Rate rise pressure underestimated in Japan

We think Japan will hike by more than the market expects. The argumentation starts with wage inflation at 5%, and there's more (we explain). Given that, 2% is a generic target to consider. Not in the immediate few years, as 1.25% is the nearer-term target for the BoJ. But eventually. If so, spreads (vs US) should tighten, and fixed rate lock-ins look great

We see the BoJ landing at 1.25%, but the longer-term neutral rate is closer to 2%

The Bank of Japan estimates its neutral rate at between 1.0% and 2.5%. We think that a neutral rate at around 2% can be justified. It's a non-consensus view, but we view the probability of achieving the 2% inflation target on a sustainable basis as far higher than the market expects. The market tends to be overly pessimistic on the Japanese economy, and in consequence heavily biased towards a dovish leaning on rates. We have a different view.

Just because they've been in deflation for decades doesn't mean they can't return to normal in the future. Note wage growth in particular, running at +5% for two years now. And also the recent increases in asset prices such as land, real estate, and equities. Corporate price setting behaviour is slowly reacting, and Japan seems to be finally moving slowly towards a more normal state.

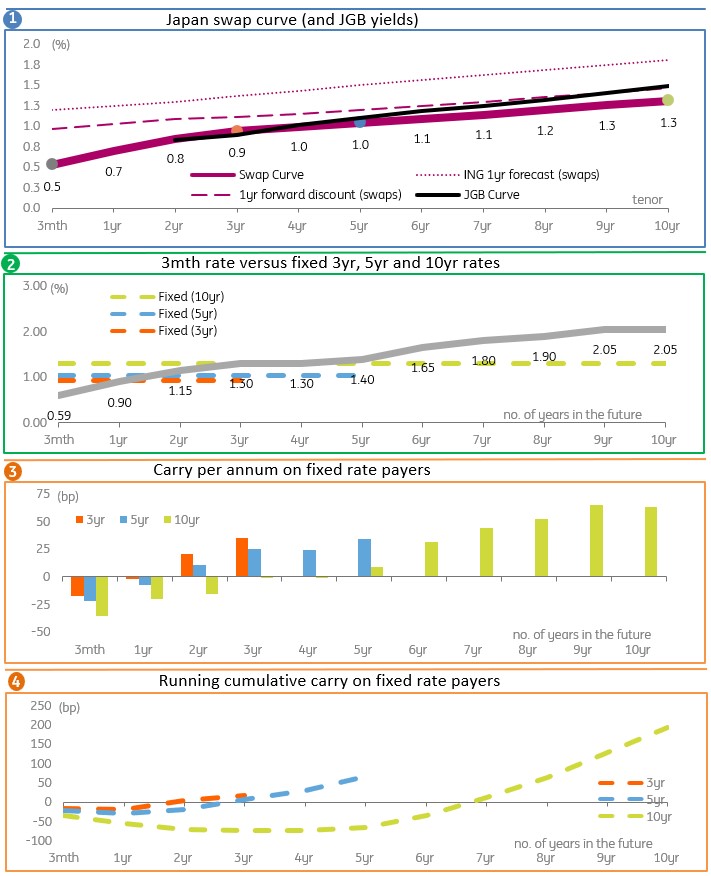

Lock-ins set today are negative in carry, but swing to cumulative positive carry

Currently, the 10yr Japanese Government Bond (JGB) yield is at 1.5% and 10yr Tokyo Overnight Average Rate (TONA) at 1.3%. These are well above the 3mth rate as the curve stretches from 0.6% on the front end. This upward sloping curve generates higher rates in the forward space, and if we go out as far as 5yrs forward, the 10yr rate begins to knock on the door of 2%. We agree with this broad directional view, i.e., that market rates are under structural upward pressure. But we anticipate that upside to market rates is in excess of the forwards, both on a shorter- and longer-term perspective.

The consequence of this is lock-ins set today have negative impact carry (as the curve is upward sloping). But over time, that negative carry morphs to positive carry (as the BoJ hikes), swinging lock-ins in the 3yr, 5yr and 10yr tenors into cumulative positive carry outcomes. In particular for the 10yr, which starts out with the highest negative carry. That said, we believe the 5yr is a suitable middle ground option.

