Asia’s AI-chip trade growth continues to boom

We’ve seen extraordinary growth in semiconductor exports fuelled by the global tech cycle in many countries across Asia. US demand for AI-related chips is particularly strong. But geopolitical risks could become significant hurdles in the future

The most remarkable thing about Northeast Asian economies – South Korea, Japan, and Taiwan – is the robust growth in exports fuelled by an upswing in the global tech cycle. Strong demand for AI-related semiconductors and their equipment is the main driver here, supporting overall economic growth. We've been delving into the trade data to get a sense of the global trend of the vast semiconductor market.

South Korea: the biggest beneficiary of the AI tech boom

South Korea’s ICT sector (Information and Communication Technology) has seen strong growth, mostly due to the current upswing in the global tech cycle. Korean chipmakers are benefiting from the recent increase in AI technology investment in the US and the recovery in memory prices. In the first half of the year, Korean chip exports and imports grew 52.2% and 8.3% respectively – but in terms of volume, exports rose 35% while imports declined 30%.

South Korea's chip trade is growing strongly

The first half of 2024. The figures were boosted by favourable price effects

What stands out most here is the surprisingly large growth in chip trade with the US, mostly driven by strong demand for AI chips. This trend started in mid-2023, and we expect AI-related investment to continue at least until the first half of next year.

While Asia remains the main production hub in the global supply chain, we are now seeing differentiation emerge between countries. Vietnam, for example, is becoming a more important trading partner in the semiconductor sector. This is likely a result of escalating US-China technology trade tensions; with chipmakers diversifying their supply chains, Vietnam appears to be the biggest beneficiary. Meanwhile, chip exports to China recovered in the first half of this year – but this was mainly boosted by price effects. China and Hong Kong still take centre stage in the semiconductor industry, while South Korea’s trade in volume terms with China and Hong Kong has been shrinking since 2022.

AI chip demand will remain strong at least until 2025

According to industry reports, SK Hynix – the second-largest memory chipmaker – had been the sole supplier of its High Bandwidth Memory (HBM) to NVIDIA until March, which is known to command about 80% of the AI chip market. SK Hynix announced that its HBM chips used in AI chipsets were sold out for this year and almost sold out for 2025 (as of May 2024) as businesses aggressively expand their artificial intelligence services. It will also begin mass producing its latest HBM chips, the 12-layer HBM3E, in the third quarter. We, therefore, expect memory chip exports to accelerate faster in the second half of the year.

Major AI chip purchasers are keen to diversify their suppliers to maintain stable supplies and operating margins. The world’s largest memory chipmaker, Samsung Electronics, is expected to add its name to the supplier list soon. There is no official announcement as to whether or not the company has passed NVIDIA’s certification process, but NVIDIA revealed in early June that it was one step away from starting to supply. Even as more providers emerge, we don’t think oversupply will be an issue for the foreseeable future given the strong demand for AI technology and tight inventory conditions.

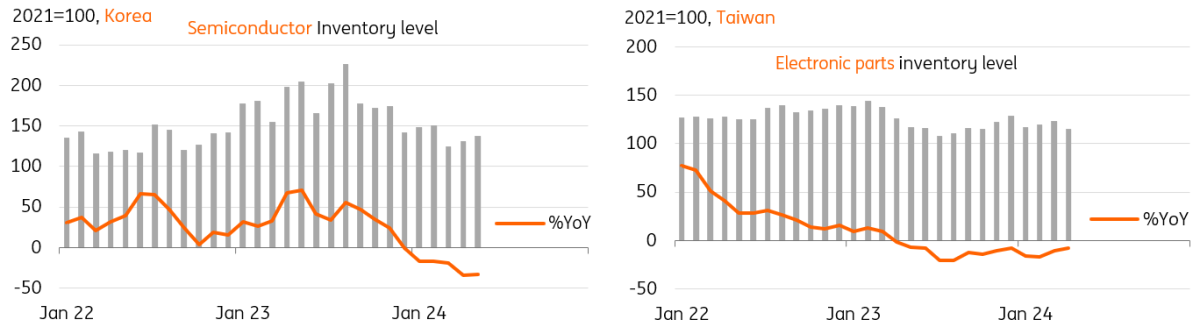

Tight inventory condition should work favourable for the inventory restocking cycle

Asia remains a global chip hub

In addition to high-end chip exports, inter-regional trade in semiconductors has also grown strongly, as the semiconductor supply chain requires several cross-border processes. Korean export data shows that its top 10 chip trade partners are all in Asia, further solidifying the continent's status as a global chip hub.

