Rates Spark: Hawkish Fed continues to simmer

Federal Reserve minutes were as expected, but the market is far more inclined now to latch on to hawkish talk given the price action of the last few weeks. It still leaves us with a Fed that's not done with hiking

FOMC minutes had a hawkish tint, but so too did Chair Powell on 1 February if listened to carefully

Although market rates are a tad higher following the Fed minutes from the 1 February Federal Open Market Committee meeting, there was nothing material in them, at least nothing terribly unexpected. Bloomberg headlines noted that some (non-voting) members would have favoured a 50bp hike, but this was not new news. Bullard made that clear on a prior CNBC interview in fact. The 25bp hike delivered was unanimous, which was also not new news.

The only item of note really was that the minutes were expected to be a tad more dovish. Reading through them, they had a clear hawkish tint. This is in stark contrast to the impact market reaction to the FOMC outcome itself, which had headlined with a nod toward a dis-inflationary tendency. Indeed this was mentioned in the minutes, but beyond that the dominant theme was a Fed continuing to fret about inflation, and noting that the labour market remains very tight.

The dominant theme was a Fed continuing to fret about inflation, and noting that the labour market remains very tight

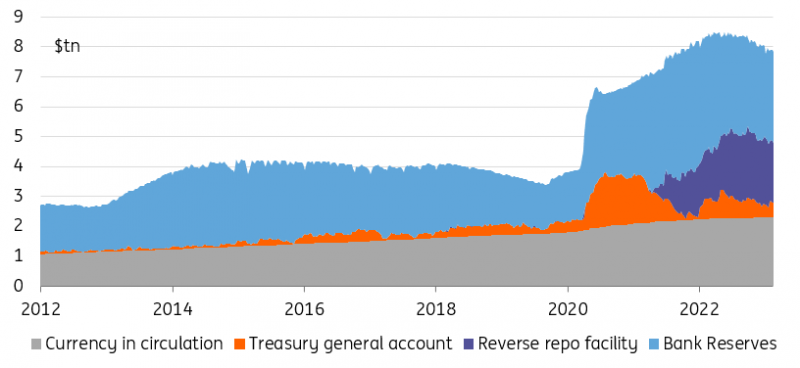

In terms of liquidity conditions, the Fed noted some easing in the use of the reverse repo facility, and an expectation that that continues through 2023. The Fed noted a likely fall in reserves as we head into the April tax season. They also noted a likely tendency for money market conditions to tighten ahead, which should correlate with falls in the cash going into reverse repo and a rise in relative repo rates. In fact that is a theme to be expected right through 2023.

Overall, the market reaction is for higher rates. A lot of this is down to the eyes of the beholder. At the FOMC itself, the market was looking for anything dovish to latch on to. From the minutes, that’s flipped, with the market now fretting over any hawkish hints. They were always there. But given the moves higher in market rates in the past weeks, there is an increased sensitivity to hawkish talk…

More bank reserve reduction should compound Fed policy tightening in the coming months

EUR rates looking for a fresh push at already lofty highs

Bund yields appear to struggle moving higher from here, but as we noted before the levels above 2.50% already appear lofty. Rates retreated from their intra-day highs after some comparatively dovish remarks from Frances Villeroy. He noted that markets had “overreacted a little” with regards to the terminal rate and that the ECB was “in no way” obliged to hike at every meeting between March and September.

Markets are already fully pricing in 125bp in ECB hikes, taking the terminal rate to 3.75%

In turn though, it still implies that all of those meetings are fair game for hike speculation. And it does not mean that there could not be another push higher. Markets will remain perceptive to any hints that inflation proves more sticky. Cue, today's final eurozone inflation. Even if it should be well flagged, any upward revision to today’s final eurozone inflation for January would neatly fit into the narrative.

But markets are already fully pricing in another 125bp in ECB hikes to take the terminal (deposit-)rate to 3.75%. The source of that next push higher in market rates would increasingly have to come from somewhere other than the front end – perhaps more related to a longer-term outlook, technical factors, or from outside the eurozone.

Long-end sovereign issuance continues undeterred

Supply can be counted on at least for a temporary bearish push in rates is illustrated by yesterday’s more than 4bp steepening in the 10-30y Bund curve. Yesterday Germany mandated a 30Y bond tap, the announcement of which accelerated a resteepening dynamics in Bunds, but not so much in swaps – the 10s30s swap curve which steepend only half as much.

European sovereigns and supranational's strong ultra-long presence despite headwinds is an encouraging sign

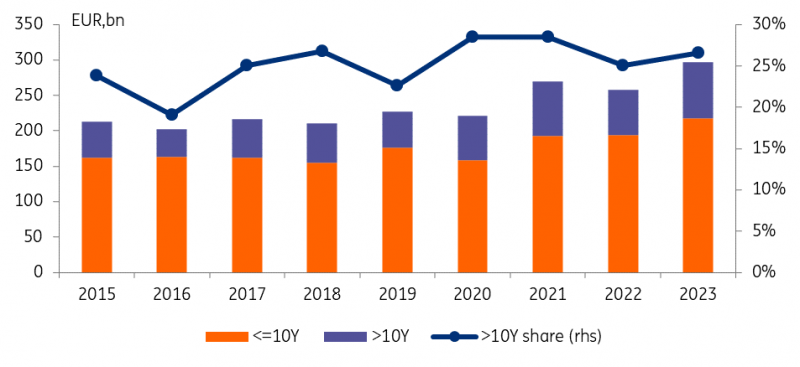

Fair, in current extraordinary times duration will demand more of a concession given still high volatility, the curve inversion and already sufficiently enticing yields at the front end. But when issuers tap into ultra-long funding they usually serve an existing and ongoing demand in the market. As such, European sovereigns' relatively strong ultra-long presence despite the aforementioned headwinds should be seen as an encouraging sign. Issuance data for the first two months in each of the past years shows that this year’s more than 27% share of ultra-long issuance (defined here as 15y maturity bucket and longer) is already above average, and that despite this year's record issuance in the first months.

European government bond and E-name issuance in the first two months of each year

Today's events and market view

In the eurozone many will look to the final inflation data for January. After German inflation data was not available for the calculation of the initial flash estimate, an upward revision now should be well flagged. Nonetheless, it will generate headlines that fit the current hawkish narrative.

In the US the attention falls on the usual initial jobless claims data as a more real-time take on the temperature in the job market. We will also get the second print of fourth quarter 2022 GDP.

In supply Germany has mandated a 30y bond tap which shoudl be today's business, The US Treasury will auction 7Y notes.

With regards to the next potential drivers of direction rates markets will closely follow the first testimony of the BOJ new incoming governor Ueda and what he has to say on its policy of yield curve control tonight.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

Rates DailyDownload

Download article