National Bank of Hungary preview: The chance of a cut this year has vanished

- 24 April

- Hungary

Elections have taken place in Hungary, but there are still many unanswered questions, especially about the effects of geopolitics. The uncertainty surrounding Hungary is preventing any alteration to the base rate, and we don't expect this to change for the rest of the year

Our call

As noted a month ago, the war in the Middle East pushed the National Bank of Hungary towards a more hawkish stance. Since then, geopolitical pressures have remained firmly in place. This is consistent with the removal of the final sentence of the March forward guidance, the “meeting-to-meeting” remark regarding the decision-making process.

The factors of uncertainty surrounding Hungary’s stability have not diminished either. Parliamentary elections have taken place, resulting in a change of government. While the worst-case scenario from a stability perspective — a hung parliament — was avoided, many questions remain about the economic and fiscal outlook for the coming period. Despite market movements that could give the NBH greater scope for manoeuvre, we believe the central bank will adopt a wait-and-see approach at next Tuesday's meeting.

The continuing high level of uncertainty surrounding the war in the Middle East suggests that the NBH will keep interest rates unchanged at 6.25%. While it is true that the economy is better placed to absorb the impact of higher energy prices than in 2022, the persistence of high levels of geopolitical uncertainty certainly limits monetary policy flexibility.

As a starter, a rate cut is definitely out of the question for April, and this is a high-conviction call. We expect the central bank to adopt a hawkish tone in an attempt to influence FX market stability, keeping the EUR/HUF at lower levels. We expect the Bank to demonstrate maximum flexibility in order to convince market players and present an image of strength, calmness, patience and caution.

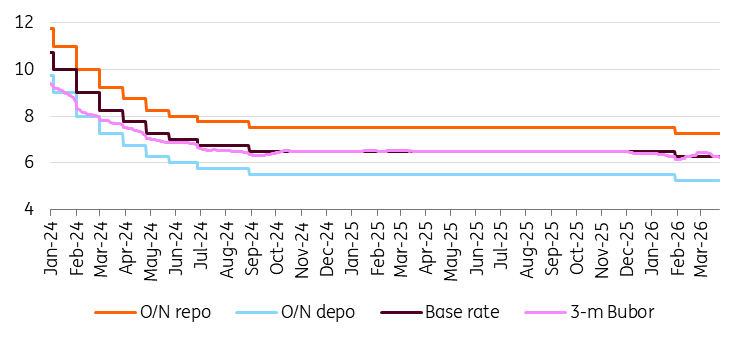

The main interest rates (%)

The protracted nature of the Middle East conflict has forced us to make meaningful revisions to our official scenarios, including the baseline. These developments are set to weigh heavily on Hungary as well. Based on the updated baseline scenario for energy markets and major central banks, which is more pessimistic than before, we forecast that Hungarian inflation will continue to accelerate for the remainder of the year. We expect it to average 3.5% in the second quarter, rise above the tolerance band in the second half of the year and average 4.3% in the final quarter. Given that energy prices remain higher than before and due to their impact on Hungary, we currently see no scenario indicating an interest rate cut this year.

However, if the worst-case scenario materialises, inflation would rise significantly, exceeding 6% during the third quarter. The NBH could not ignore this and would be forced to raise interest rates.

Our market views

The forint has strengthened against the euro by around 3.2% since the general election in April and by 5.2% just at the beginning of the month. We saw even bigger gains against the US dollar. The market sees the elections as a restart of relations with the EU, which should bring a number of benefits to the economy. We remain bullish here in general, but it is necessary to take into account the heavy long positioning that has built up in the market in recent weeks. This will undoubtedly slow down further strengthening of the forint, and we will rather see a gradual grind of EUR/HUF down.

On the other hand, the NBH is in no hurry to cut rates, and FX carry remains solid. The risk at the moment could be sudden profit taking if the market sees any disappointment from the new government, but this does not seem like an imminent risk, given that it has not yet been appointed, or a significant escalation of global energy prices, where Hungary still remains the most exposed country in the region. However, overall, we see further gains for the forint in the medium term and think that 350 by mid-year should not be too difficult a target in our forecast.

In the rates space, the market is already pricing in two rate cuts in the one-year horizon, but not in the coming months. However, the central bank will not rush, and we won't see much of a visible dovish shift due to significant FX strengthening. We are still in the middle of an energy shock with an unclear end; short-term pricing may see some pressure next week.

Since the election, market behaviour has repeatedly shown that investors remain broadly bullish on Hungary despite the strong post-election rally. Sell‑offs are quickly faded, especially at the long end, which some might see as the most attractive. We therefore expect further curve flattening and continued compression of the country premium at the long end.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more