Monitoring Turkey: Balanced economy still some way off

Turkey's fourth-quarter GDP data showed that private spending has accelerated despite an increasingly restrictive policy stance while leading indicators point to a further acceleration in GDP growth in the first quarter of this year. This implies that there is still a long way to go to rebalance the economy

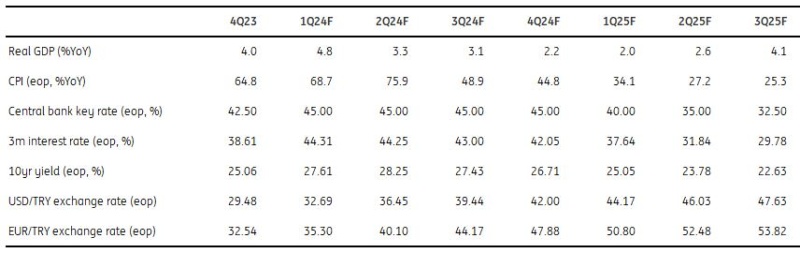

Turkey at a glance

- Given the still-high growth rate of private consumption in the fourth quarter and continuing strength in the early indicators, we have revised our growth forecast for this year from 2.5% to 3.3%.

- With the higher-than-expected monthly reading, annual inflation turned out to be 67.1% year-on-year, up from 64.9% a month ago on the back of an across-the-board increase in prices. We expect a further increase in the near term. Given also that the recent depreciation in the Turkish lira has been stronger than anticipated, we have increased our inflation forecast for this year from 42% to 45%.

- When we look at the momentum in loan growth, the trend has shown signs of acceleration lately, driven by retail and SME loans. Accordingly, the Central Bank of Turkey decided to reduce the monthly growth limit from 2.5% to 2% for TL commercial loans, and from 3% to 2% for general-purpose loans.

- The CBT also decided for banks to hold the part exceeding growth limits in loans as part of the required reserves for one year. These moves show that the CBT continues tightening via macro-prudential measures and quantitative tools.

- We do not expect rate cuts this year any more. Given the deterioration in price dynamics and the underlying trend remaining above the CBT's projection for the first half of the year, inflation prints for March and April will be key to the bank’s actions given its clear forward guidance that the monetary policy stance will be tightened “in case significant and persistent deterioration in inflation outlook is anticipated”.

Quarterly forecasts

Strong GDP growth with private consumption

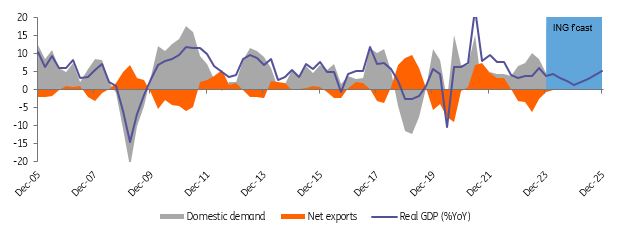

Turkish GDP growth in 4Q turned out to be 4.0% on a year-on-year basis, better than the market consensus at 3.5%, on the back of a rebound in private consumption. This was despite some moderation compared with the previous quarters, and robust investments. Accordingly, 2023 GDP growth decelerated in comparison to a year ago but recorded a strong rate of 4.5% YoY. 4Q GDP translates into a quarter-on-quarter growth rate of 1.0% after seasonal adjustments, showing momentum in comparison to a relatively modest reading in 3Q of 0.3%. Accelerating sequential performance is attributable to the positive turn in household consumption after a negative reading a quarter ago and the supportive impact of net exports despite negative contributions from an inventory build-up, government consumption and investment.

Real GDP (%YoY) and contributions (ppt)

PMI recovered to above 50 threshold

The manufacturing sector PMI, which had been below the 50 threshold in the second half of 2023 and the first month of this year, turned to expansionary territory, at 50.2 in February. Attributable to a stabilisation in demand, this reading signals an improvement in business conditions. In the breakdown, the data shows: i) renewed expansion of manufacturing output, ii) signs of recovery in customer demand, iii) a slowdown in new orders and new export orders to a lesser extent iv), increasing purchasing activity of firms in the sector v) a moderation of employment, vi) rising input costs, reflecting exchange rate developments and the recent wage adjustments (though easing marginally in comparison to previous months) vii) increasing output prices at the fastest pace since August last year.

