New Money V: Central Bank Digital Currencies may soon hit the wholesale market

Central banks may partner with financial institutions to introduce digital currencies within 5 to 10 years, in our view. But it's primarily businesses that will feel the effect. This wholesale approach is a likely first step towards universal adoption of CBDCs. It is less disruptive and makes global payments cheaper, 24/7 faster and more secure

Why wholesale CBDC?

In many countries, domestic payment infrastructure is being upgraded to make “real time” payments possible. Yet legacy payment infrastructure continues to have important shortcomings. While the front-end may be upgraded to allow real-time transactions, including outside office hours, the back-end infrastructure (for smaller payments at least) is based on batch processing, requiring periodic (e.g. end of day) downtime to process payment batches. Moreover, domestic systems tend not to be interoperable with each other across currencies.

Wholesale Central Bank Digital Currency will feature 24/7 instant payments across borders with settlement finality

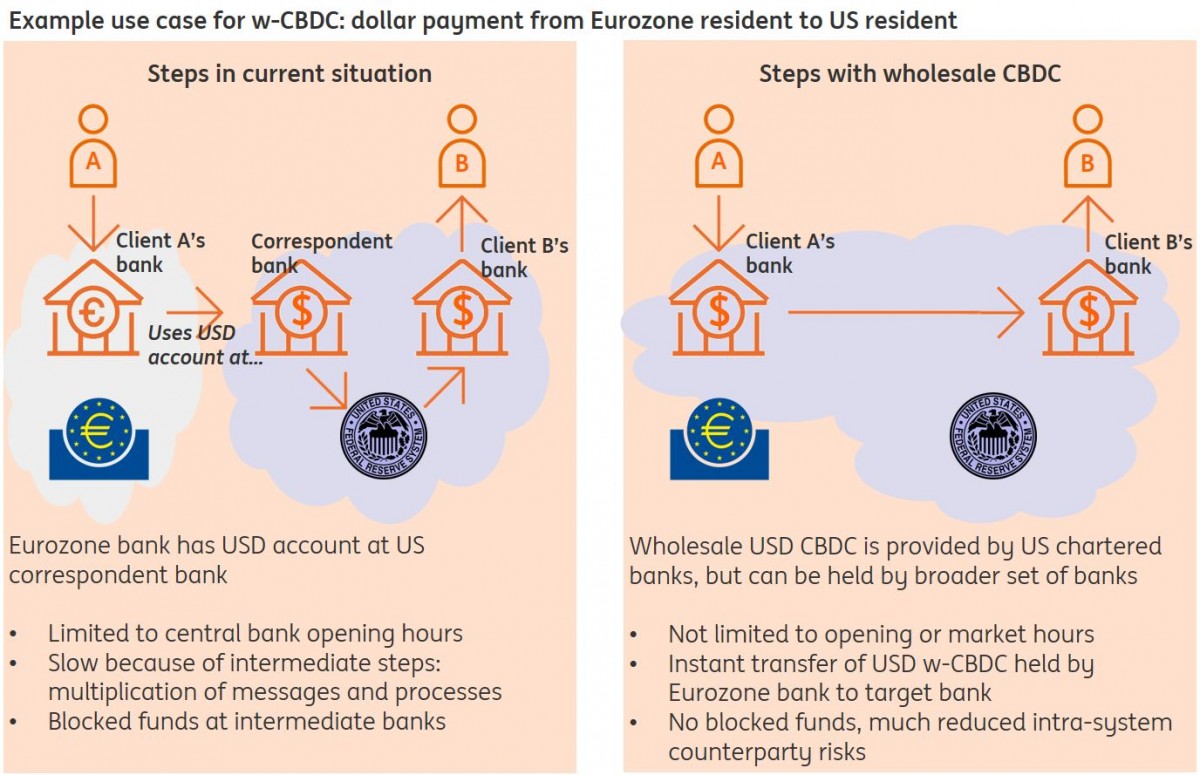

Wholesale Central Bank Digital Currency (w-CBDC) on the other hand, being built on state-of-the-art technology, will feature 24/7 instant payments across borders with settlement finality (meaning the recipient can be sure that the funds have been received, regardless of things like revocation attempts, payer insolvency or other reasons for non-delivery). Moreover, w-CBDC technology would allow linking to other platforms. Directly linking securities or FX platforms to cash platforms could improve the speed of trades and eliminate settlement risk. At this point, you may ask, doesn’t it already work this way?. Indeed exchanges already operate fast, centralised infrastructure. Still, settlement on OTC markets for example, stocks, bonds and derivatives, as well as for syndicated lending and trade finance, is still slow, and could speed up considerably if linked live to an instant w-CBDC system.

