Mounting US job fears to push the Fed into action

Everything was weak in the July jobs report. The one crumb of comfort is that the jump in the unemployment rate is being caused by surging labour supply rather than workers being fired, but with demand indicators looking soft and jobless claims on the rise the risks are skewed towards unemployment increasing more rapidly. Rate cuts are on their way!

| 4.3% |

The US unemployment rate |

| Higher than expected | |

Everything is weak

The July US jobs report really makes the case for Federal Reserve interest rate cuts. Everything is weak. Non-farm payrolls growth of just 114k with 29k of downward revisions to the past two months (consensus was 175k). Private payrolls grew just 97k while wage growth comes in at only 0.2% month-on-month, the working week shrinks to 34.2 hours AND the unemployment rate rises to 4.3% (above every forecast in the market). This triggers the Sahm Rule that suggests whenever the 3M average of the unemployment rate rises by more than 0.5ppt in a 12M period we get a recession.

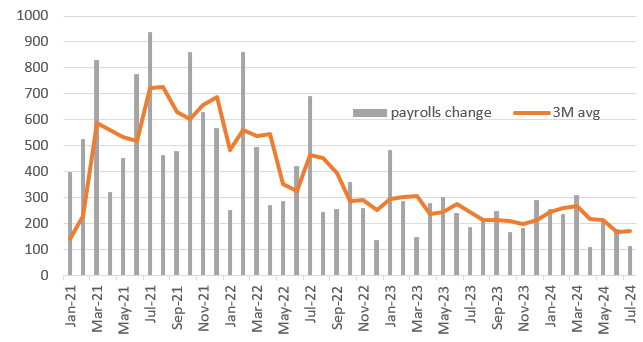

We already had three 25bp cuts priced for this year as of yesterday, but we are going to see the market gunning for one of those being a 50bp now. Treasury yields are plunging and the dollar is getting a battering as the prospect of a 3% Fed funds rate next year looks increasingly realistic. Below is a chart of payrolls growth and the 3M average (000s).

Monthly change in non-farm payrolls (000s)

Details don't offer any encouragement

The details offer very little comfort. In terms of payrolls we had outright falls in employment in financial (-4k), information (-20k) and professional business services (-1k). Construction was a bright spot, adding 25k, but with housing construction not looking in the best of health we are not sure how long this can last. Once again, the usual three sectors of private education and healthcare services (+57k), government (+17k) and leisure and hospitality (+23k) are where the jobs are being added. These are not sectors that you would necessarily be expecting to be driving growth of the US economy.

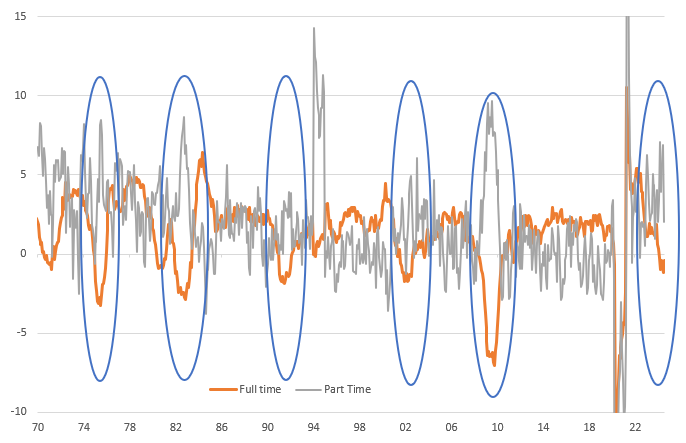

It is the increase in the unemployment rate that is going to attract most of the attention though and the only positive thing I can say is that it is being caused by rising labour supply growth exceeding demand for workers rather than outright job losses – household employment rose 67,000 while unemployment rose 352,000. However, with initial and continuing jobless claims appearing to be on the rise we can’t rule out the possibility that by late this year the moves in the unemployment rate could be accelerated by job losses. Certainly the ISM employment indices and the NFIB hiring intentions don’t look good. Moreover, the year-on-year declines in full-time employment are always a warning sign of impending recession threat, especially when part time is spiking higher, suggesting firms are reluctant to replace retiring or quitting workers with like for like replacements – the first stage of cost cutting! (see chart below of YoY change in employment).

YoY change in full time and part time employment

The Fed won't stand back from easing

We have long been in the camp expecting the Fed to be more responsive to a cooling economy, resulting in more rate cuts than both the Fed and the market were anticipating. For now we are sticking with our three 25bp cut view for this year, but the risks do increasingly appear to be skewed to more aggressive action, especially in early 2025 we suspect. The Fed remain wary about inflation, but this week’s employment cost index and unit labour cost data should really have boosted their confidence that inflation is on the path to 2%. Their focus needs to be the state of the jobs market.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article