IP vs PMI

Broader definition of unemployment on the rise

The seasonally adjusted unemployment rate inched down to 8.8% in December from 8.9% a month earlier and in the last quarter of 2023 was close to the lowest level since late 2012. The composite measure of labour under-utilisation, which is the sum of time-related underemployment, unemployment and the potential labour force, increased by 2.1ppt in December compared to the previous month and turned out to be 24.7%. This indicator has been on the rise in the last two months, from 21.4%, now standing at the highest since mid-2021. According to the quarterly data, the unemployment rate continues to decline and has been in single digits in all quarters of 2023. The 4Q reading stood at 8.8% with a continuous decline during the entire 2023. The improvement in the last quarter is attributable to strong employment, recording a 195K increase. This contributed to a 137K decline in the number of unemployed despite a growing labour force of 57K.

Retail sales vs consumer confidence

Turkey faces continuing price pressures

With February's month-on-month inflation figure for Turkey at 4.53%, which was above our call and the consensus, annual inflation came in at 67.1% YoY up from 64.9% a month ago on the back of an across-the-board price increase. Accordingly, cumulative inflation in the first two months reached 11.5% vs the 36% central bank forecast for this year, while annual inflation has remained above the CBT’s forecast range of 30-42%. Core inflation (CPI-C) came in at 3.6% MoM, moving up to 72.9% on an annual basis on the back of pricing behaviour, implications of the minimum wage and public salary hikes, the adjustment in administered prices and inertia in services. Relatively subdued exchange rate moves have recently supported the inflation outlook. On a seasonally adjusted basis, after the spike in January, core inflation improved markedly thanks to core goods, while services have maintained a solid underlying uptrend. As a result, despite some easing, the headline inflation trend has remained elevated at above 4% MoM. The CBT sees seasonally adjusted monthly inflation hovering below 4% on average in the first half of this year (around 3% except for January). This implies that disinflation should be more pronounced in the coming months for the CBT forecast to hold.

Inflation outlook (%)

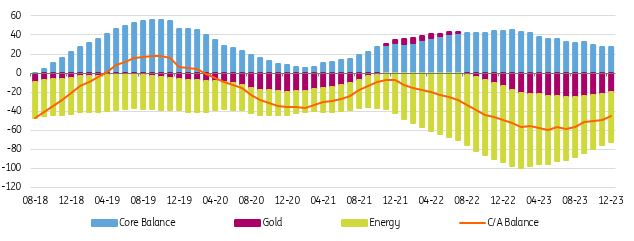

A modest improvement in the current account deficit

Turkey's current account in December posted a deficit of US$2.1bn, lower than the market consensus. The 12-month rolling current account (C/A) balance, on the other hand, showed a modest improvement last year due to a narrower goods deficit amid i) declining energy bills (from US$80.1bn to US$52.7bn) and ii) some recovery in services income thanks to stronger tourism. However, a swing in gold imports to a large deficit and the turn from a surplus in the core balance (excluding gold and energy) to a deficit limited the extent of improvement in the current account. Accordingly, the figure showed a $45.2bn deficit (translating into c.4.3% of GDP) at the end of 2023 vs U$49.1bn in 2022. On the capital account, despite the monthly C/A deficit and large outflows via net errors & omissions, official reserves recorded a $2.0bn increase thanks to the relatively better shape of the capital account in recent months. For the whole of 2023, despite higher inflows at US$53.8bn and large reserve accumulation after the elections, official reserves actually declined by US$2.0bn. This was driven not only by the large C/A deficit but also by US$10.7bn of outflows via net errors & omissions (vs large US$26.2bn inflows in 2022 at US$36.9bn).