The rates environment in Japan, including projections

And carry calculations from lock-ins at current rates

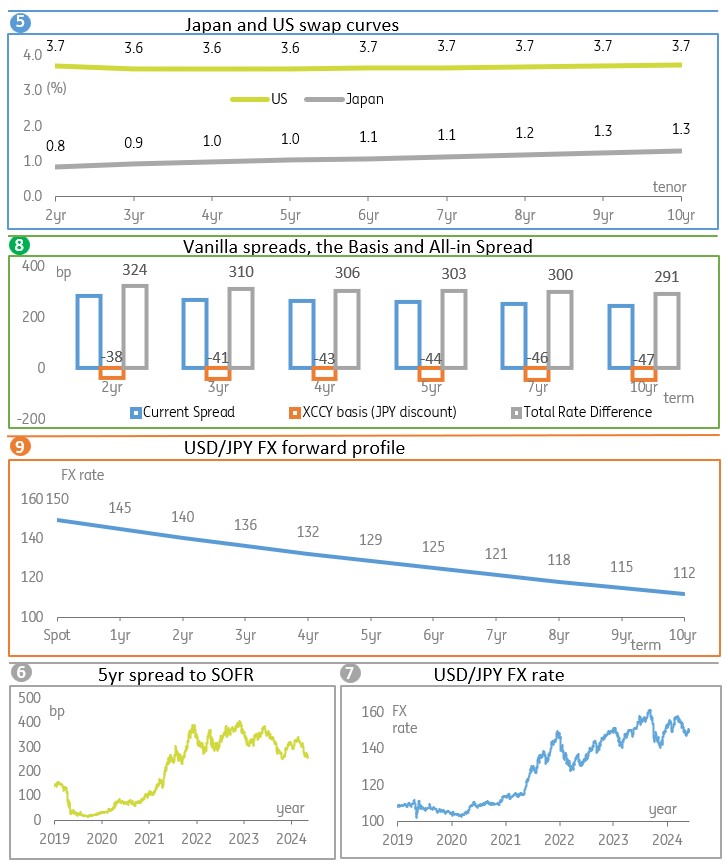

Spreads are tighter now, but projected to get tighter still

Spreads to Secured Overnight Financing Rate (SOFR) are off previous highs, but still elevated. The 5yr spread, for example, had hit 400bp in 2023, and is now at around 300bp (3%). The negative basis attached to the JPY leg remains on a tightening trend, but continues to meaningfully act to amplify the all-in spread. As a theme we think this basis should remain on a gradual tightening trend, and we also expect underlying TONA to SOFR spreads to continue to tighten too. This all argues for the classic positive carry play, where we go long SOFR and short TONA to pick up the spread.

For asset managers’ this acts as a yield pickup, while for liability managers it acts to reduce interest rate costs. The risk in either case is on the currency. As this positive carry swap generates a JPY liability, the biggest fear is too much JPY appreciation. The FX forward profile maps out something of a breakeven curve. It discounts significant JPY appreciation, reflecting the spreads profile. The trick here is to avoid the appreciation as discounted in the forwards, as hitting the forward curve wipes out the benefit of the positive carry in the swap.

Our FX strategists have USD/JPY at 150 at end-2026. This is a huge comfort for those setting the positive carry play, at least for the coming couple of years. Beyond that, it's unlikely that USD/JPY gets to 129, which is the 5yr forward breakeven, and even less likely that it gets to 112, which is the 10yr forward breakeven. In consequence, we're quite comfortable with the FX exposure. And to boot, the play would achieve an offsetting positive mark-to-market on a theory that we have absolute tightening in spreads going forward.

Japan spreads to SOFR, and spreads environment

Cross currency circumstances calculated

The macro back story is one of recovery, with notable upside risks to inflation

Japanese CPI inflation unexpectedly accelerated in March. See more here. More importantly, the acceleration in inflation was broad-based. Earlier price hikes in fresh food are feeding through to processed foods, and, with a time lag, to service prices such as eating out prices. We expect this trend to continue. Next up is the BoJ's meeting on 1 May. We'll get the April CPI reading ahead of that, which will be a good gauge of how firms' pricing behaviour changes in the face of strong wage growth and rising input cost pressures, as they usually tend to adjust their prices in April (the first month of the fiscal year). We think there will be enough to justify a May hike, but the most recent monetary board minutes argue for gradualism.

Meanwhile, growth is expected to remain on a recovery path. The recovery should be driven by services and private consumption. The latest data from industrial production, retail sales, and the labour market, point to a gradual recovery. See more here. Further wage growth above 5% and a solid performance in the asset markets should lead to a recovery in consumption. In addition, Chinese tourists, who haven't yet returned to pre-Covid levels, are finally starting to return to Japan, which will also help retail sales and services. Manufacturing and exports are likely to remain subdued though.

Regarding the US trade policy, if trade tensions don’t escalate more than the market currently expects, they won’t affect the BoJ’s rate hike plans. Also, the government is trying to negotiate with the US government to opt out of the 25% reciprocal tariff list. In the end, we believe that eventually the tariffs will be much more relaxed, but negotiations will take a long time.

As for the Japanese Government Bond (JGB) market, while the BoJ may be concerned about the recent rise in 10Y JGB rates, market intervention is unlikely. The BoJ has already mentioned that the current trend reflects the market's view and that it is not the time for the BoJ to intervene. They left the door open for adjusting the bond-buying operation if they find excessive volatility. But given the fact that the BoJ ended its Yield Curve Control (YCC) programme a year ago, a drastic change in the operation could mislead the market about the revival of YCC; thus, the BoJ will be quite cautious on that.

As we expect the BoJ to hike two times in 2025 (May and October) and once more in 2026, with the terminal rate at 1.25%, the JGB 10Y yield is also likely to rise to +2% by the end of 2026. That forms the underpinning of the carry analysis outlined above in the swap market space, and argues that even though market rates have already risen, lock-ins here look good against an even higher rates prognosis ahead. Spreads versus the US are also projected to tighten.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article