W-CBDC may also simplify (cross-border) payment infrastructure, strongly reducing the number of intermediaries involved. This improves efficiency and security, minimises liquidity and counterparty risks and reduces cost. A 2016 McKinsey report estimates that the average cost for a bank to send a payment across borders via correspondent banking is $25-$35.

Example use case for w-CBDC: dollar payment from Eurozone resident to US resident

Deploying today’s technology would also allow “smart” features to be added to w-CBDC, including earmarking funds, limiting their use in time and place, applying conditional interest rates and others. Such smart features would allow central banks to explore new and powerful operational monetary policy tools, such as tailor-made interest rates. It should be noted, however, that, in an environment where citizens are suspicious of new monetary tools against a backdrop of low or negative interest rates, central banks don’t appear very keen to investigate (see e.g. this IMF paper, chapter VI).

Real-time monitoring and track-and-trace on a unified platform should facilitate anti-money laundering efforts.

A unified payment ledger would allow central banks and prudential supervisors to monitor payment traffic in real time. This not only benefits them, but also private parties that may see their reporting requirements reduced. Real-time monitoring and better track-and-trace options on a unified platform should facilitate both anti-money laundering efforts by banks and supervision over those efforts.

Who is going to take the initiative to build w-CBDC?

Only central banks have the mandate to issue a digital token and call it legal tender. But they lack extensive experience and resources needed to build and maintain such an infrastructure and, for example, build a compliance apparatus to vet clients and transactions.

The private sector, on the other hand, has the necessary experience and resources to do this. Commercial banks also have an incentive. Regulation is becoming ever more stringent, and makes it more costly to maintain a presence in payment systems in multiple countries. Moreover, the current international payment system, based on correspondent banking, creates various costs such as KYC and handling costs of all banks involved. There are also delays due to opening hours in different time zones while liquidity is trapped in pre-funded nostro-accounts. A single cross-border 24/7 international direct payment and settlement system therefore is very attractive.

In order to build a successful w-CBDC, you need the private sector’s experience and the central banks taking away the various counterparty risks

But the private sector cannot build a w-CBDC system on its own for the simple reason that any liability it issues carries counterparty risk. While retail deposits are covered by guarantee schemes, this is not the case for large and wholesale deposits. Equally, privately issued w-CBDC tokens will carry counterparty risk. This applies, for example, to the widely covered announcement of JPM Coin. This will hold back adoption, as institutions will want to minimise their counterparty risks, preferring government bonds and central bank accounts, for example, over liabilities issued by private entities.

So in order to build a successful w-CBDC, you need the private sector’s experience and resources and central banks to take away the various counterparty risks. Moreover, jurisdictional differences need to be harmonised. So international public-private partnerships make sense.

If this seems controversial, keep in mind that the existing monetary system is already a public-private partnership of sorts. While central banks determine monetary policy and monitor financial stability, commercial banks actually create most of the money by lending. Central banks (and other government agencies) in turn license and regulate them.

| Cryptocurrency-based solutions | Commercial bank digital currencies | Wholesale CBDCs | |

|---|---|---|---|

| Examples | Ripple, Lumen, IBM Blockchain World Wire |

(Bank-issued) stablecoins, JPM-Coin |

USC (2), Jasper (3), Ubin (3) |

| Issued by | Non-banks | Commercial banks | Commercial and central bank partnerships |

| Collateral | None (1) | Commercial bank money | Central bank money |

| Target group | Financials | Wholesale | Banks, other financial institutions (4) |

| Settlement finality | No: probabilistic settlement with counterparty risk | No: counterparty risk | Yes |

| Legal framework | To be developed | To be developed | Existing |

1) Ripple: applies to XRP only. IBM: depends on digital asset chosen for transaction. 2) “Utility Settlement Coin”. 3) Jasper and Ubin are Bank of Canada and MAS research projects, respectively. 4) Monetary policy implications (see e.g. “The Narrow Bank” vs the Fed)

What next?

W-CBDC will have to compete with upgraded legacy systems. Payment systems are considered the “backbone of the economy” and can ill afford major downtime. Both central and commercial banks will therefore take it very slow when building completely new alternatives. Experiments are the way to go.

Cross-border wholesale CBDC involving multiple commercial and central banks should have the biggest chances at success.

Experimental w-CBDC that are cross-border from the start and involve multiple commercial and central banks, should have the biggest chance of success. We foresee prototypes built and tested in the years ahead. Over a 5-10 year horizon, a limited number of new wholesale digital currencies may emerge, competing with existing global payment networks. Network effects are strong in this industry, so time will tell which scheme will be the winner.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

21 June 2019

New Money: A new chapter for central banks and capital markets This bundle contains 6 Articles