Rates Spark: A dovish week

The Fed and BoE overall messages didn't change, though offered enough dovish hints for market expectations to converge on June as the kick-off date for the easing cycles. June is still some months away, and potentially hot US PCE data next week could show that there is still a way up for rates near term. Expectations for the ECB should have the best foundations

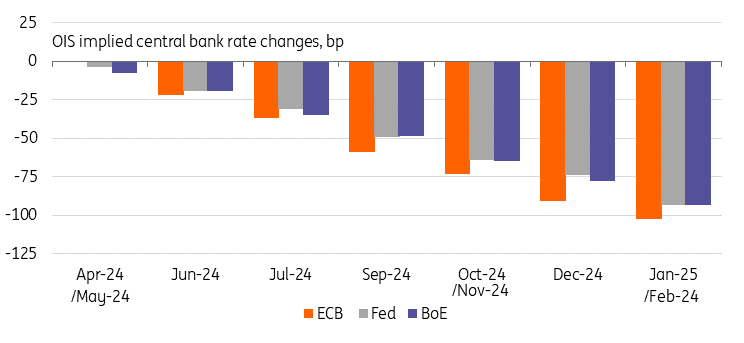

Markets are settling on June as the month for central bank cuts

This week was one for the doves, with market pricing converging to the idea that June will likely be the month that the ECB, Fed and BoE all make their first rate cut. With regards to the BoE markets took their cue from the two hawkish members of the monetary policy committee having finally dropped their vote for a rate hike, opting instead to join the consensus vote for no change. The Swiss National Bank was supposed to be among those central banks but surprised us on Thursday with an early cut, which did however add to the overall dovish backdrop.

June is still a couple of months away, however, and with US PCE data expected to come in hot next week, cuts are not set in stone everywhere. US yields have been surprised before by inflation numbers and can set the tone for the weeks thereafter. Combine that with a backdrop of high supply and US yields could test higher grounds. For the BoE our economist also still thinks there is a better chance that the first hike could be postponed to August, being wary not to overinterpret the change in the voting split.

The ECB seems to be in the most comfortable position – inflation is gradually falling and growth remains in stagnation territory. The disappointing manufacturing PMIs from Germany and the eurozone on Thursday were a reminder of the economy’s weakness. All the ECB wants to assure is that first quarter wage increases are contained, which will be known by the June meeting date and should not be a hurdle. Markets are pricing in an 87% probability for a cut in June and around 90bp of cuts for the year.

Now that June ECB cuts are anchored, markets will want to hear how many more cuts the ECB has in mind for the rest of this year and next year. On Friday morning the ECB’s Nagel may share his view on the way forward and later in the day we have Holzmann and Lane speaking, which can all influence market views. Having said that, implied volatility from swaptions came down significantly since the beginning of the month, suggesting that markets have started narrowing down on their idea where rates should be going, limiting potential moves on the short end of the curve.

Markets are eyeing a synchronised start to Fed, BoE and ECB rate cut cycles

Today's events and market views

German Ifo survey data will likely reflect the economy's underlying weakness and thus a sharp upside surprise seems unlikely. The other highlights are the various speakers from the ECB and Fed, including Nagel from the Bundesbank and Powell at the US opening.

For supply we have Italy auctioning 2y BTPs for around €2.5-2.75bn with the inflation linked auction having been cancelled after the recent syndicated sale of a new 10Y BTPei.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more