Positive outlook for Hungarian labour market but caution advised

Recent data continues to paint a positive picture of the labour market outlook. However, expected real wage growth in 2025 is now lower while the unemployment rate remains stable as people are going back to work, both due to higher inflation

Recent data releases on the Hungarian labour market paint a mixed but in general still positive picture. The trend in employment and unemployment shows a tight labour market which is also expected to stay with us for the whole year as new productive capacity is expected to go live. On the other hand, average wage growth continues to slow in almost all sectors, but not at the same pace. Expected real wage growth in 2025 is now lower due to the lower wage growth outlook and higher expected inflation.

| 4.3% |

Unemployment rate (Nov-Jan)ING Forecast 4.6% / Previous 4.4% |

| Lower than expected | |

Positive surprise despite seasonal labour market trends

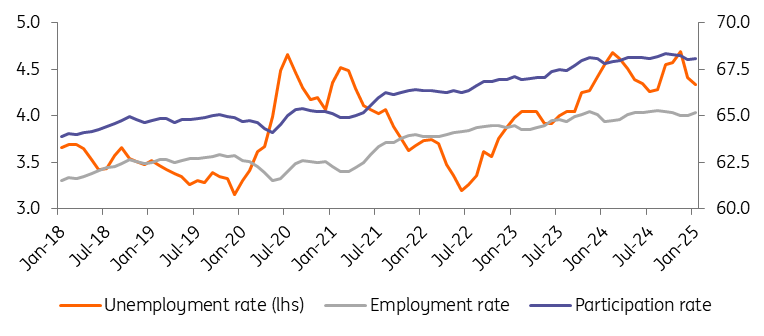

The latest labour market statistics from the Hungarian Central Statistical Office (HCSO) came as a positive surprise at the beginning of the year, with the model estimate for January 2025 showing an unemployment rate of only 4.4%. Meanwhile, the official three-month moving average of the survey rate moved in a positive direction, with the indicator standing at 4.3% for the November-January period. The seasonal rise in the unemployment rate at the beginning of the year, which has been observed in recent years, was therefore largely absent in the first month of this year. In terms of the number of unemployed, the two statistics put the size of the group at around 213,000 to 214,000.

The detailed data shows that, unlike in recent years, the number of people in employment has not fallen, but has actually slightly risen on a monthly basis. Moreover, the number of unemployed rose slightly, within the margin of error, from December to January, so the number of participants in the labour market also increased. All this suggests that many people may have returned to the labour market in anticipation of the new wave of inflation, fearing that it will worsen.

Historical trends in the Hungarian labour market (%, 3-m moving average)

Of course, no serious structural conclusions should be drawn from one month's estimated data. But if we look back to the depths of the cost-of-living crisis, which may still be fresh in households' memories, similar processes took place. As inflation picked up, the number of people participating in the labour market increased. Many people started actively looking for a job (the definition of unemployed), but back then it was easier to get a job straight away after inactivity. Today the task is much more difficult as most companies have had two difficult years. Rationalisation and cost-cutting have started in many places, especially in manufacturing.

We are only at the beginning of this potential wave of downsizing, which is why the indicator of the potential labour reserve (which includes not only the unemployed but also the underemployed and the inactive who do not meet the official definition of being unemployed but are self-classified as such) remains at its lowest level for a year and a half. This is keeping the labour market tight. This tightness could be maintained by the new productive capacity expected to come on stream during the year, which could represent a substantial absorption of labour.

In the year ahead, however, the positive effects mentioned above may be tempered by a trend decline in consumer and business confidence, suggesting that the economy may again be weaker than expected. This could lead to further retrenchment by companies that are still holding onto their workforces. In this respect, the export-orientated manufacturing sector may be particularly affected. All in all, the unemployment rate could deteriorate somewhat at the beginning of the year, while an improvement is expected towards the end of the year. In numerical terms, this could mean an average unemployment rate of around 4.5% for 2025 as a whole.