Current account (12M rolling, US$bn)

Budget balance remains under pressure

The budget balance showed a favourable course until December due to high tax increases in July 2023, the boosting effect of inflation and continuing strength in domestic demand. However, in December, the budget deficit deteriorated significantly on the back of the accrual of earthquake expenditures that were not actually realised. Budget data for January also indicates continuing pressure, particularly due to interest payments. Given this backdrop, the recent acceleration in the budget deficit points to additional challenges in the disinflation process. While the current outlook implies expenditure-cutting and revenue-raising measures that will not create inflationary pressure, Treasury and Finance Minister Mehmet Simsek recently stated that the government does not plan across-the-board tax increases in income tax, corporation tax or value-added tax.

Budget performance (% of GDP)

CBT keeps policy rate flat and maintains tight stance

The central bank has signalled that the current policy rate (45%) is tight enough to trigger disinflation, though it has signalled that a further deterioration in inflation could unlock further rate hikes. It has adopted a “higher for longer” stance until there is a sustained decline in the underlying trend in monthly inflation and inflation expectations converge to the projected forecast range. The bank expected seasonally-adjusted monthly inflation to hover below 4% on average in the first half of this year, reaching 1.5% in the fourth quarter, implying strong disinflation. Any diversion could see a possibility of higher rates, and market participants are projecting higher inflation than the central bank. The CBT, meanwhile, has pledged further macro-prudential moves, potentially targeting credit expansion, likely credit card growth, and downward pressure on deposit rates in the period ahead. Against this backdrop, the CBT expects real TRY appreciation, an explicit reference to ease any concerns about the currency.

CBT funding rate (%) vs FX basket

FX and rates outlook

Net foreign exchange reserves, which increased rapidly in November and December due to strong foreign portfolio inflows, have been on a downward trend since the beginning of this year. The price action in lira and the decline in reserves suggest continuing onshore demand for hard currency, likely driven by the high seasonal current account deficit in the absence of large tourism revenues. In this environment, the central bank has maintained a hawkish stance with a determination to keep rates high and monetary conditions tight.

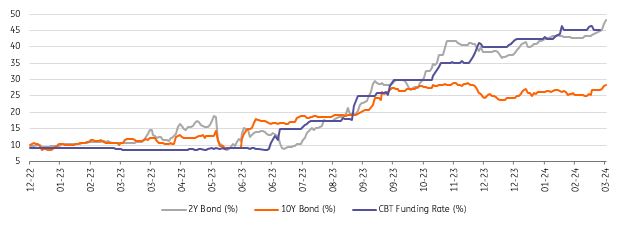

Regarding local debt, since early January, bond yields have been on the rise as 2-year bond rates moved from below the 40% level to above 45%, while back-end yields have also moved higher as well, now the 10-year is trading close to 28% vs below 25% towards the end of December. However, the rising inflation path in the near term is still a concern adversely impacting real returns. We saw US$3.8bn of inflows between early November and mid-January, though there has been some weakness lately with a mere US$450m on a year-to-date basis.

Local bond yields vs CBT funding rate

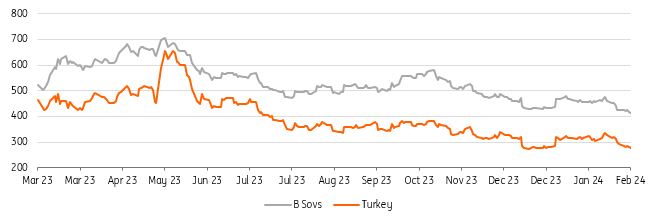

Sovereign credit: Some investor nervousness returns

With inflation coming in hotter than expected and the gradual depreciation of the lira continuing, policymakers' commitment to their shift to orthodox monetary policy will be tested in the coming months. The decline in FX reserves seen year-to-date has likely brought some nervousness back for sovereign credit investors ahead of local elections at the end of March, with external vulnerabilities continuing to show. In this context, Turkey's dollar bonds lagged the rally seen in most higher-beta names in February, and have sold off somewhat in the past couple of weeks. This leaves valuations somewhat cheaper than their recent history relative to both single-B and BB-rated peers, but investors will likely wait for election risk to subside and more concrete signs of adjustment in the economy before becoming more optimistic on the credit.

ICE US$ Bond Sub-Index Spreads vs USTs

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article