Rates Spark: Relentless and potentially dangerous

- 21 October 2022

- Rates Spark

Pressure continues to build on market rates, as they ratchet higher in a relentless fashion. That can be dangerous, as we can easily face circumstances where something breaks. The UK had a brief taste of this. But even there, the odds are that gilts too re-engage in the 'pain trade' of higher market rates and tighter conditions. The US 10yr is eyeing 4.5%

The US 10yr has a pathway to 4.5%, but is held back by capital inflows

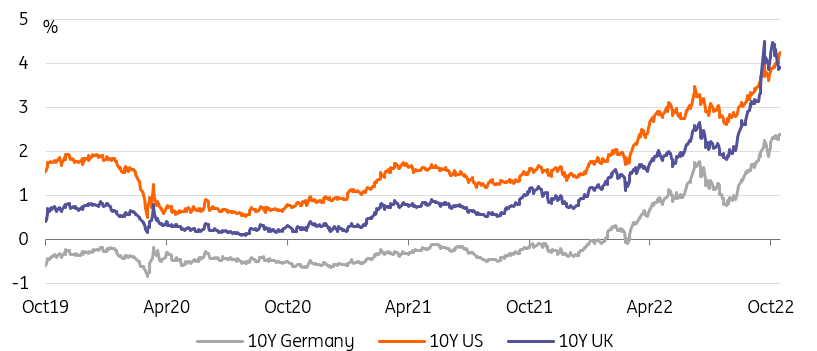

The separation between UK gilts and US Treasuries has been quite stark. In fact, it’s UK gilts doing their own thing as Treasury yields and Bund yields just continue to shoot on higher. The 10yr US Treasury yield in the area of 4.25% and the 10yr Euribor rate in the 3.25% area are quite some levels, and the trend for yields remains to the upside.

UK gilts are now trading back below Treasuries as the outlook for the UK darkens, even as the smog of the political landscape clears. These are remarkable times where the market abruptly stepped in recently to punish policy mistakes in the UK, but has tended not to do the same in the US and the eurozone where arguably some mistakes have also been made (albeit not as stark). But the UK is suffering from a very poor track record, and sterling is no dollar. Even the euro is managing to trend firmer versus sterling (big picture).

Capital flows are and will be a driver ahead

The fact that global FX reserves have a 7% weighting in sterling is anomalous given the 3% weight of the UK in global GDP (approximate rounded numbers). Times are a-changing for the UK. For the US the mighty dollar remains everyone else’s problem and is reflective of net capital flows; it’s also containing the rise in US Treasury yields. Had it not been for the buffer being offered by the flight into Treasuries and US assets (in a relative sense), Treasury yields would be much higher than they currently are.

With the effective fund rate now discounted at 5%, there is a path for the US 10yr to get to 4.5% (with 50bp through at the extreme in the past, when the funds rate peaks). It does not need to go much above this, provided the terminal rate discount does not continue to ratchet higher, and there are no guarantees there.

