Rates Spark: No peak rate in Europe, not yet anyway

The Fed did what was discounted, and the challenge now is to prevent market expectations for cuts from going too deep. We find that low inflation breakevens support cuts, and we still expect these in 4Q. The ECB tightening cycle will continue after today’s 25bp hike. If calls for Fed cuts are right, USD-EUR rates convergence should reverse late this year

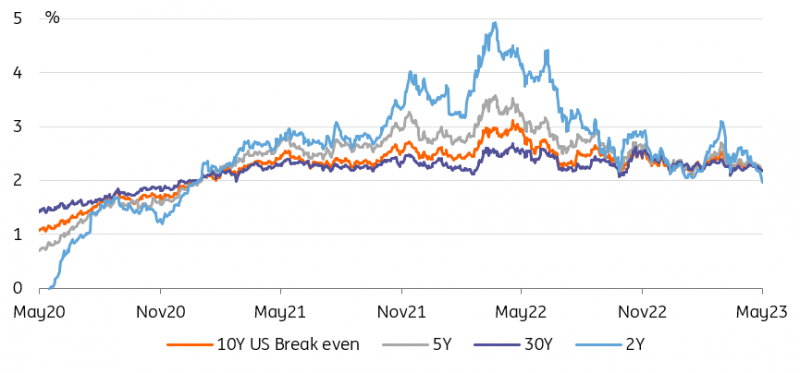

Market breakeven inflation rates support a Fed pause here, and indeed support future cuts

The impact reaction to the FOMC outcome was more downward pressure on market rates, driven by lower real rates, as breakeven inflation rates have edged higher. But that morphed into upward pressure on market rates, dominated by rises in breakeven inflation. This is an interesting reaction, suggesting a rise in market inflation concern remains in the period ahead. At the same time, the 10yr breakeven inflation rate at 2.2% is at a very tolerable level, impliedly discounting a return to 2% inflation. It's even more striking when you look at the 2yr breakeven, which is now at 2.05% and looking like it could dip below 2% if it keeps up the pace of decline seen in recent weeks. These breakeven trends support the Fed pause, and indeed provide room for eventual cuts, should delivered inflation actually trend towards the breakeven expectations.

The 10yr breakeven inflation rate at 2.2% is at a very tolerable level

We also note that all rates are up 25bp, including the rate on the reverse repo facility, now at 5.05%. Also the rate on the standing repo facility is up to 5.25%. And the rate on excess reserve is up to 5.15%. So no surprises there. All bands have been kept intact right through the rate hiking cycle. The Fed has concentrated on getting all rates higher throughout the process as opposed to any finessing of the different rates that it employs to manage other aspects of policy. Meanwhile, some US$3trn remains in bank excess reserves at the Fed and over US$2trn continues to go back to the Fed on the reverse repo facility. These are measures of the ongoing elevated size of the Fed’s balance sheet. The Fed’s reversal policy here also remains as was, as it continues to allow some US$60bn of Treasuries and US$35bn of mortgage backed securities to roll off their balance sheet on a monthly basis. That also tightens conditions.

No material directional impulse from this outcome. We continue to view 3% as a medium-term level that market rates can aspire to getting towards. The 10yr yield should get there first, while the 2yr will be constrained by Federal Reserve reluctance to nod towards cuts too soon. The 5yr area of the curve should remain quite rich in the months ahead, as the inversion on the 2/5yr segment remains deep. That will change later in the year though as the 2yr finally becomes untethered from the fund rate as cuts are more clear and imminent.

Falling break-even inflation is a comforting sign for the Fed as it signals a possible pause

ECB: Inflation outlook in lieu of forward guidance

Economic data of late, disappointing first quarter growth and tighter lending conditions, allow the European Central Bank (ECB) to ‘downshift’ from a 50bp hike in March to 25bp today. This is not to say the inflation fight is over. There isn’t much cause for celebration in the most recent inflation report and the central bank very much remains in a tightening mode. We don’t expect it to give much indication on its next policy steps, but inflation worries should make it clear enough that at least one more hike is needed after today.

