National Bank of Hungary preview: Chasing stability

The October rate-setting meeting had the potential to be interesting, but due to financial market instability, the outcome is now clear. We expect the National Bank of Hungary to maintain the base rate at 6.50%, with hawkish forward guidance

The central bank cut rates in September

Following a brief pause in the easing cycle, the National Bank of Hungary (NBH) resumed its rate cuts in September, reducing the key rate by 25bp to 6.50%.

This decision was supported by the four key factors previously highlighted in our NBH Review here, all of which were essentially met. However, the past month has seen an unfavourable turn of events.

The main interest rates (%)

Inflation outlook

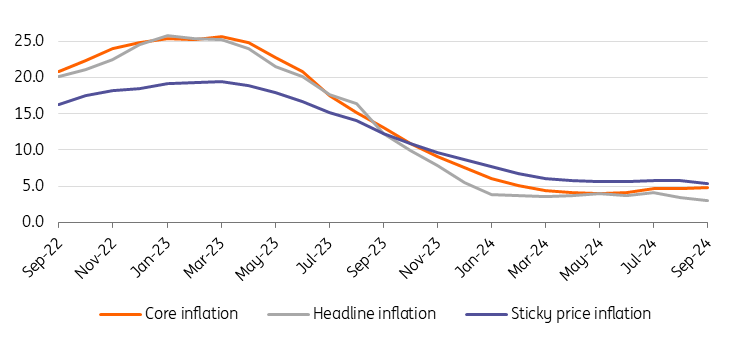

Headline inflation slowed by 0.4ppt to 3.0% YoY in September, reaching the central bank's target for the first time since January 2021. The data release was a slight downside surprise compared to market expectations, as well as the central bank's inflation trajectory outlined in the September Inflation Report. More surprisingly, core inflation came in at 0.0% on a monthly basis, largely due to a significant decline in services prices. Therefore, we can conclude that several indicators point to some improvement in the underlying inflation picture.

What also improves the overall inflation outlook is weak economic activity, which poses less of a pro-inflationary risk. The high-frequency activity data from the industrial and construction sectors for August are all worrisome for the performance of the economy in the third quarter. And while the retail sector provided an upside surprise, it appears to be more of a one-off rather than a systemic change in growth trajectory.

Moreover, the monthly fiscal developments in September brought us closer to a flashing red light for GDP growth, as the surplus had more to do with Brussels than the domestic economy. Against this backdrop, we see an increasing risk of weaker-than-expected growth in the short term.

When it comes to risk perception, the National Bank of Hungary sees this through the lens of budget developments and external balances. The September budget surplus itself improves the feasibility of the 2024 fiscal target. When it comes to the fiscal outlook for 2025, the government has yet to reveal the draft budget (due in November).

Last but not least, the usual autumn revision of the balance of payments brought a significant positive change in the current account balance in 2023 (+0.5ppt to 0.7% of GDP). In contrast, the preliminary monthly data for July and August show only a minimal surplus overall, compared to the significant surpluses of the previous months. So, while we see a bit of a mixed bag here, none of it was significant from a risk perception perspective.

Under normal circumstances, these developments would have strongly supported continued monetary easing in October. However, this time, financial market stability was the deciding factor that halted the process.

Headline and underlying inflation measures (% YoY)

Change in financial market stability is the deal-breaker this time

Since the last NBH rate-setting meeting on 24 September, core rates have significantly trended higher, with the US 10-year yield rising by almost 30bp by 16 October. The short end of the US yield curve also moved up by around 40bp. The direction of the German yield curve was broadly similar, with less pronounced amplitudes. The spread between 10-year HUF and PLN government bond yields widened by 7bp during this period.

However, the EUR/HUF exchange rate is the key issue for financial market stability. Since the September meeting, the exchange rate has been drifting higher on expectations of a local rate cut. In addition, rising geopolitical risks met the already vulnerable currency and the EUR/HUF reached 402. Since then, the forint has been hovering close to that level, despite verbal interventions from the National Bank of Hungary.

Following the indication that maintaining rates in the short term is the rational choice, expectations for aggressive easing have decreased. Based on the FRA curve, investors anticipate a year-end rate of 6.20, suggesting they expect only one rate cut before the year’s end.

Performance of CEE FX versus EUR (end-2023 = 100%)

Our call for October

In our view, the National Bank of Hungary will leave the interest rate complex unchanged at its next rate-setting meeting on 22 October. This will leave the key interest rate at 6.50%, which is a high conviction call. We also expect the Monetary Council to leave both ends of the interest rate corridor unchanged.

Our baseline scenario for a low point in the base rate in 2024 remains at 6.25%, which implies another rate cut in the fourth quarter of this year, probably in December. However, for this to happen, we need a significant improvement in the exchange rate and/or a significant improvement in the risk perception of the Hungarian economy.

Overall, we believe that the Monetary Council will present a new hawkish forward guidance to improve the chances of such a change. The cautious, patient and stability-oriented approach will remain in place, even in a super-data-driven mode, with the assumption that there will only be room for another rate cut if the situation regarding the inflation outlook, risk perception and market stability is optimal.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article