Rates Spark: Words have (debatable) meaning

Whether and how does the ECB reflects its new inflation target in its forward guidance will be the main focus today. The aim is clear: providing more accommodation. A successful meeting would see lower rates for longer, and open a wider chasm with US rates.

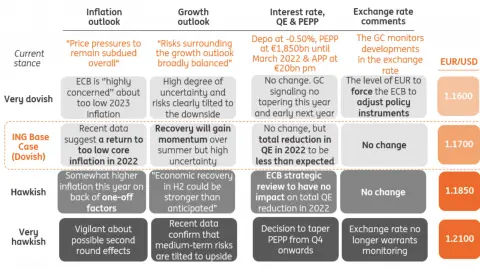

ECB: lots of noise and a dovish message

Today, the ECB has the first opportunity to revise its forward guidance, the promise not to unwind asset purchases and raise rates until inflation picks up, to reflect its new inflation target announced two weeks ago. To many, the symmetric inflation wording and promises of more forceful action when it undershoots sound familiar from past ECB communication. Perhaps the greatest change was the fact that the new wording was endorsed by the entire governing council.

It is fair to say that a change in forward guidance will prove more controversial. However, we are led to believe, through president Christine Lagarde’s public comments, and through ‘EC sources’ stories in the press, that it too will receive an update. The aim to make forward guidance clearer is laudable but we doubt it is achievable, as long as the ECB stops short of quantitative targets. The inclusion of words such as ‘forceful’ and ‘persistence’ would convey urgency but leave significant room for interpretation.

Rates markets will want to know how the new wording will translate into asset purchase amounts

What is clearer is that the aim of any change is to send a more dovish message. Rates markets will want to know how the new wording will translate into asset purchase amounts, and timing of rates hikes. We are unsure the ECB will go as far as spelling these out but, at a push, we think markets will understand new forward guidance as sign that APP (one of the two asset purchase programmes with PEPP) will receive a boost when PEPP is stopped in March next year. We already expected this but more dovish ECB comments should help more to come around to our view.

Market reaction: QE as far as the eye can see

Market reaction should be fairly straightforward, rates need to price purchases continuing for longer and outstripping supply for at least another year. The magnitude of the move will depend on how specific the ECB is in its forward guidance, and how explicit it is in flagging more APP purchases. With 10Y Bund yield flirting with 0.40%, only 10bp above the deposit rate, one can easily see that downside is limited. But what today’s meeting should achieve is reduce EUR rates’ ability to rise in tandem with their USD peers when the current gloom finally dissipates.

German yields are already low but the ECB could reduce their ability to rise alongside US rates

The alternative scenario is one where the ECB fails to agree on any change, or where these changes are so woolly that the market fails to draw any conclusion. This outcome would be slightly detrimental to risk assets in our view, as it would imply lower central bank support due to divisions. In the near-term, we also see this as a reason for EUR rates to remain pinned down, but this could leave them more leeway to rise when the economy picks up.

Today’s events and market view

The ECB policy decision and press conference are the main events today. In the US, the release of jobless claims and existing home sales will be the main focus. We expect a slight rebound in EUR yields after their July drop, as profit taking on tactical longs dominate price action. Markets can take a while to fully digest central bank decisions, especially when it comes to ambiguous forward guidance, but we expect lower and flatter curves in most scenarios (see above).

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

Rates DailyDownload

Download article

22 July 2021

It’s ECB day: What you need to know This bundle contains 5 Articles