National Bank of Hungary Preview: Pandora’s box

The outcome of the next rate setting meeting seems set in stone: rates will remain on hold. We think that the NBH doesn’t want to open Pandora’s box. We therefore want to pour cold water on some of the hot communication ideas about possible rate hikes and expect the central bank to balance the messages, to be hawkish, but not to go the extra mile just yet

The central bank kept its rate unchanged in October

The National Bank of Hungary (NBH) kept its base rate unchanged at 6.50% in October. The interest rate corridor also remained unchanged, with a range of +/- 100bp around the base rate. In line with its stability-oriented approach, this decision was driven by the significant weakening of the Hungarian forint due to global risk aversion shocks. Although there were some positive developments in the economy from a monetary policy perspective, the decision did not come as a big surprise due to market stability issues. Something similar can be said about the upcoming decision in November.

The main interest rates (%)

Inflation outlook and risk perception on the sidelines, again

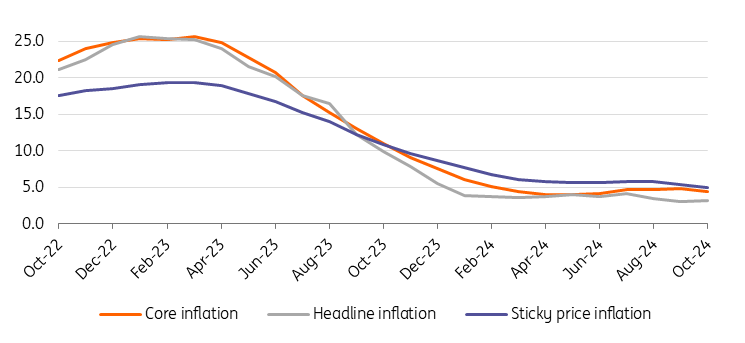

Headline inflation rose slightly by 0.2ppt to 3.2% year-on-year in October, below expectations. Services prices fell by 0.9% month-on-month, partly due to cheaper “other travel” (airfares) and health services, but the downside surprise was mainly due to an unexpected fall in telecommunication services prices (-6.8% MoM). However, it may be that this only reflects the impact of the free data packages offered during the September floods. If this is the case, then it was a one-off event that may re-accelerate inflation next month. Nevertheless, looking at the data, the picture is satisfactory in the short term, but there is a lot of uncertainty in the medium term, for example due to the expected high wage increase next year. All in all, the short-term inflation situation in itself could even have opened the door to an easing, but taking other factors into account, this is clearly no longer the case.

As far as risk perception is concerned, the National Bank of Hungary sees this through the lens of fiscal developments and external balances. The October budget deficit was the second largest since 2002, but this could also be a one-off event due to the September floods. The government has published the draft budget for 2025, which aims to maintain the previously telegraphed deficit level of 3.7% of GDP, and it looks more or less realistic, although we could point to several risks. On the external balances side, we haven't seen any significant deterioration from recent trends. All in all, risk perceptions alone won't play a major role in the decision-making process this time.

Headline and underlying inflation measures (% YoY)

Financial market instability drives monetary policy decision

Under normal circumstances, the inflation picture and risk perceptions might move the needle a little towards easing, but with the instability in the financial markets, this idea is no longer a possibility. And the door to easing has been slammed shut, judging by the central bank's latest communication.

Since the last NBH rate-setting meeting (22 October), core rates have moved significantly higher, with both the short and long ends of the US yield curve rising by around 25bp by 13 November. The 10-year Bund also moved higher by around 7bp. This time, however, such a move in core rates did not translate into a higher risk premium for Hungarian government bond yields, as the spread between 10-year HUF and PLN government bond yields narrowed by 7bp compared to the October meeting.

The EUR/HUF exchange rate is therefore now the key issue for financial market stability. Since the October meeting, the exchange rate has moved sharply higher on the back of rising geopolitical risks and the outcome of the US presidential election, with Trump and the Republicans winning big. The already fragile currency and these changes pushed EUR/HUF to as high as 412 (3% weaker than mid-October), and the forint remained the underperformer from a regional perspective. A clear red flag in this currency move is that the market has already priced out the possibility of rate cuts in the coming months. This also means that an on-hold decision will be in line with market expectations, which is crucial given the HUF's vulnerability.

Performance of CEE FX versus EUR (end-2023 = 100%)

Our call

In our view, the National Bank of Hungary will leave the interest rate complex unchanged at its next rate setting meeting on 19 November. This will leave the key interest rate at 6.50%, which is a high conviction call. We also expect the Monetary Council to leave both ends of the interest rate corridor unchanged.

As the market has the same expectation, the focus will be on the communication and the forward guidance itself. While some may expect an open communication on rate hikes, citing an emergency case, such an admission itself could turn out to be a self-fulfilling prophecy and would be premature. We also don't see the central bank pulling the trigger on any kind of liquidity tightening right now, as all possible options have some limitations and could open a Pandora's box for the markets to test the central bank's pain thresholds. We therefore expect the central bank to balance the messages, to be hawkish but not to go the extra mile.

Looking further ahead, we do not expect another rate cut under the current administration (end of February 2025), and while this is not a high conviction call, the new administration will probably not be able to start cutting rates immediately either. We see the dollar continuing its gradual strengthening, the current account could weaken and there could also be some slippage in the budget. All things considered, we expect the cycle of rate cuts to continue, but not until next summer.

Our market views

In pre-election market positioning, the HUF was one of the most short currencies in the EM space, however, the market reaction disappointed, allowing some short position closing and relief for the HUF. However, the market quickly reverted back to the original view of a Trump negative scenario for CEE. Indeed, we should see weaker performance in the CEE region, global trade headwinds and more room for rate cuts in general. The HUF has fallen from an already weak position into a global view which makes a problem for a potential recovery of the currency. Positioning is probably a bit softer than before the election but still clearly short HUF.

At the same time, the market has stopped pricing rate hikes into very front-end FRAs. This tells us that while the market is not aggressively negative on HUF assets, it is also too early for any major relief and the market has room to add shorts if it sees reason, which could be both local and global. Next week's NBH meeting may put the HUF under pressure again. We thus expect EUR/HUF to remain around 410 with constant pressure from the dollar. And in the medium term, we expect EUR/HUF to move higher to 420 next year. The market has outpriced almost all rate hike expectations from very front-end FRAs and FX implied yields, while two rate cuts have returned to pricing in the longer term after the HUF market saw some relief after the US election. Valuations still look cheap in both IRS and HGBs from this perspective. However, as with FX, it is hard to see a major rally here at the moment. Although local data of low inflation and weaker growth would indicate more rate cuts, it seems clear the NBH does not want to go in that direction for some time and the risk of a rate hike has not been completely taken off the table by the market given the fragile FX. Still, in these conditions the belly and long-end should have some chance to normalise slightly and revert some of the steepening we've seen in previous months. Overall, we prefer to wait a bit longer on the sidelines here before we see any major signs of relief.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article