Forget the gilt rally, bond yields are heading up globally

UK in the headlines, but no longer in the driving seat

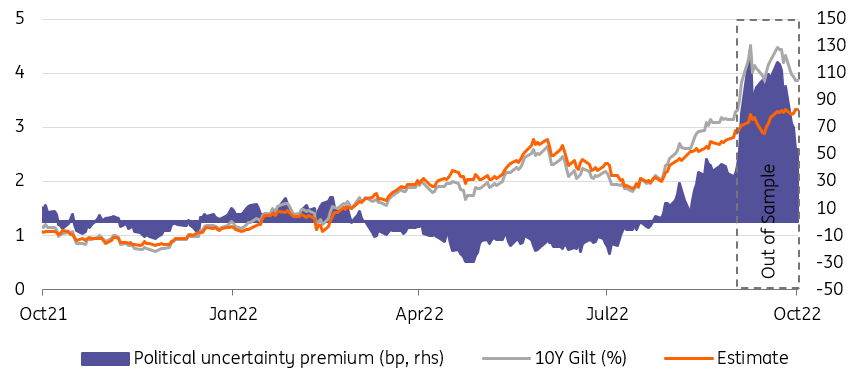

The UK remains in the headlines with prime minister Truss announcing her resignation yesterday and the governing Conservative party heading for another leadership contest. With thus some uncertainty still surrounding the fiscal plans, gilts should continue to trade with a risk premium. Any further retightening versus Bunds looks set to be much slower. The 10Y spread between gilts and bunds has already tightened from levels around 215bp last week to 150bp following the latest developments. This is still above levels in late August/early September before the spike in gilt yields.

Long end yields should struggle to remain below 4%

But as politics start to emerge from their turmoil gilts will increasingly focus on the Bank of England’s reaction. Currently, markets are still seeing the Bank lifting the key rate above 5% before the middle of next year. That being the case will also mean that long-end yields should struggle to remain below 4%.

There's still a risk given the political backdrop that the BoE won't have all the information on fiscal plans when it decides on rates in November. Such feared lack of clarity may help explain why money market pricing has not dropped more on the back of dovish comments coming from the bank's Broadbent yesterday, who clearly said he thought market pricing was overdone. Our own economists think that the Bank Rate could top out at 3.5% to 4%.

There is still a 50bp political risk premium in gilts but it won't go away easily

inflation versus recession angst enters the next round

At the forefront of the inflation-fighting charge next week will be the European Central Bank, which is seen hiking 75bp and perhaps also setting in motion first plans to start shrinking the balance sheet. But they will also follow the Bank of Canada’s decision, which should underscore that the hawkish push is a global phenomenon. A larger 75bp hike looks more likely here after a recent upside surprise in inflation.

The Fed meeting is still a week further away, but here US money markets have for the first time started to price a terminal rate of 5% for the Fed Funds effective rate. To be sure, the market is still pricing the Fed turning towards cuts later next year, but Fed officials are pushing against that notion. The Fed’s Harker stated that it could hold hiking in 2023. But this is more to assess whether policies have the desired impact on inflation as he remarked the Fed could then tighten further if needed; one cost being that he sees unemployment peaking at 4.5% next year.

Near-term data is unlikely to deter markets from continuing to price a hawkish Fed

Near-term data is unlikely to deter markets from continuing to price a hawkish Fed. The 3Q GDP data next week should show positive growth again after the technical recession of the first half of the year. The Fed’s preferred inflation measure due for release next week should reflect the upside surprise already witnessed in the CPI data.

As for the eurozone, the PMI data next week as well as the German Ifo index later in the week should provide evidence of the economy having slid further into contraction. The ECB’s new reaction function has made clear though that the fight against inflation may come at the cost of recession. While market participants will always question how far this notion can be pushed, we doubt that they are in the position to focus on the long-term picture just yet. Market volatility remains high and the outlooks for both inflation and growth are still shrouded in great uncertainty. In the upcoming round of inflation versus recession angst, inflation looks set to maintain the upper hand.

The odd one out among next week’s central banks is the Bank of Japan which is largely seen to stay put, sticking with asset purchases and its yield curve control programme. But with inflation hitting 3% for the first time in three decades the pressure on the bank to eventually reduce stimulus is increasing.

Today's events and market view

Near-term upside to rates should dominate. In the upcoming round of central bank meetings, kicking off with the ECB next week, inflation angst should still maintain the upper hand in determining policy action and communication.

Eurozone PMI data at the start of the week pointing to deepening economic woes as well as month end – note that the German debt agency’s increase in own holdings will also be reflected in the month-end rebalancing of index trackers – can provide some support to rates markets. But that may prove fleeting as the focus then turns to the Fed and BoE.

Eurozone consumer confidence is one of the few data points to watch today. In the US the Fed's Williams and Evans are scheduled to speak.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more