Rates Spark: Some encouraging signs for the ECB

Contained inflation swaps and peripheral spreads suggest the European Central Bank is not in as tough a spot as most fear. These are still early days and we think the ECB will have to deliver both on hopes of a spread management facility, and on the hikes the market is pricing this year. Question is: will it make enough progress this week?

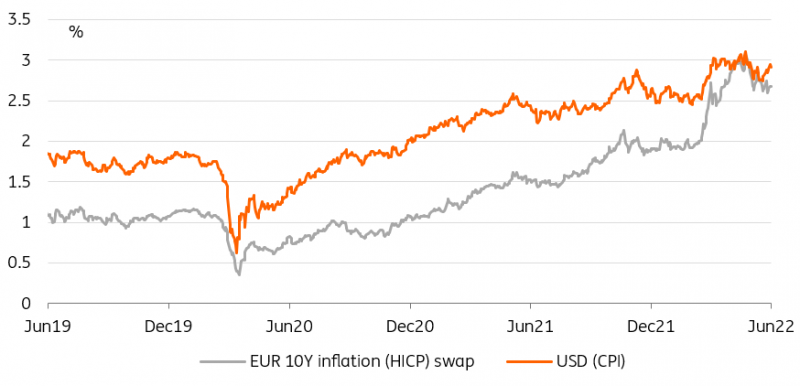

Early signs of inflation swap divergence

The past few sessions have delivered a head scratcher in the form of diverging long-term inflation swaps in the US and eurozone. At face value, this runs counter to the thesis that eurozone inflation is less under control due to the ECB being further behind the curve than its US counterpart. So far, markets were under the impression that by acting aggressively, the Fed managed to keep a lid on inflation expectations and thus on long-end rates. 10Y US CPI swaps crossing the 3% threshold (although break evens remain below that level at around 2.7%) is likely to give the Fed some sleepless nights, and would imply a more hawkish rhetoric going forward.

EUR inflation swaps suggest the ECB is more in control than it looks

Even long-dated swaps tend to trade on short-term developments

At the ECB, we are inclined to attribute the drop in inflation swaps to the sharp re-pricing of ECB hike expectations. In a sense, this is a questionable assumption given that much of the eurozone’s inflation is externally-generated, but even long-dated swaps tend to trade on short-term developments. There is also a growing assumption in financial markets that second order effects will add to inflation pressure. Ironically this also comes at a time the EUR yield curve remains stubbornly steeper than its USD equivalent both now and where it was at the same time into the Fed’s hiking cycle.

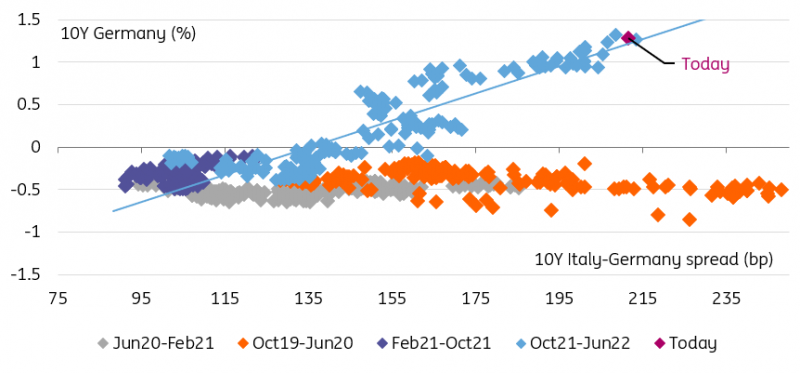

At least one corner of the rates markets is showing some optimism

Meanwhile, Italian bonds are on a tear. There was little reaction on Monday to reports in the Financial Times that not only is there a proposal on the table at the ECB to prevent market fragmentation (central bank speak for a widening of credit spreads, especially in government bonds), but also that a majority of the governing council is ready to support it. It is hard to attribute the subsequent tightening to hopes of ECB intervention given the time lag. And yet, we’re inclined to think prospects of ECB intervention (or not) hold the key to near-term sovereign spread developments.

Peripheral spreads tend to widen when yields rise

Warm words from the ECB tomorrow would go some way towards calming spreads volatility

Warm words from the ECB tomorrow would go some way towards calming spreads volatility but we doubt they will be enough to convince private investors to return to peripheral bond markets in droves. When net purchases stop, the shortfall in demand will have to be made up by investors in the private sector. This is not impossible but the best way to convince them to is to reduce the risk associated with the peripheral bonds, or to offer greater yields. In the long-term, a more unified EU economic and fiscal architecture could achieve that risk reduction but, in the near term, the burden falls once again on the ECB’s shoulders.

Today’s events and market view

There is little on the events calendar so far this week but this hasn’t prevented rates volatility from picking up a notch. We think the approaching event risks, in particular the ECB, could prompt a short-covering rally in the coming days but a resumption of the yields upside looks inevitable as long as the global growth outlook holds.

Markets will have one last day of low apparent event risk tomorrow before Thursday’s ECB and Friday’s US CPI. The main data release will be the final reading of the eurozone’s 1Q GDP. This being the third iteration, chances of a surprise are relatively limited. In the afternoon, investors will look to MBA mortgage applications for further signs of a slowdown in the US housing market.

On the supply front, Germany and Portugal will sell bonds in the 10Y sector. This will be followed in the US session by the Treasury selling 10Y notes. On the other side of the bid-ask spread, Italy’s treasury will buy back short-dated bonds today.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

Rates DailyDownload

Download article