| 11% |

Average wage growth (December)ING Forecast 11.1% / Previous 11.9% |

| Lower than expected | |

Hungarian wage growth is continuing to slow

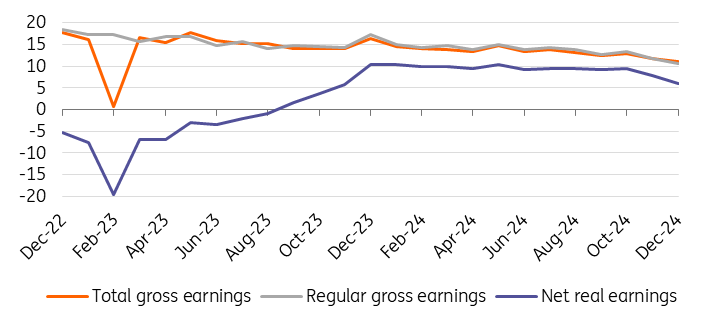

According to the latest data from the Hungarian Central Statistical Office (HCSO), wage growth in the Hungarian economy continued to slow in December. Compared to the market consensus, which already expected wage growth to slow to single digits in December, the growth was stronger. Average wages rose by 11% in the final month of last year, almost in line with our expectations.

Today's data point is in line with the longer-term trend of a slow but steady moderation in the pace of wage growth since the beginning of the year. December's year-on-year wage dynamics were the lowest in 2024. But with the growth rate still in double digits for the year as a whole, the picture for wage outflows is clearly positive. Unfortunately, this was not enough to pull the Hungarian economy out of stagnation. Despite an average wage increase of 13.2% for the year as a whole and unusually high real wage growth of more than 9% on the back of falling inflation, a lack of consumer confidence pushed households towards savings rather than sparking a consumption boom.

Wage dynamics (3-month moving average, % YoY)

Looking at the December data in more detail, the slowdown in average wage growth is not sector-specific. However, the slowdown was more pronounced than usual in a number of sectors, such as agriculture, mining and construction. In manufacturing, on the other hand, the pace of wage growth slowed only slightly, while there were also some large negative surprises in the services sector.

Looking at developments in the number of persons employed, there is a subtle downward trend almost everywhere, so the slowdown in wage dynamics is unlikely to have been driven by the composition effect. It is more likely that the higher base effect of the unconventional minimum wage increase in December 2023 is reflected, and that sectors where the impact of the minimum wage increase was greater showed a greater slowdown in wage growth. In addition, lower company bonuses may have played a role in the lower average wage growth. In contrast, the public sector saw a dramatic jump in wage growth (over 17%), clearly linked to education (28.5%), where teachers in all school district centres received an end-of-year bonus last December, the first time this has happened since 2012.

Nominal and real wage growth (% YoY)

Turning to this year, the key question is whether we will see a repeat of what we saw in 2024. In other words, despite companies' desire for lower pay rises, the final agreement was closer to what workers wanted. According to the Randstad survey, 88% of companies are considering a maximum wage increase of 10%. In contrast, 86% of workers said they wanted wage increases above 11% (45% above 20%). So the gap is again huge.

However, given the fluctuating unemployment rate, the generally weak economic environment of the past year and the generally declining profitability of companies, we expect employers to be in the driving seat this year, resulting in lower wage growth. This could be offset by ongoing wage adjustments in the public sector and the composition effect. With regard to the latter, it is likely that companies will first lay off low-paid, low-productivity workers as part of a rationalisation drive, which could proportionally reduce the number of low-paid workers in the economy and thus push up the average wage in the economy.

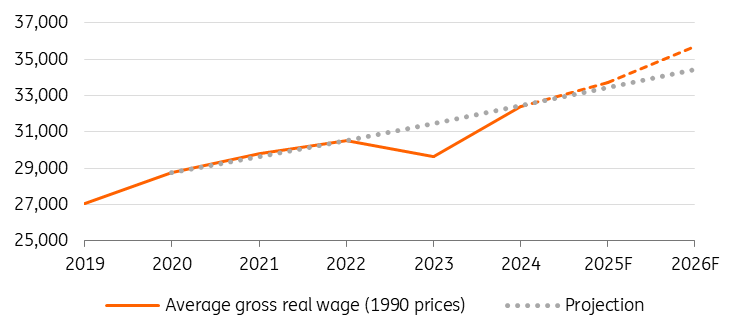

The level of average gross real wage (1990 CPI adjusted HUF)

All in all, we are forecasting average wage growth of 9-10% this year. However, we also expect average inflation to be at least 5.1%, so real wage growth for the year as a whole could be around 4%. While this is still slightly above the historical average, it is nowhere near as strong as last year.

The more important question, therefore, is whether the accumulated savings will be reflected in the real economy in the form of consumption and whether the government measures will find their way into the real economy or whether, in the end, they will only increase the propensity to save as a result of rising inflation.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article