Portugal: Political stability to support economic growth in 2022

- 10 February 2022

- Eurozone Quarterly Portugal

We expect the Portuguese economy to continue to grow at a firm rate in 2022. A strong labour market, lower political uncertainty, and a fiscal boost from Europe will support the economy

We see economic growth rebounding in 2022

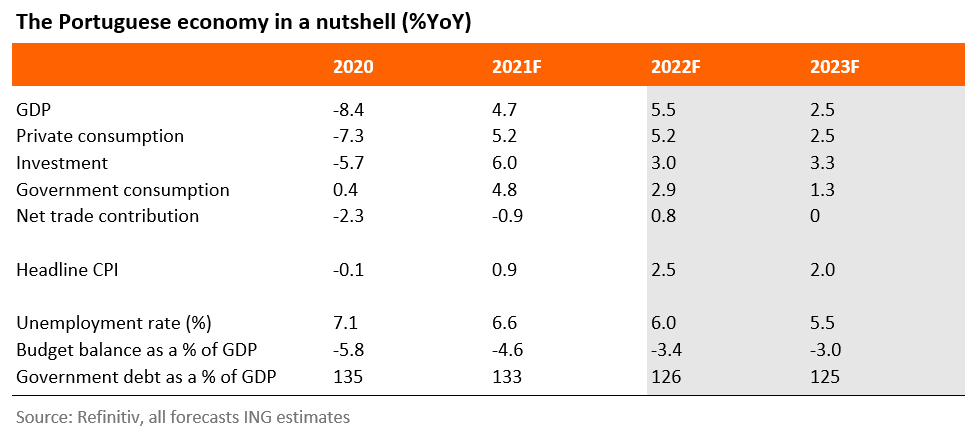

The latest gross domestic product report showed that the Portuguese economy grew by 4.9% in 2021, the highest growth figure since 1990. The economy was able to grow relatively well in the final quarter of the year (1.6% quarter-on-quarter), which implies that the economy is now only 1.5% smaller compared to pre-pandemic levels.

For the first quarter of 2022, we expect a slowdown due to the Omicron wave, but thereafter we expect growth to pick up. Activity should reach its pre-pandemic level in the second half of 2022. For 2022 as a whole, we expect 5.5% economic growth.

The strong labour market should support activity. The unemployment rate was equal to 5.9% last December, which is lower than before the pandemic. As we expect demand to remain elevated from the second quarter onwards, and the number of businesses that report labour shortages is currently limited, we expect the unemployment rate to fall further.

Political uncertainty is now lower

Political uncertainty dropped significantly at the beginning of the year. The previous government fell in October 2021 because radical left-wing parties did not support the proposed 2022 budget. Radical left-wing parties wanted to alter the labour law and increase social spending. During the snap elections held in January, however, the Socialist Party unexpectedly won a majority in parliament. This will smooth the approval of the original budget.

It is likely that the Socialist government remains fiscally prudent, even though an important part of the budget will likely invest in the national health service and increase the minimum wage. Increasing the minimum wage in times of higher inflation could pose problems for companies.

The reduced political uncertainty, together with the stronger labour market, might also make consumers more confident which in turn could lower precautionary savings. Currently, the savings ratio is 11%, which is about four percentage points higher than before the pandemic.

A more stable majority will also help secure funds from the Next Generation EU fund. Portugal should receive €16.6bn (about 8% of 2021 GDP) over the next three years. This should boost the current low levels of public investment in Portugal.

All in all, the outlook is positive for the Portuguese economy. A strong labour market coupled with lower political uncertainty and a fiscal boost from Europe will support activity. For 2022 and 2023, respectively, we expect 5.5% and 2.5% economic growth.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Eurozone Quarterly: Leaving the pandemic behind

- This bundle contains 11 Articles