Rates Spark: Swap spreads on the move in opposite directions

The spread between UST and swap rates has narrowed significantly since January, but Bund-swap spreads showed little correlation with the moves. Lots going on in this space. Meanwhile, Treasury yields have found a way to block out Wednesday's CPI reading, implicitly balking at the notion of shooting higher, at least not for now

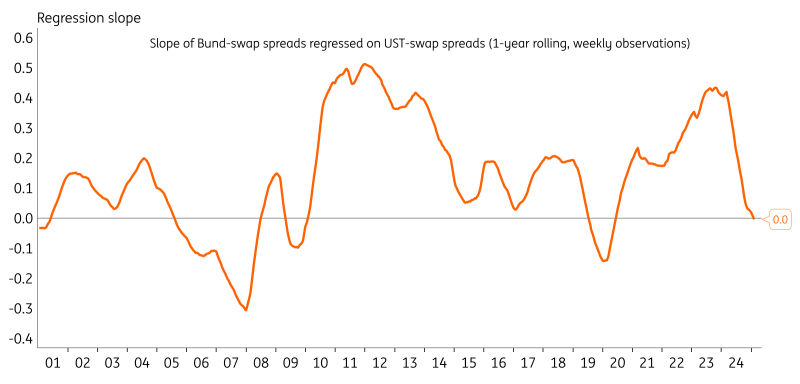

UST-swap spreads tightening might not mean much for the eurozone

Whilst the gap between UST yields and SOFR swap rates has narrowed significantly since January, the Bund-swap spread has been moving in the opposite direction. This is in contrast to broad patterns observed before: Since 2023, the direction of swap spreads have moved in the same direction, whereby the ongoing quantitative tightening programmes of the European Central Bank and Fed together added to the supply pressures of government bonds.

Looking at weekly changes, however, the correlation is now close to zero (see figure below), suggesting that changes in swap spreads have little spillover to other jurisdictions. The tightening gap between UST and SOFR rates may therefore leave little mark on swap spreads in the eurozone going forward. The shared narrative no longer holds.

If anything, the trends can actually continue in opposite directions. The tightening in US spreads can be attributed to recent remarks by Fed officials about possible banking regulation adjustments, which would give banks more balance sheet capacity to deal in USTs. Furthermore, DOGE’s initiatives could convince markets of lower government deficits, which would also help UST yields lower versus swaps.

Meanwhile, Bunds will stay under pressure versus swaps. German elections add uncertainty to the political outlook, including the possibility of easing the debt break. This would bring additional issuance expectations on top of already high supply pressures, pushing Bund yields relatively higher. In other news, a peace agreement between Russia and Ukraine could give some risk relief, reducing the bid for Bunds as a safe haven, although this could depend on the conditions of the plans. Thursday actually saw Bunds outperforming swaps.

Correlation between UST and Bund swap spreads low, suggesting limited spillovers

US Treasuries find a way to break lower in yield, mostly on a Ukraine resolution thesis

In the US, the headline PPI report was undoubtedly firmer then expected, and firm in absolute terms (although the elements that filter into PCE were broadly less poppy). Basically PPI inflation is running in the 3.5% area, and the month-on-month readings for January are annualising in the 4% area. PPI is actually not a big market mover, typically. But on the heels of the pop in CPI, a reaction higher in yield would have been understandable. But Treasuries have had other things on their mind. The market is looking at wider circumstances, which include a ramped-up tariff narrative, a “resolution” in Ukraine, DOGE, moderate dollar weakness and a resistance for now to really break higher in yield.

The market has absolutely latched on to a "Ukraine war resolution" outcome (even if it’s a hold your nose result). The reciprocal tariff announcement is also impactful, but cuts two ways. Higher tariffs mean higher prices upfront, but down the line can hamper growth. Impact reaction from tariff news has tended to pull yields lower. However, once this begins to show up in inflation metrics this can easily swing in the other direction. The US 10yr continues to find comfort in the 4.5% area, and area that we consider to be broadly neutral i.e. not pricing in a material inflation and/or fiscal deficit upside risk. Should such risks fail to be downsized in the months ahead, then the pressure re-builds for higher yields in due course.

Friday's events and market views

From the eurozone we have the second estimates of GDP growth for the last quarter of 2024. The initial estimate was zero growth, which consensus sees being repeated. The US will publish data on retail sales, import prices and industrial production. Not top tier data, but of interest nevertheless.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

Rates DailyDownload

Download article