Inflation worries should make it clear enough that at least one more hike is needed after today

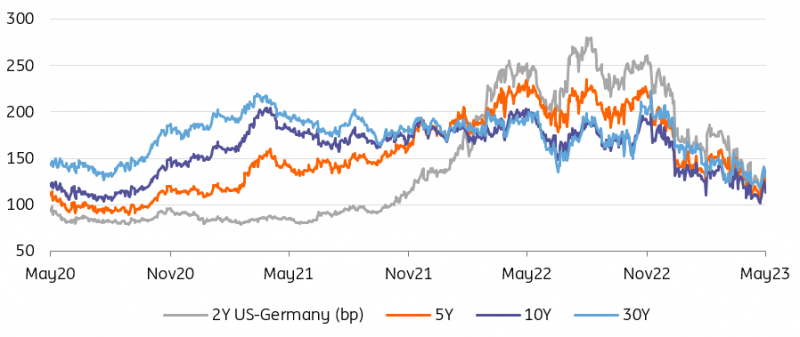

It will also be interesting to see how prominent is the debate on the speed at which policy tightening is reaching the economy, the famed 'transmission mechanism'. Judging by the most recent Bank Lending Survey (BLS), the answer seems to be fairly quickly. One should be wary of relying on a single indicator, however. This will take time to affect inflation in any case and, in the meantime, the ECB can ill afford a dovish policy error. This is the key reason why we see the differential between US and European policy rates narrow this year.

US-Germany yields differentials can keep tightening for a few more months, until the Fed starts cutting

The Fed and risk appetite as breaks on the ECB’s ability to hike

It is an open question how much longer euro rates can decouple from their dollar counterparts, however. There are historical precedents where the ECB’s hiking cycle went on for around a year after the end of the Fed’s (in 2006-2007), but the more severe the recession in the US, and so the greater the contagion to Europe, the shorter that lag. Rates convergence looks set to continue over the coming weeks and months, as 10Y Treasury yields dip towards 100bp above Bund, and is now more than 12bp below that of 10Y gilts. Our guess is that once Fed cuts become a reality, it will be difficult for the euro and sterling curves not to price more rate cuts.

Once Fed cuts become a reality, it will be difficult for the euro and sterling curves not to price more rate cuts

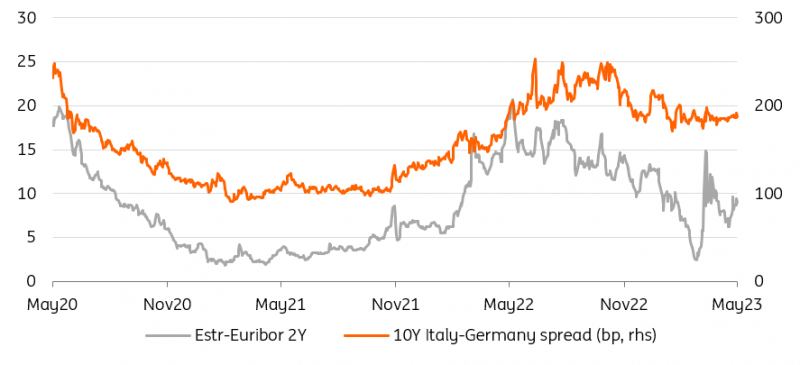

Besides the Fed, another important factor on the ECB’s next policy steps will be how risk appetite develops. Sovereign spreads have got over the ECB’s tightening, with realised volatility at its lowest level in a year. Other indicators of financial conditions, for instance money market spreads, send a similarly sanguine signal, despite recent banking worries. In a special question as part of the BLS, banks responded that the ECB’s bond portfolio is contributing to a worsening of their liquidity position and of market financing positions. This might give the ECB pause as it nears a decision on a potential acceleration of quantitative tightening (QT), currently running at a modest €15bn per month.

Sanguine sovereign and money market spreads might embolden the ECB to accelerate QT

Today’s events and market view

European services PMIs will set the stage for today’s ECB meeting. Only the Spanish and Italian ones are first readings. The picture, judging by consensus estimates, is still one of ongoing expansion (in contrast to the manufacturing sector). Eurozone PPI is expected to confirm the dis-inflationary trend.

The ECB is not the only central bank on the calendar - the Norges Bank will meet in the morning.

Bond supply will come from Spain (3-7Y and linkers) and France (10-50Y).

Our call for the ECB is to hike rates by 25bp hikes but amid vocal hawkish pushing for a larger 50bp move. There was little to celebrate in the recent inflation data but the tightening of credit conditions might feature more prominently in its outlook following the result of the recent BLS.

US data won’t be any lighter with Challenger job cuts, trade balance, jobless claims, productivity, and unit labour costs.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

Rates DailyDownload

Download article