Rates Spark: US CPI looks sticky, but primed to fall

Monthly US core CPI is running at twice the Fed’s target, and looks sticky. But the upcoming pipeline number should look much better. EUR swaps are taking their cues from soft data and from USD markets more than from ECB hawks. We agree, and ESTR forwards should soon invert more

US CPI today, but take a glance at the pipeline numbers to come (much lower)

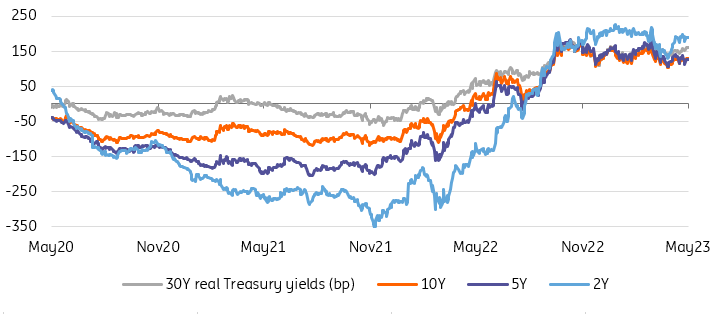

Today's US CPI data are set to confirm that the US remains a "5% inflation economy". Core inflation, at 5.5%, is runnning at above headline inflation, confirming its sticky nature. The month-on-month rates expected are also troubling, at 0.4%. Annualise those and you also get to a 5% handle. Yet the 10yr Treasury yield is at 3.5%, resulting in a large negative real yield. These data as a standalone place upwards pressure on Treasury yields, or at the very least, prevent them from falling.

Pipeline inflation pressure is more subdued than CPI implies

Interestingly though, the producer price inflation data due tomorrow should confirm that pipeline pressure is more subdued, with a 3% handle more dominant. In fact, the headline number is expected to be at 2.5% year-on-year for April. These are typically less correlated with Treasury yields, but at the some time point in a downward direction for inflation impulses ahead. Import and export prices due the day after are even more subdued.

So we'll start out with a reminder of how high inflation is at the consumer level, but then we'll have a snapshot of the future in subsequent days, as pipeline inflation impulses are in fact pointing down. That's a recipe for lower market rates, eventually.

Treasury yields are lower than current CPI but are well above inflation swaps

ECB hawks fail to move the needle

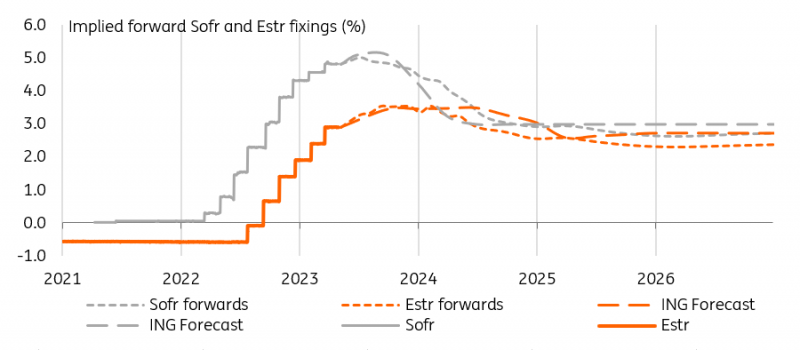

The most striking recent example of markets paying more attention to economic data than to central bank commentary is the failure of European Central Bank hawks to cause much of a re-pricing higher in policy rates expectations. Among others, Martins Kazaks tried to dispel the impression that rate hikes will stop in July, which is currently where the Estr swap curve puts the most likely end point of this hiking cycle. We think current market pricing of just under two more 25bp hikes is realistic, with our own call is for this cycle to end with just one additional hike in June.

There may well be a lag between Fed and ECB cuts, but no major policy divergence

To be fair, the most likely target of central bankers is the impression that the ECB will soon follow in the Fed’s footsteps and cut rates. For instance, Isabel Schnabel judged that rates cuts are "highliy unlikely for the foreseeable future". Similarly, Kazaks described this cycle in two phases: one where the terminal rate is reached, and one where rates are maintained at this level for as long as necessary. Markets and most ECB speakers seem to be in agreement about the former, give or take one hike, but the latter is harder to agree on. We side with the markets. There may well be a lag between Fed (we think as soon as the fourth quarter of 2023) and ECB (more likely around mid-2024) cuts, but no major policy divergence. The implication is that the inversion in 2024-25 Estr forwards should be more pronounced, in anticipation of cuts.

The truth is that, in the market’s psychology, the greater the conviction about a US ‘hard landing’, the more likely is Europe to be dragged into it. There is some logic to that reasoning. Investors can point to the weakness of recent data, for instance German factory orders and industrial production, as early evidence that Europe is not pulling ahead. More hawkishly-minded participants would, as Peter Kazimir another ECB official did, point out that inflation dynamics currently do not allow the bank to contemplate a pause. That mindset is likely shared by many of his colleagues, but the more aggressive the ECB is in hiking now, the more subsequent cuts the curve will price, and the more inverted Estr forwards will get.

Markets infer that the ECB will follow the Fed's cutting steps in 2024

Today’s events and market view

Most European data will come from Italy, in the form of industrial production and in the Bank of Italy and Istat monthly reports.

Germany will carry out auctions in the 30Y sector, on top of a 10Y UK gilt sale. In the afternoon, the US Treasury will sell 10Y T-notes.

The limelight will be firmly on the US CPI release. Monthly core inflation is expected to remain in the 0.3-0.4% range it has stabilised in since late 2022, roughly twice the monthly rate necessary for inflation to reach the Fed’s 2% target. Such a result is unlikely to be greeted with much joy across markets, but it would take a beat to get 10Y Treasuries above the top of their post-Silicon Valley Bank range, roughly around 3.6%. A further fall in PPI tomorrow may well bring dip-buyers.

The US President’s meeting with congressional leaders has not led to any progress on resolving the debt ceiling standoff, with the next meeting scheduled for Friday. In the meantime Moody’s sees the probability of a short breach at 10%, and also warned that a longer standoff no longer has zero probability.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article