Rates Spark: A quieter US can help to calm things for a bit

US Treasuries remain heavy, but it's not all about the US this time. The Euro curve remains under steepening pressure. Without a catalyst to reassess the ECB path, the front-end will remain anchored, while the back-end plays out inflation concerns and supply pressures. Gilt yields also continue to rise sharply. But a quieter US on Thursday might just calm things for a bit

US Treasuries remain under pressure, but at least the 30yr saw some buying

Market rates have shot higher as a theme for early 2025, and while the move has been bolstered by higher Treasury yields, there’s been independent rises in the likes of Euro market rates and gilt yields. Issues spanning sticky inflation and high deficits abound, as do Trump administration tax cutting and tariff raising policies. Actual effects remain opaque, but the path remains higher until or unless the underlying narratives change.

Wednesday's US 30yr auction was a much tidier affair compared with the 3yr and 10yr earlier this week. The 30yr came c.1bp through "secondary" – the inverse of tails seen on the 3yr and 10yr auctions. We had a suspicion this might happen. We saw a frantic move higher in yields for no good new reason. In contrast to Tuesday when at least we had some data that was supportive of higher yields on the day. In any case it's a small relief for bonds for a change – at least there are some buyers out there that have spotted some semblance of value. There is no doubt that yield have seen a material back up in the past number of weeks, and at some point will attract interest.

Thursday sees US equity markets close in honour of Jimmy Carter's funeral, but banks will be open as it's not an official federal holiday, so most other financial market activities will be operational. However, there will likely be a material dampening effect on overall market liquidity, and at the margin, will likely see some buying of bonds as a place to park cash on days like these.

More records broken by gilt yields, but jumping in is risky business

UK gilt yields broke even higher, with now also the 10Y point at 4.8% reaching new highs. The key drivers are sticky inflation, government spending, US rates and supply pressures. These factors together justify the higher yields we currently see, although we don’t think we are dealing with a new equilibrium. Current market pricing suggests a terminal Bank of England policy rate of 4.25%, which seems too high in our eyes. But turning the bearish sentiment around may not happen in the near term since the catalysts for a push lower in rates, such as better inflation numbers, is still missing.

One could argue that the current yields pose attractive value for investors, but we are also aware that catching a falling knife is risky business. We, and many others, have held the belief that gilt yields have been trading too high for a long time, and yet the drift has been consistently upwards. What we’re seeing is therefore also an unwind of positioning. The additional volatility adds to the mix, because this limits investors with risk budgets from jumping in now. And given we still see potential for US rates to go higher, gilt yields will also remain under upward pressures for the time being.

EUR rates are still under the spell of supply and a refocus on inflation concerns

Longer EUR rates remain under upwards pressure while the front end remains largely anchored for now. For the latter to move more meaningfully it will probably need a catalyst for markets to reassess the European Central Bank trajectory, while further out markets are more freely pushing rates higher alongside US rates amid seasonally amplified supply pressures and a refocus on inflation concerns.

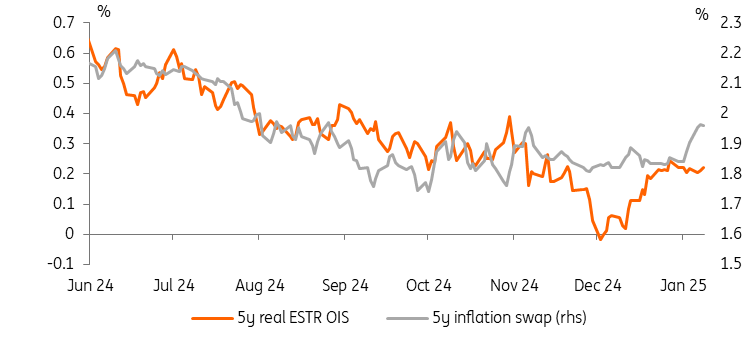

EUR real OIS rates and inflation swaps illustrate nicely how the market shifted from growth concerns in late November back to inflation concerns at the start of the year – the dip in real rates is now followed by a rise in inflation swaps, here depicted in the 5y tenors. If we were to look at this for the US the picture is less clear for the past few days, but one would see a clear rise in real rates picking up again after the December jobs report.

EUR rates markets go from growth concerns back to inflation worries

Thursday’s events and market view

From Germany we will receive industrial production numbers for November, which are expected to have risen by 0.5% year-on-year. For the eurozone as a whole we have retail numbers. The US will have Challenger jobs data and various Fed speakers.

Issuance includes a syndication by Portugal for 10Y PGBs totalling an estimated €3-4bn. Spain will auction 3Y, 7Y and 22Y SPGB, together with a 15Y SPGBei, together totalling €7bn. France has 10Y, 11Y, 18Y and 30Y OATs lined up for a total of €13bn.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

Rates DailyDownload

Download article