OPEC+ policy shift clashes with demand uncertainty

Another large supply hike from OPEC+ confirms the group's policy change. However, the issue is that this policy shift is occurring at a time when there is already plenty of demand uncertainty. Stronger supply means the oil market will face a larger-than-expected surplus this year

OPEC+ policy shift

Demand concerns induced by tariff uncertainty have only been compounded by a shift in OPEC+ policy, which has weighed heavily on oil prices. OPEC+ appears to be in the process of moving away from defending prices towards defending market share. The group has announced two larger-than-scheduled supply increases for May and June. OPEC+ is set to increase supply by 411k b/d in both May and June. Under the original plan, the group was set to bring back 2.2m b/d of supply over 18 months. However, in a three-month window, it is set to bring almost 1m b/d of supply back onto the market. And if the group sticks with increases similar to those seen for May and June, the full 2.2m b/d of supply will have been brought back by the end of the third quarter of this year – a full 12 months ahead of schedule.

A key reason for this shift in policy appears to be growing discord within OPEC+. Saudi Arabia is not happy that some members are producing above their agreed production levels, specifically Kazakhstan and Iraq. Therefore, the boost in output is to punish those producers who have consistently pumped above their target levels.

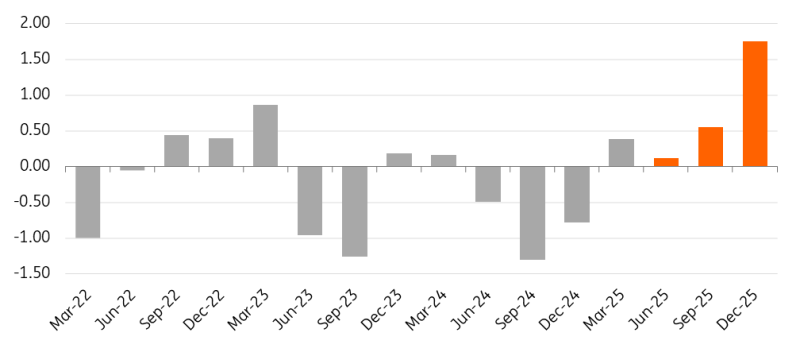

The move to bring back supply quicker than expected leaves the market in a larger surplus through 2025, thereby lowering the market's floor. We have revised our 2025 Brent forecast from US$70/bbl to US$65/bbl. While the scale of the surplus later in the year should mean further pressure on prices in the fourth quarter, where we now forecast Brent to average US$59/bbl. Expectations for a larger surplus are also reflected in the Brent forward curve, with more of 2025 trading in contango.

The uncertainty for the market is how long OPEC+ is willing to run with this new policy before reversing back to trying to support the market. Saudi Arabia needs around US$90/bbl to balance its fiscal budget, and so the country will be facing a widening budget deficit given the price weakness.

US oil producers will also be feeling the pain. The US industry needs an average of US$65/bbl to profitably drill a new well, according to the Dallas Federal Reserve's quarterly energy survey. And with WTI trading sub-US$60/bbl, we are likely to see a pullback in drilling activity in the US, which also calls into question any forecast for US crude oil supply growth this year and next.

Global oil balance moves deeper into surplus (m b/d)

European gas supply fears ease… for now

European gas prices remain under pressure, with TTF down more than 20% since "Liberation Day". Tariff uncertainty will raise demand concerns. However, there are also other factors weighing on prices.

Europe has been seeing stronger flows of LNG in recent months. In fact, EU LNG send-outs in April were the highest on record. Weaker Chinese LNG demand has allowed for stronger flows to Europe. Chinese LNG imports over the first three months of the year were down more than 21% YoY. Lower prices might stimulate some Chinese spot demand in the short term, however, tariff escalation does pose some broader demand risks in the months ahead.

In addition, the EU is moving towards possibly lowering storage targets ahead of the 2025/26 winter, as well as providing more flexibility on these targets. This would naturally reduce the buying needed over the injection season to hit storage targets. This has also helped the TTF forward curve return to a more normal shape, where summer 2025 prices are now trading at a discount to winter 2025/26 prices, providing more of an incentive to store gas ahead of next winter.

EU gas storage stands at more than 41% full now, up from a low of 34% at the end of March. However, it is still some distance below the five-year average of 51%, and therefore, ahead of next winter, we will still need to see the largest net injections since 2022 to reach the current 90% storage target.

Demand risks, stronger LNG flows, a better storage situation and more flexibility in storage mean that we have cut our TTF forecast. We have lowered our 2025 forecast from EUR45/MWh to EUR39/MWh. However, we are reluctant to cut significantly more for now, given that the market is still relatively tight and remains vulnerable.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

WTI TTF Trade War Tariffs OPEC+ Natural gas Monthly Economic Update LNG Energy Commodities BrentDownload

Download article

8 May 2025

ING Monthly: The world is caught like a deer in the headlights This bundle contains 14 Articles