Oil, Gas & CO2: Comfortable energy fundamentals vs growing supply risks

The 2025 oil balance looks comfortable which should see prices edge lower. However, sanctions are a clear risk to this view. We also expect weakness in European gas despite the stoppage of Russian pipeline flows through Ukraine. For European carbon, we believe the market is set for some moderate gains

Call 1: Oil market to be in surplus but growing supply risks

Oil prices have had a strong start to the year on the back of stricter US sanctions against the Russian energy sector and colder weather supporting demand in parts of the Northern Hemisphere. In addition, the decision from members of OPEC+ to extend additional voluntary cuts has reduced the scale of the surplus that was initially expected for 2025.

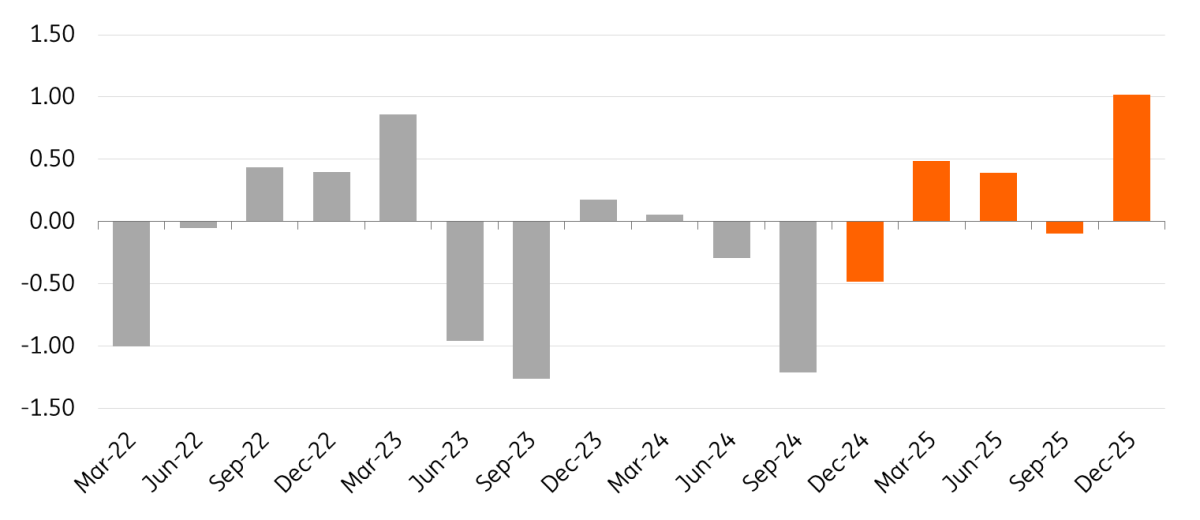

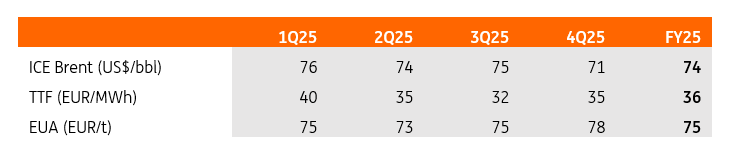

The oil market is still set for a 500k b/d surplus, which should keep a cap on prices. However, the uncertainty over Russian supply means that prices are likely to be better supported than initially expected. We expect ICE Brent to average US$74/bbl in 2025, down from an average of US$80/bbl in 2024.

In terms of supply for 2025, non-OPEC output is expected to grow by around 1.4m b/d. This supply growth continues to be a problem facing OPEC+, making it difficult for the group to increase their own supply without accepting lower prices. OPEC+ are currently set to start unwinding their additional voluntary cuts of 2.2m b/d from April. The group will also unwind these cuts at a slower pace than originally planned. Instead of bringing this supply back over the course of 12 months, they will now do so over an 18-month period.

OPEC+ supply is a risk to our view. Already the group has delayed its easing several times. Pushing back the return of this supply even further would tighten up our 2025 supply/demand balance. However, the potential impact of stricter sanctions against Russia and Iran does provide other OPEC+ members the opportunity to increase supply without weighing too much on prices.

OPEC's spare capacity provides comfort to the market in the event of any significant supply disruptions.

It is still too early to have a strong view of the potential Russian supply loss from US sanctions targeting Russia’s shadow tanker fleet. But clearly, the uncertainty will support oil prices in the short term. These sanctions may disrupt flows in the short term; however, Russia and buyers will likely find ways to circumvent them in the medium to long run. Failing to circumvent them and assuming strict enforcement means that the global supply surplus we expect could be fully erased.

Iran is the other upside risk. It is unclear how aggressive President Trump will be with Iran, but stricter enforcement of US sanctions against Iran could mean a large decline in export supply. Under Biden, Iranian supply grew by a little more than 1m b/d. But again losing Iranian supply would provide OPEC+ the opportunity to increase supply.

The cap for the market is the fact that OPEC+ is sitting on more than 5m b/d of spare production capacity. While the group may hold out for higher prices before tapping significantly into this, this spare capacity does provide comfort to the market if there were to be any significant supply disruptions.

