Rates Spark: The 3%+ area targetted for the 10yr Bund

The ECB has cut by 25bp, and Europe is awash with the narrative of fiscal expansion leaving less room (or need) for monetary stimulus. US non-farm payrolls next. It's typically influential, but this time the market will look through a firm number, or, regard a weak number as validating current levels. So not expecting much impact. Still, got to be watched

The ECB cuts to 2.5%, and we now see only one more 25bp cut hereafter

The European Central Bank cut by another 25bp, bringing the policy rate to 2.5%, and President Lagarde now describes the stance as “meaningfully less restrictive”. If anything, the communication turned slightly more hawkish but the key word is “uncertainty”. With a flurry of headlines bringing volatility and uncertainty these days, we think the ECB will take a break in April and then only cut once more before summer, implying a terminal rate of 2.25%.

Markets are still set on a terminal rate of around 2%, and this is already 25bp higher than last week. With the data showing no signs of an economic deterioration and inflation numbers still on the sticky side, we think markets could continue trading in the range between 2% and 2.25% as the ECB’s new potential landing zone.

A fair value of 3% for the 10Y euro swap rate looks reasonable

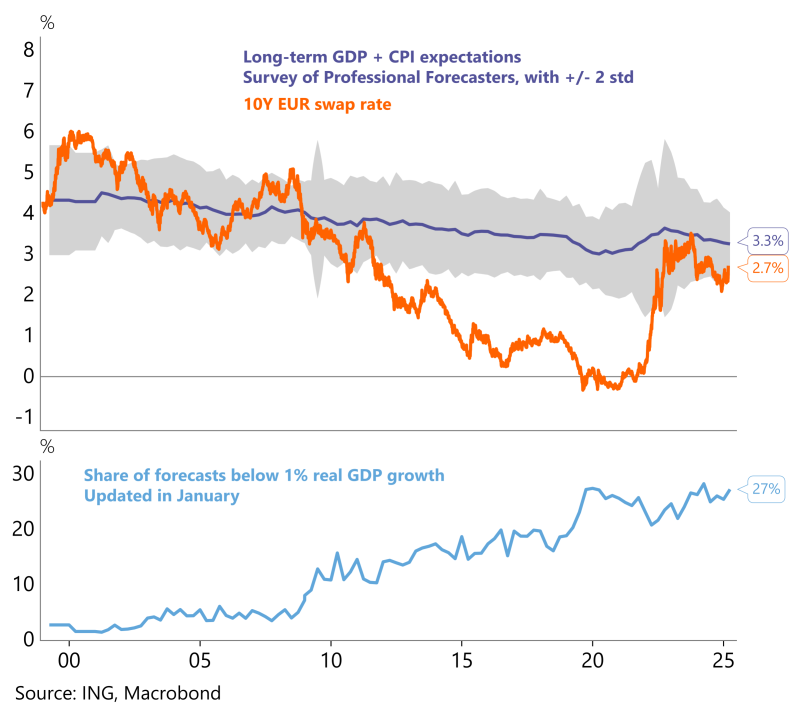

More interesting are the developments at the back end of the curve, which saw the 10Y swap rate rise another couple of basis points on the day. From a fair value perspective, we often look at long-term nominal growth expectations as an anchor point for 10Y rates. The ECB’s Survey of Professional Forecasts would imply a 10Y rate of around 3.3%, and these numbers were even from before the grand spending announcements of this week. So whilst the current 10Y swap rate of 2.7% looks high compared to last week, the number may not have peaked yet.

Since the secular stagnation period after the Global Financial Crisis, markets have been more wary about Europe’s growth outlook, but this may be about to change. If markets start pricing out the downside risk of returning to a low growth, low inflation environment, then we could see euro rates easily rise further. In the last survey, around a third of forecasters still foresee a real GDP growth rate of below 1%, but this share could quickly diminish on the expectation of broad-based European spending initiatives. We are sceptical all spending promises can materialise, but if the headlines keep giving, and the data doesn’t disappoint, a 3% target for the 10Y swap rate seems reasonable.

Long-term growth expectations provide an anchor for 10Y rates

Friday’s events and market view

For a change, the main focus should turn to the US again with the release of the US payrolls data. The consensus forecast is for a rise by 160k in February after 143k in January and for the unemployment rate to remain at 4%. Bloomberg’s ‘whisper’-number at 120k points to some downside risk. In the wake of the jobs data markets will also be watching a number of Fed speakers, with the list starting at Bowman, Williams and Kugler and ending with Chairman Powell.

Central bank speakers will also be one focus for European markets after Thursday’s ECB rate cut decision. Lagarde will speak, but also Nagel and Knot from the more hawkish spectrum of the Governing Council.

Primary markets will be quiet with Belgium conducting a reverse inquiry auction.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

Rates DailyDownload

Download article