OPEC+ goes with another big supply hike

OPEC+ is implementing another aggressive supply hike. Effective in June, this increase solidifies a shift in policy. With prospects of further large supply increases in the months ahead, we revised our oil forecasts lower

OPEC+ supply increase

Nearly five years ago, the Saudi Energy Minister said speculators need to “watch out” and threatened to leave them “ouching like hell”. Well, the target appears to have shifted from speculators to the OPEC+ alliance. The Saudis are the driving force behind larger-than-scheduled supply increases to punish members who’ve repeatedly produced above their targets.

OPEC+ surprised the market back in April with a supply increase of 411k b/d for May, above the scheduled increase of 135k b/d. This past weekend, the group decided to go with a similarly aggressive supply increase for June.

Originally, OPEC+ was meant to bring back 2.2m b/d of supply over an 18-month period, running through to September 2026. However, in three months, the group has decided to bring back almost 1m b/d of supply. There are reports that the Saudis threatened similarly large supply increases in the months ahead if members don't stick to their targets. This could mean that the full 2.2m b/d of supply is brought back to the market by the start of the fourth quarter of this year -- 12 months ahead of schedule.

The oil market has been dealing with significant demand uncertainty amid tariff risks. This change in OPEC+ policy adds to uncertainty on the supply side. Adding to the uncertainty: the group will decide on output levels month by month. OPEC+ will decide July output levels on 1 June.

The key to knowing how far the Saudis will take what is starting to look like a price war is the nation’s tolerance for low oil prices over time. The Saudis need around US$90/bbl to balance their fiscal budget, quite a distance above current prices. Saudi Arabia will be able to lower its fiscal breakeven level by pumping more. Obviously, this also depends on how much lower prices trade amid increased supply. The widening gap between their fiscal breakeven level and current oil prices means that the Saudis will have to cut spending and/or tap debt markets.

What does this do to the oil balance and price forecasts?

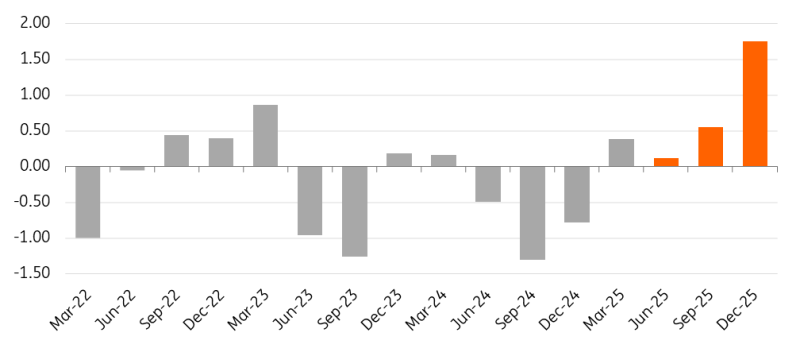

These more aggressive supply hikes from OPEC+ mean that the oil surplus will be brought forward, leaving the market in surplus throughout 2025. Previously, we assumed a balanced market in the second quarter and a small deficit in the third quarter, before moving into a large surplus by the final quarter of the year. This dynamic is reflected in the ICE Brent forward curve with more of 2025 now trading in contango. However, the key assumption is that OPEC+ continues to increase supply through the third quarter of the year by similar amounts as in May and June.

Oil prices have reacted negatively to the latest supply increase, with Brent trading below US$60/bbl. This is despite the market already expecting a large supply increase. The main uncertainty was around how large this increase would be. More aggressive supply hikes lower the floor for the market. As a result, we’ve revised lower our ICE Brent forecast for the remainder of the year from US$68/bbl to US$62/bbl (2Q25-4Q25). This leaves the 2025 average forecast at US$65/bbl, down from US$70/bbl previously. This will change if OPEC+ reverses policy once again or if lower oil prices embolden President Trump to take a more aggressive approach toward several sanctioned oil-producing countries.

Global oil balance moves deeper into surplus (m b/d)

US oil industry set to slow

The weakness in oil prices will prompt a pullback in drilling activity in the US. According to the Dallas Federal Reserve Energy Survey, oil producers need, on average, US$65/bbl to profitably drill a new well. With West Texas Intermediate (WTI) trading closer to the mid-US$50s, there’s little incentive to drill. Producer hedging may protect some oil producers initially. But US crude oil supply growth in 2025 and 2026 is looking less likely.

The US oil rig count stands at 479, down from a peak of 489 at the start of April. Well completions also appear to be trending lower, reflected in a lower frac spread count. In addition, if drilling activity does hold up, it isn’t guaranteed to translate to production. Producers may delay completing these wells in the current low-price environment. This would cause an increase in the inventory for drilled, but uncompleted wells (DUCs).

A slowdown in the US oil industry also has ramifications for US natural gas supply, given that a large amount of this supply is associated with production. This could be an issue, particularly given the stronger gas demand we’ll see with a ramp-up in US LNG export capacity.

Forward curves and spreads

Larger supply increases mean that more of the Brent forward curve should trade in contango, particularly towards the front end of the curve. The forward curve had been trading in backwardation through the end of this year. But now it only trades in backwardation until September. As more of the curve moves into contango, it’s reflecting an increasingly more comfortable market.

The more aggressive supply increases from OPEC+ should also be supportive for the Brent-Dubai spread. The spread was negative for much of the year, but recently returned to a premium as more Middle Eastern supply comes onto the market and weighs on Dubai.

Oil forecasts

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

WTI US oil production Trump Trade War Tariffs Saudi Arabia Price war OPEC+ OPEC Natural gas Dubai BrentDownload

Download article