Global oil demand disappointed last year with Chinese demand falling short of initial expectations. For 2025, demand growth is expected to be fairly similar to last year with global demand set to grow by around 1m b/d. Non-OECD, and specifically Asia, is set to dominate growth. Asia (including China) is set to make up around 60% of global oil demand growth. However, escalating trade tensions are not only a risk to oil demand but also broader sentiment across risk assets, something oil is unlikely to be able to escape.

Oil market set for a surplus, but sanctions are a clear risk (m b/d)

Call 2: European gas to trade lower

European natural gas prices have been well supported through the 2024/25 winter. Firstly, stronger gas demand from the power generation sector towards the end of last year meant that European gas storage started the heating season below initial expectations. In addition, the region has experienced a more normal winter relative to the two previous winters which has supported heating demand.

This stronger demand comes at a time when Russian pipeline flows via Ukraine have been halted following the expiry of Gazprom’s transit deal with Ukraine at the end of 2024. However, this stoppage was largely expected. The loss of this supply equates to around 15 bcm of natural gas per year. It also leaves the TurkStream pipeline as the only route for Russian pipeline gas into Europe, which in 2024 supplied a little under 15 bcm to the EU.

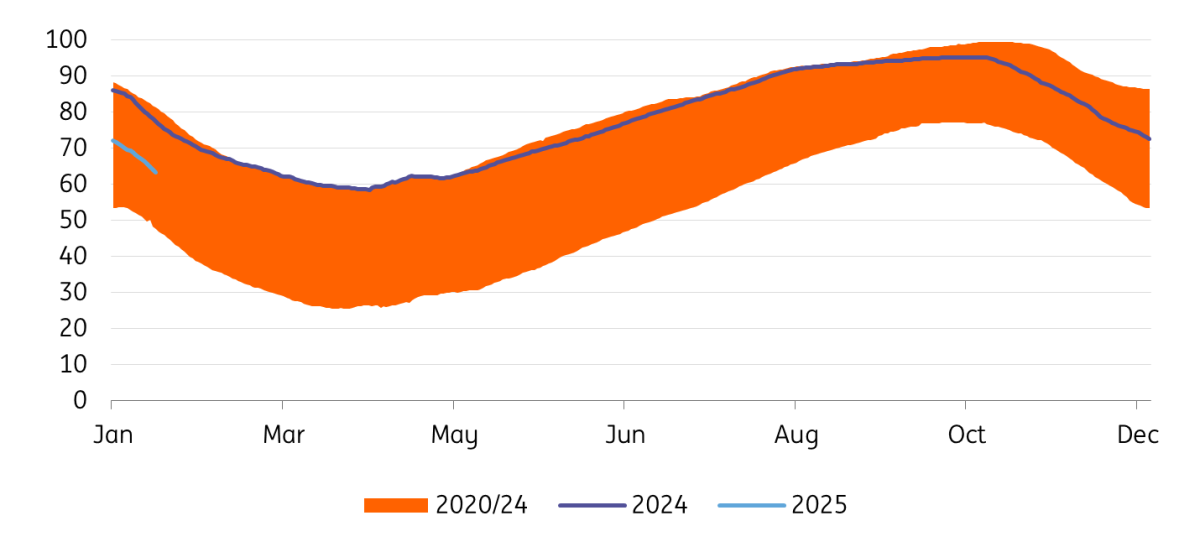

Stronger demand and reduced Russian flows have meant that Europe is drawing storage at a quicker pace this winter. Storage is well below year-ago levels and also lower than the five-year average. However, we still expect storage to finish this heating season at just below 40% full, compared to 58% last year and the five-year average of around 45%. Clearly, this is going to be dependent on how the weather plays out for the remainder of this heating season.

It is also important to point out that comparing expected storage levels at the end of this heating season to last year and the five-year average is not entirely a fair reflection of how tight the market is. The impact from Covid-19 and the two mild winters seen in 2022/23 and 2023/4 mean that both the five-year average and last year’s storage levels were unusually high.

Increased supply risks and the EU facing a bigger task in refilling storage mean that the downside in prices is likely less than we originally anticipated

However, the lower storage levels mean that Europe will face a bigger task in refilling storage over the summer months and hitting the European Commission’s target of having storage 90% full by 1 November. Expectations of stronger summer demand for storage are reflected in the forward curve with summer 2025 prices trading at an unusual premium to 2025/26 winter prices. The spread between summer and winter prices leaves little incentive for players to refill storage, so there may be a need for member states to take action to ensure mandated storage targets are met.

Recent moves in the JKM-TTF spread mean that Europe is pulling in additional LNG to ensure adequate supply. One factor helping Europe is weak Chinese demand so far this winter. Chinese buyers have reportedly been in the market to resell cargoes.

Furthermore, the global gas market will benefit from the ramping up of US LNG supply from Plaquemines LNG and Corpus Christi Stage 3. Once fully operational, this will bring in c.40bcm of additional LNG supply to the market. Unfortunately, the start of Golden Pass has been pushed into 2026.

