Rates Spark: Tactical re-flattening risk parameters

- 22 September 2020

- Rates

Sentiment is deteriorating fast and we expect risk appetite to be dampened by the approaching US elections. 30Y USD stands to benefit the most from risk adverse investors, and by dwindling yields elsewhere. Steepening remains the dominant underlying impulse, but this risks temporarily fading to flattening as we get closer to the US elections.

Dark electoral clouds on the horizon: election-centred flattening risk on the USD curve

When investors look back to 21 September 2020 in a few weeks’ time, they might identify the date as the day the election became the most prevalent worry among investors. Granted, there are plenty of other risks on the horizon that justify a bull-flattening, including waning fiscal support in the US, and rising covid cases globally. We think appetite to fade these risks will be diminished due to the looming election, and necessity to reduce risk exposure by that date.

One should also note that scant chance of fiscal support before the new administration is sworn in means the Fed is ‘the only game in town’. In the past, monetary easing on its own, especially stuck at the lower bound, has resulted in flatter yield curves.

So what is the upshot for rates markets? Firstly, under the Fed’s new forward guidance, the curve is likely to push even further out the date of the first hike (it is worth remembering the last cycle saw no hike for a whole 7 years after the final cut). This isn’t relevant for the first 4-5 years’ worth of expectations since hardly any tightening is priced by then, but the 5-10Y sector would see rates dive even lower.

The second order effect is also likely to be the most significant. Faced with ever lower yields on government curves (this is not a phaenomenon specific to the US), investors would search for yield further up the curve. Similarly, those relying on US Treasuries for diversification purposes would likely target the only section of the curve where volatility remains: the long-end.

| 35bp |

USD 10s30s to revisit their August low...likely requiring 30Y USD sap rate to drop below 1% |

This is no departure from our long-term view that a more dovish (on balance) Fed does justify a greater inflation premia on the USD curve, and that supply pressure will push long rates in the same upward direction. That dynamic is merely likely to be interrupted temporarily by the accumulation of near term event risks.

As a result, we would not be surprised to see USD 10s30s re-visit their August lows around 35bp, likely by the time of the US elections. This would likely require 30Y swap rates to dip below 1% but would be justified by a hunt for yields as global curves are compressed once again.

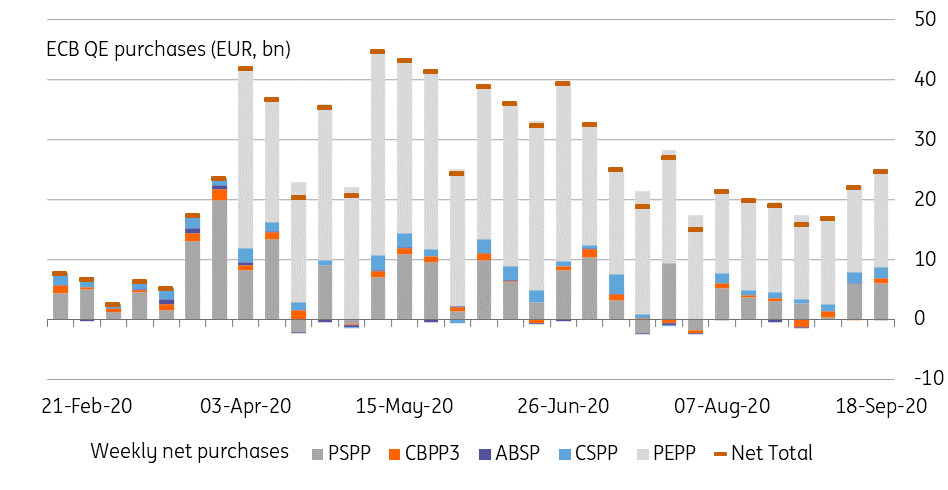

ECB QE volumes are slow to pick up

Weekly ECB purchases are increasing, albeit only slowly from their summer break. Purchases under the pandemic emergency programme rose to €16.1bn from €14.4bn the week before, reaching their highest volume since late July. Other asset purchases rose to €8.7bn of which public sector purchases accounted for €6.1bn. Looking at the currently benign environment for bond spreads one can see why the ECB might not feel the urge to ramp up purchases faster.

Today's events: Fed's Powell, ECB speakers, 30Y DSL sale

The main event is the joint appearance of Fed Chair Powell and Treasury Secretary Mnuchin before the House Financial Services Panel. Powell's prepared remarks released ahead of time suggest no change of tone since last week's FOMC, and do not validate expectations of more easing. Expectations should rise nontheless if sentiment continues to deteriorate.

European central bank speakers are bound to grab some headlines with Villeroy, Panetta and Lane all speaking.

European bond markets will also turn their attention to the sale of the new 30Y DSL 0% 1/52 via Dutch direct auction. Yesterday the Dutch State Treasury Agency released the spread guidance of 7 to 11 basis points over the reference bond, the German Bund 8/50. The agency plans to sell €4-6bn. Whilst the sale is a significant amount of duration for the market to take down, we think it comes at an opportunte time: we expect demand for duration globally to rise over the coming month.

Germany also taps its 2Y Schatz.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more