr tends to get there 5yrs forward and the 10yr gets there at around 3yrs forward. There is then a flatlining at around 2%, practically no matter how far we go forward. This is as good a measure as any, of the terminal rate for the Fed funds rate.

The EUR curve is telling us that 70bp is a terminal rate discount for the ECB’s refi rate.

Performing the same analysis on the EUR curve shows that we need to go further out in the forward space to get to a flatline, and the implied terminal rate from that plateau is in the 60bp to 75bp range in the forward space (chart below). The 10yr in fact never gets much above 60bp, and the 5yr hits just north of 70bp when pushed 10yrs forward. Without getting too bogged down in specifics, it seems that the EUR curve is telling us that 70bp is a terminal rate discount for the ECB’s refi rate.

These are not far off our own predictions, where we see the Fed settling in the 1.75% to 2.0% area, while the ECB gets up to 75bp (both slightly above the implied market discount).

Current curves versus some forward ones

The US and eurozone compared

Why the 2yr rate is a good guide on what's really discounted

And what about the timing? Here we look at the 2yr rate. Why the 2yr rate? It is long enough to incorporate a robust view of where rates are heading to, without being too long where things can get quite fuzzy (the further we go into the future). In the eurozone, the 2yr swap rate is at -30bp. Even the 2yr rate set 5yrs forward is at just 30bp. If rates are really heading higher in the next few years, these valuations would need to be higher.

In the US, the rate hike discount is more pronounced, but still not dramatic. The 2yr USD swap rate is at 65bp. The 2yr forward rate is 100bp higher, at 1.65%. And we need to go to 5yrs forward to get to the 2% area. While there is a non-linear relationship between the level of rates and the shape of the curve, it does seem to us that the absolute level of front end rates remains low relative to where they could be, given where terminal rates are pitched.

Bottom line, the market discount is one where terminal rates of 2% and 70bp are operable for the US and the eurozone respectively. But the front end casts doubt on these, as front ends are not discounting an imminent increase in rates, and the longer it takes, the fuzzier the outlook becomes in terms of hitting those terminal rates.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

5 November 2021

ING Monthly: Curve surfing This bundle contains 11 Articles