Rates Spark: Where rates upside could come from

Yield curves are already consistent with the new hawkish message from central banks, so any rise in yields is more likely to come from economic data. Yields may well continue rising, to 4% for 10Y Treasuries, but this is set to come with a more inverted curve

Data is already in the price, as is the new more hawkish central bank reaction function

At the fundamental level, rates are currently driven by two forces. Firstly what the market’s current economic projections suggest is the appropriate path for policy rates in the future to bring inflation to target, and second what central banks suggest this path should be. Most of the time, these two estimates are very close to each other. It is worth remembering that in a “data dependent” setting where central banks are reacting to incoming data, efficient markets should quickly reprice with each important economic release, that is if central banks’ reaction function is clearly communicated and understood.

Market interest rates over the past few weeks have been driven by a reassessment in central banks’ reaction function

This point of the above reminder is to highlight that the retracement higher in market interest rates over the past few weeks has been driven mostly by a reassessment in central banks’ reaction function, especially in a context where the global outlook, for instance China's recovery, is dimming. Cases in point are the resumption of the Bank of Canada’s hiking cycle, or the Fed’s skipping the June meeting but communicating that more hikes are likely. From here, the question is whether the much-awaited Powell testimony tomorrow will deliver a further update to the Fed’s reaction function, or if markets materially differ from what the Fed sees as the appropriate path for policy rates.

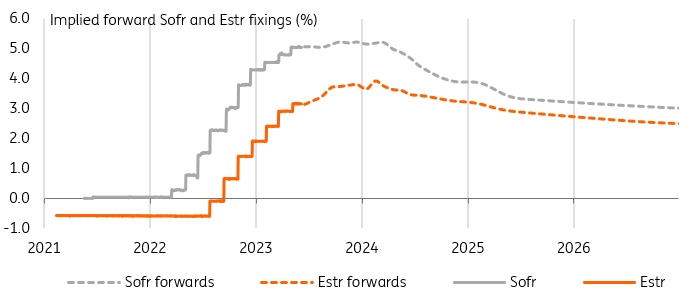

Dollar and euro swap forwards are no longer pricing cuts before early 2024

Not much mis-pricing for central banks to push back against

Rate cut expectations have all but disappeared from the dollar curve for 2023. Similarly, the euro curve doesn’t price a first cut before the first or even second quarter of next year. In our view, this counts as a communication success for central banks, and it reduces the mis-pricing (in their view) that they can push back against. The conclusion from this is that barring yet another central bank communication change, say Powell wanting more explicitly the curve to price two more hikes this year rather than one, any re-pricing higher in rates will be to be driven by the data. Similarly from the ECB, we do not get the feeling that the debate over a potential September hike is settled. Data to be released by the end of the summer, and another update to the Bank's forecast will be key, data-dependence in short.

Rate cut expectations have all but disappeared from the dollar curve for 2023

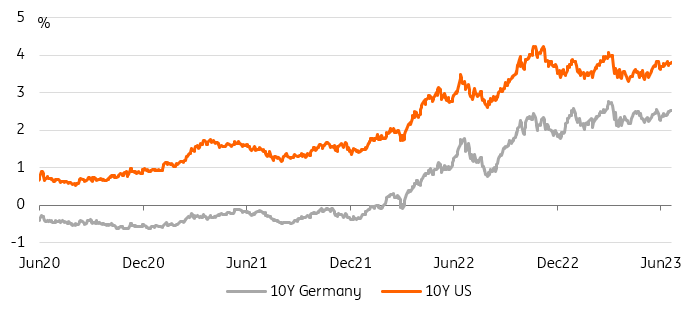

Of course one might simply disagree that current market rates accurately reflect the data. One such example is the very inverted state of the US yield curve when one compares 10Y Treasury yields, below 4%, to policy rates, above 5%. Inversion can persist if the market’s conviction is high that rates will be cut aggressively in the future. In the case of the Fed, but it is also true of the ECB, upbeat central bank economic forecasts explain their hawkish tone, while dimmer predictions from investors justify lower longer-dated yields. All this shouldn't prevent another sell off on long-dated bonds, for instance to 4% for 10Y Treasuries if the economic outlook improves, but it should all but ensure that another rise in yields will bring a more inverted curve until rates cuts are much closer in time.

Yields already reflect hawkish central banks, but also a dim economic outlook

Today’s events and market view

Economic data today consists mainly of the European construction output and US housing data, in the form of housing starts and building permits. The US session will also see the release of the Philadelphia non-manufacturing index.

There will be front-end bond supply from Europe, namely a 2Y auction from Germany, and a new 5Y launch from the UK.

In this relatively thin economic and supply calendar, central bank comments will be in focus. They include, among other, VP Luis De Guindos from the ECB and John Williams of the Fed. We argue above that with the recent flurry of central bank meetings, it is unlikely that market rates are too far away from where bankers would like to see them.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more