Rates Spark: Rates price out systemic risk, but unevenly

As optimism grows that the worst of the banking crisis is now behind us, we look at the uneven pricing of systemic risk across rates markets. Euro swap spreads appear ripe for a retracement through the levels prevailing in early March

Optimism grows, and rates continue to climb

Every day that passes reinforces the market’s, and our, conviction that a line has been drawn under systemic banking worries (individual travails are another matter). We need to be as careful as possible when writing this because turns in market sentiment in recent weeks have been sudden and violent. Still, with markets having spent that last three weeks looking for hairline fractures in every bank’s balance sheet and business model, there is a case to be made that a large number of closets have already been checked for skeletons.

Markets now need to factor in a greater likelihood of a credit crunch in their forecast

Of course such statements only apply to near-term liquidity risk of individual banks. What remains, as the dust settles, is greater macroeconomic angst. Markets now need to factor in a greater likelihood of a credit crunch in their forecast. Given already downbeat answers to the Fed’s senior loan officers survey, we’re in the camp of those expecting a further contraction in credit.

This shouldn’t prevent the curve from pricing one more hike in May, however. Similarly periods of calm, after the banking turmoil but before data reflects more tense lending conditions, should cause markets to doubt the number of cuts the Fed can deliver this year. We think they will deliver them, but that transition period may well feature one or more pull-backs higher in rates before the final descent, once Fed rates peak and cuts come into view. We hoped this would take the 10Y above 3.5% this week. That line has been crossed on Monday. Can we go to 3.75%? Entirely possible but we need an assist from data, for instance in case of an upside surprise to the February PCE released this Friday.

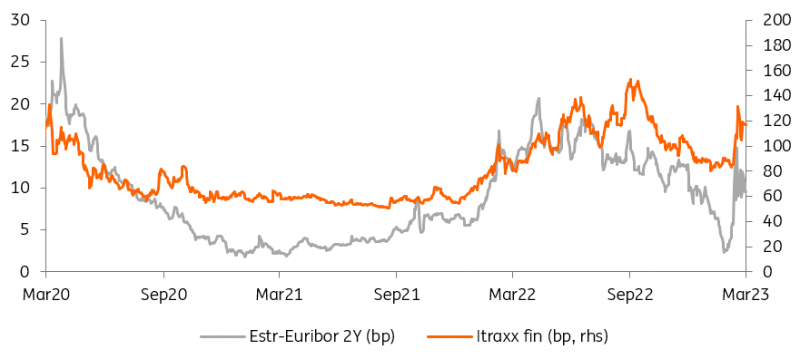

European systemic stress indicators didn't even rise above 2022 levels

European markets have more risk premia to shed

The eurozone has managed to stay in the periphery of banking worries, even at their worst, and we hope this will remain the case. Broader systemic stress indicators never got to critical levels in Europe, especially in money markets (the chart above is showing the Euribor-Estr basis compared to the Itraxx Fin CDS index). Some of the credit has to go to the swift intervention of regulatory authorities and central banks, for instance through dollar liquidity injections. Provided sentiment continues to recover, there is more room for risk assets to shed their risk premium, especially if they are only loosely related to the epicentre of the crisis.

Broader systemic stress indicators never got to critical levels in Europe

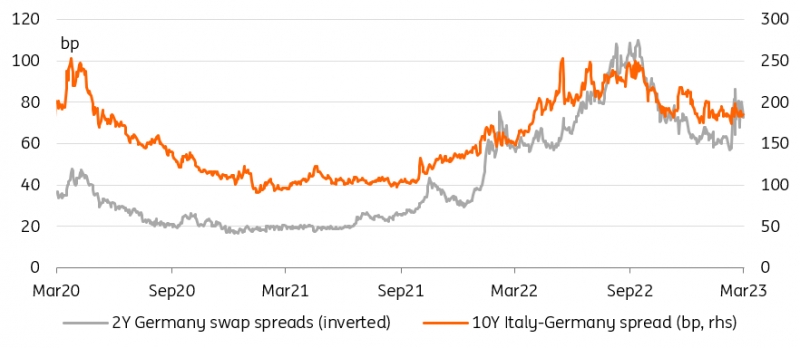

We feel this way about sovereign spreads, for instance the yield differential between 10Y Italian and German bonds, and swap spreads, the difference between bond yields and swap rates. The former didn’t even rise to 200bp, a level long considered the floor in a period of aggressive monetary tightening. The latter did jump (the chart below shows swap spreads at the 2Y point in inverted values, meaning a positive number denotes German yields being below swap rates), presumably in anticipation for the demand for safe collateral. Whilst there are still some fears of collateral scarcity, which caused the late 2022 widening in swap spreads, we think this issue has largely been addressed by the European Central Bank and national treasuries. Swap spreads are a prime candidate for mean reversion as systemic risk gets priced out of the system in our view.

Swap spreads are a prime candidate for retracing their systemic stress widening

Today’s events and market view

Greece has mandated banks for a 5Y syndication, which should take place today. The US Treasury has a 7Y T-note auction scheduled today.

In the current market environment, the Bank of England’s financial stability summary is likely to get more attention than usual, so will Michael Barr’s testimony before the House financial services committee. It is perhaps coincidental, but the string of testimonies from the Fed, BoE, and ECB this and last week have come with an improvement in sentiment towards banks (if one puts the uncertainty about potential FDIC support to large depositors to one side), perhaps these two events will support the recovery further.

The data calendar is relatively light, with UK mortgage approvals and US pending home sales.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more