US: The job’s not done…yet

Three interest rate cuts and easing trade tensions have calmed fears about a potential US recession, but we think the market's reaction is excessive. With the economy decelerating and politics likely to remain a source of uncertainty, we believe the Federal Reserve has more work to do to ensure a slowdown doesn’t become more severe

Markets are in a happy place

Looking at financial market moves since the summer you would have to say that policymakers and politicians have done a fantastic job in calming nerves about a potential US downturn. August was a rocky month with equity markets coming under pressure and the US 2-10-year Treasury yield spread inverting – a signal that typically portends a recession.

But now, markets seem to be of the view that the three rate cuts from the Federal Reserve and the easing of US-China trade tensions, backed up by stimulus elsewhere and better optics on European politics (think Brexit and Italy) means a potential crisis has been averted. After all, equities are up at all-time highs, the yield curve has re-steepened, credit spreads have narrowed and the dollar remains the currency of choice.

Equity and bond market optimism returns

But we remain cautious

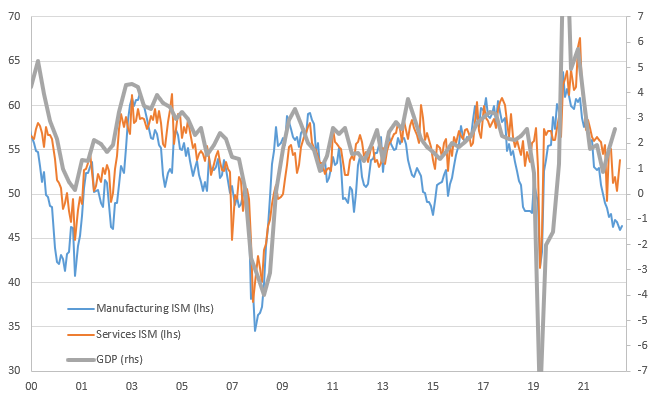

Unfortunately, we have our doubts on how sustainable this is and think there is more work to be done. The troubles facing manufacturing are plain to see. Weak global growth and trade tensions have hurt demand and sentiment with the headwinds from a strong dollar compounding the problems for US manufacturers. The ISM manufacturing index has been in sub-50 contraction territory for three consecutive months with the production component at its lowest level since 2009 while official figures show manufacturing output is down 1.6% year to date.

There is evidence that the weakness in this sector is spreading with the ISM non-manufacturing index on a softening trend and the National Federation of Independent Businesses survey at its lowest level since Donald Trump won the presidency. Moreover, business investment has contracted for two consecutive quarters with the durable goods orders report suggesting we could see a third consecutive fall in 4Q.

ISM indices point to slower growth

The economy is slowing, but a recession looks less likely

This indicates that businesses are reluctant to put money to work and it tallies with the slowdown in employment growth seen over the past eighteen months.

Having averaged 223,000 jobs per month throughout 2018, employment creation is running at a net 167,000 for 2019. The slowdown would have been even more marked had it not been for consecutive gains of 48,000, 45,000 and 61,000 in the leisure and hospitality sector. The fact that this one, relatively modest-sized (and lower-wage and lower-skilled) component was responsible for 30% of all the jobs created in the past three months underlines the weakness in other sectors.

For now, the story is one of a gradual slowdown in US growth rather than a recession

The news from the consumer sector also hints at slowing growth, albeit from a firm rate. Retail sales have recently been soft and auto sales are weaker in October while consumer confidence is off its highs. With wage and payrolls growth both looking relatively modest, real household disposable incomes don’t signal a major upturn in spending growth is likely. Meanwhile, the sharp increases in longer-dated Treasury yields is pushing up mortgage and other borrowing costs, which will be a headwind for consumer activity more broadly.

For now, the story is one of a gradual slowdown in US growth rather than a recession. As such the Fed has signalled a preference to pause for a while after cutting rates in July, September and October. Fed Chair Jerome Powell suggested “monetary policy is in a good place” and that they want to take stock of the impact of their actions before considering additional stimulus, which clearly hints at “no change” at the December meeting.

The jobs market is showing vulnerabilities

Key risks remain

It's worth noting recent data flow has been consistent with that narrative. After all, the ISM non-manufacturing index has improved a little and the October payrolls report was not as bad as feared. With the November payrolls report set to be lifted by 40 - 45,000 after the end of the General Motors workers strike, the data should stay consistent with stable policy in December.

Moreover, the US and China look set to sign a phase one deal on trade that suspends proposed tariffs in exchange for China buying more US food and agricultural products, which is boosting sentiment. In fact, there has been some talk about the potential rolling back of some of the tariffs already implemented - the 15% tariff on around $111bn of Chinese imports (largely consumer goods) that came into effect on 1 September.

We think it is too soon to sound the all-clear on downside US growth risks and with inflation and inflation expectations looking benign we continue to see scope for the Fed to cut rates twice more

It would be in response to China making concessions on rules regarding currency manipulation and potentially also offering concessions on intellectual property protection. It would make the deal broader than initially envisaged, although we would caution that this proposal could yet be dropped with some in the US administration vocally opposing a rollback of tariffs. Either way, it would still leave significant tariffs and barriers to trade in place so it would be more of a stabilisation of relations rather than a major boost to growth at this stage.

There are other trade-related political risks. President Trump has to make a decision on whether to implement tariffs on EU made cars and car parts after postponing the decision in May. At this stage we suspect he will postpone again, not least because there is growing recognition over how significant European carmakers are to US manufacturing – for example, the BMW Spartanburg plant in South Carolina has been announced as the biggest US auto exporting plant for the fifth year in a row, and there have been significant investments by other European automakers within the US.

There is also the potential for another government shutdown with the latest short-term spending bill set to expire on 21 November. If Congress and the President can’t agree a year-long budget that would get the US through to next year’s elections then there is the possibility of government workers being sent home soon after Thanksgiving. We would assume neither side wants to risk taking the blame for an unnecessary and economically damaging situation to develop, but the impeachment process against President Trump could increase tensions and make reaching an agreement more challenging.

Recession risks have declined in the US, but the loss of economic momentum is clear and there is little to suggest we should expect an imminent re-acceleration in growth. Moreover, asset markets have reacted very positively to news of a trade truce and better news about Brexit and European risks. However, as you will see, our team is less sanguine about these threats.

Consequently, we feel markets and the global economy are likely to experience more bumps in the road. We, therefore, think it is too soon to sound the all-clear on downside US growth risks and with inflation and inflation expectations looking benign, we continue to see scope for the Fed to cut rates twice more.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

8 November 2019

November Economic Update: Trading the positives This bundle contains 9 Articles