There are clear risks facing the European market which leave it vulnerable. The global LNG surplus appears as though it has been delayed due to project delays. Meanwhile, the latest US sanctions against a couple of Russian LNG projects pose a risk to supply, although admittedly, these plants have relatively small capacity. The larger plants supplying Europe have not been sanctioned. Furthermore, there are reports that the EU is looking at a potential Russian LNG ban. However, this will have to be phased in given the disruptions it would cause if imposed in one go.

While we expect prices to trade lower through the year, increased supply risks and the EU facing a bigger task in refilling storage mean that the downside in prices is likely less than we originally anticipated. We expect TTF to average EUR36/MWh over 2025.

EU gas storage trending below 2024 levels & the five-year average (% full)

Call 3: EUA prices have bottomed

Having been under pressure for much of 2024 due to weak demand and stronger supply, EU Allowances (EUAs) have started 2025 on a strong footing with prices hitting their highest level since January 2024. Stronger gas prices, higher fossil fuel power generation, and stronger heating demand have all been supportive for EUAs so far this year. In addition, speculators, who were bearish on EUAs for much of 2024, are now holding their largest net long positions since August 2022.

We expect higher EUA prices this year relative to last year. We forecast prices to average EUR75/t, up from an average of EUR67/t in 2024. Offering support to the market is the further removal of free allowances for the aviation sector, further shipping sector emissions covered, and the market preparing itself for the start of the removal of free allowances for Carbon Border Adjustment Mechanism (CBAM) sectors from 2026.

Demand is still clearly a concern, particularly once we get through the winter months. Industrial activity in Europe remains sluggish, while the potential for escalation in trade tensions is another concern.

This year the aviation sector loses further free allowances, which is part of the gradual phasing out of free allowances for the industry. Free allowances were reduced by 25% in 2024 and will be reduced by 50% in 2025 (from the initial free allocation). For 2026, there will be no more free allowances for the EU aviation sector. This should provide some support to demand. Looking further ahead there is also the potential that the Commission includes emissions for flights departing from an EU airport to non-EU destinations, rather than just intra-EU flights, as is currently the case.

While the bringing forward of EU supply has been a bearish factor, the fact that supply from 2027 has been reduced by a similar amount should prove supportive for prices in the longer term.

Furthermore, 2025 will see more of the shipping sector’s emissions covered. 2024 was the first year of inclusion of the shipping sector in the ETS and as part of a gradual phase-in, only 40% of the sector’s emissions were covered in 2024. For 2025, this rises to 70% of the sector’s total emissions. And from 2026, 100% of emissions will be covered. Again, this is broadly supportive of demand dynamics.

In addition, while we are currently in the transitional phase of CBAM, from 2026 it will be fully implemented, which will see CBAM sectors starting to gradually lose their free allowances.

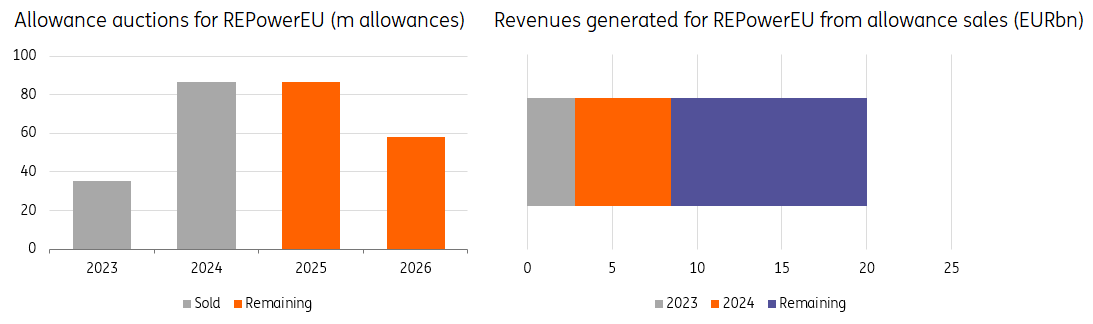

The selling of allowances to fund REPowerEU added to the downward pressure on EUA prices for much of 2024. The European Commission wants to raise EUR20bn from allowance sales in order to partly fund REPowerEU. This supply has come from the Commission bringing forward volumes which were set to be auctioned later in the decade. In total, the plan is to bring forward 266.7m allowances for auction between 2023 and 2026. In 2023, 35.2m allowances were sold, while in 2024, 86.7m allowances were sold. This has raised EUR8.43bn for REPowerEU. The Commission still has almost 145m allowances to auction between now and the end of 2026 and given the target to raise EUR20bn in total, this means that on average they would need to achieve a price of EUR80/t. This suggests that the EU will either have to sell even more allowances to achieve its EUR20bn target for RepowerEU or lower its target. If it is the former, obviously that would only provide further headwinds to EUA prices.

While the bringing forward of EU supply has been a bearish factor, the fact that supply from 2027 has been reduced by a similar amount should prove supportive for prices in the longer term.

Allowance sales for REPowerEU adds to the pressure for EUAs

ING forecasts

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

22 January 2025

Energy Outlook 2025: Growth amid challenges This bundle contains 7 Articles