In value terms, Korean trade with China and HK combined accounted for more than 76% of total chip trade and, in volume terms, about 52% of total trade. We also found it interesting that Vietnam's role has grown significantly compared to a decade ago and that India, while still a minor player, seems to have recently entered the semiconductor scene.

South Korea's Top 10 chip trade partners

Geopolitics are never far away when looking at this sector. And the odds of Donald Trump winning the White House once again are increasing. His recent comments on Taiwanese defence have sent tech stocks tumbling and his 'America First' strategy would increase the risks for Asian chipmakers. While this is ultimately a threat, we believe that the dependence on Asian chipmakers is so large that they will not be easily replaced by potential US counterparts for some time.

And, let's be realistic. Trade tensions will continue to escalate regardless of who wins. But if Trump does return to office, US reshoring efforts will accelerate sharply over the next few years and create more hurdles for Asian chipmakers.

Developed economies play an important role in equipment

When we look at semiconductor manufacturing equipment, we see that developed countries still have a comparative advantage. Japan leads the market, followed by the US, Netherlands, Germany, and Israel. Equipment imports to South Korea declined during the first half of the year in both volume (-17.7%) and value (-4.5%) terms, but this could be due to the globalisation of production sites. Korean semiconductor companies are establishing production bases overseas, especially in the United States.

South Korea's imports of chip making equipment fell in 1H24

Japan: Tech export ban positively affects Japanese exports to China, ironically

In the semiconductor industry, Japan is not a semiconductor powerhouse compared to South Korea and Taiwan, but it does have a technical edge in semiconductor manufacturing equipment as shown by the Korean trade data in the previous section of this report.

Japan has been an active participant in the US sanctions against China on semiconductors, so we initially expected that Japanese exports to China would be negatively affected this year. However, it turns out that Japanese exports to China, particularly semiconductor manufacturing equipment, have increased sharply. Increased US efforts to slow down China’s semiconductor process development appear to be driving China’s pre-emptive purchases of chipmaking equipment in anticipation of tougher export regulations in the future. Thus, the export ban on technology has had a positive effect on Japanese exports to China for the time being.

While Japanese exports of semiconductor machinery to China have risen, exports to the rest of the world have been lacklustre.

Chip making equipment exports took off only to China

According to industry reports, China has been ramping up production capacity, mainly in the post-process stage, which includes packaging and testing. This is not subject to any sanctioned measures at this time. Photolithography products are for packaging that manufactures 28 nanometers or larger, meaning the technology is already over a decade old. In general, post-processing often involves the manual assembly of various parts and products. This is why most of the factories are concentrated in labour-abundant China and Southeast Asia.

Japan’s exports appear to be mainly photolithography equipment, which is exempt from the US’s tech export ban list. However, the post-process takes almost 76 % of the total share in foundries in the entire manufacturing process.

In the long term, the US is looking to lower its supply chain risk in China by batch-producing semiconductors in countries with friendlier relations. However, due to high labour costs, investment in automation technology for production lines is likely to take centre stage, with many companies, including Intel, TSMC and Samsung Electronics, investing in post-processing in Japan. The Japanese government has also designated semiconductors as an industry critical to economic security and has significantly increased its budget to support them. So, we expect Japanese investment in semiconductors to rise in the coming years and Japan to play a more important role in the post-process part.

The latest trade data confirmed that global demand for semiconductors is robust, with demand coming mainly from the US and China for different reasons. The market in the US is more related to AI technology, while demand in China is set to accelerate given efforts to improve technology self-sufficiency before trade bans are tightened still further. In fact, South Korean semiconductor manufacturers seem to be reducing their dependence on China, something that has been underway for the past year or two.

While the chip upcycle is expected to continue in the short term, geopolitical risks are likely to pose more of a hurdle for Asian exporters next year and beyond.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article