Monitoring Turkey: Inflation set to persist in the near term

In its final inflation report of the year, the Central Bank of Turkey repeated that inflation will start to decline in the second half of next year with the support of higher demand for TRY-denominated assets, the anchoring of inflation expectations and normalising domestic demand

Turkey: At a glance

- The Central Bank of Turkey (CBT) raised its year-end and 2024 inflation forecasts by 7ppt to 65% and by 3ppt to 36% respectively, while the uncertainty band around the forecasts widened on the back of higher geopolitical risks and uncertainties surrounding administered prices. However, the bank reiterated that the timing, pace and the course of disinflation all remain unchanged.

- The CBT’s 2023 inflation forecast is now closer to the consensus, while the upward revision in next year's forecast is attributable to higher TRY-denominated import prices and administered prices – including energy – despite downward revisions to food prices and the output gap.

- Thanks to progress in monetary tightening, with high enough rates to control lending and support de-dollarisation, the CBT has i) further simplified rate caps on loans ii) eliminated security maintenance requirements on TRY cash loans and securities issued by the real sector and purchased by banks, and ii) exempted imports of investment goods from the net exporter requirement with the objective of providing companies access to export loans.

- Renewal of FX-protected deposit accounts and conversion to TRY deposits to facilitate de-dollarisation (by increasing the share of TRY accounts) are no longer subject to security maintenance. Instead, commissions on reserve requirements for FX deposits are to be utilised for this purpose.

- Finally, to mop up liquidity in the banking system, the bank made further adjustments in required reserves. The total liquidity withdrawal with reserve requirement hikes since June amounts to TRY 1 trillion.

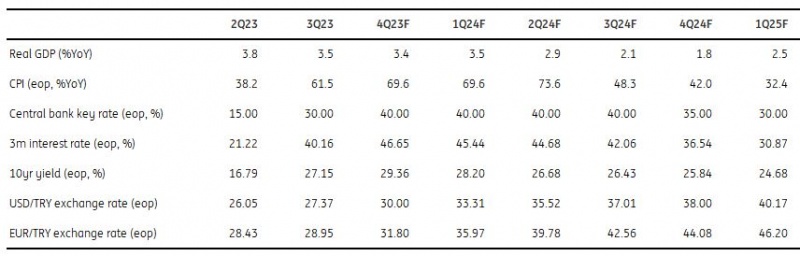

Quarterly forecasts

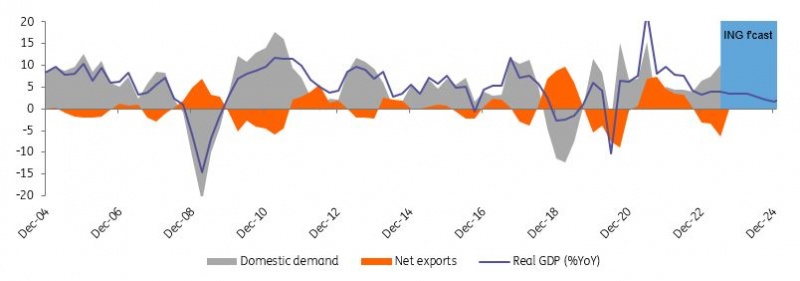

Recent growth indicators confirm slowdown in activity

The contraction in August industrial production and the plunge in retail sales in the same month imply that, following the large diversion in both indicators since the second half of 2022 that has contributed to growing macro imbalances until recently, we are likely to see the start of a reversal in this trend. This can be attributed to the impact of an ongoing deceleration in consumer loan growth as higher lending rates and the caps on volume expansion likely started to weigh on domestic demand.

We expect this loss of momentum to continue over the coming period given tighter financial conditions which are supportive of normalising household consumption. Meanwhile, weak external demand is persisting as a result of a more sluggish growth outlook for the eurozone, Turkey’s key export market. A soft landing scenario currently prevails as a result of the gradual tightening of monetary policy through the CBT's long rate hike cycle from June, as well as the slower simplification process in the macroprudential framework and supportive fiscal policy.

Real GDP (%YoY) and contributions (ppt)

Another monthly contraction in IP

IP in August recorded a 3.08% year-on-year increase on a calendar-adjusted basis, while in seasonally adjusted terms, it contracted by a 0.81% month-on-month following a mild 0.35% MoM drop a month ago. The data signals a loss of momentum in the third quarter with a limited 0.5% increase over the previous quarter, decelerating from 2.1% quarter-on-quarter in the second quarter.

While manufacturing production dropped on a sequential basis, mining, electricity and gas turned positive, supporting the industry sector's performance. In the breakdown, intermediate and non-durable consumer goods dragged the headline most with a -0.5ppt contribution each, while durable consumer goods provided another -0.1ppt drop. On the flipside, energy recorded 2.4% MoM growth and – by lifting monthly industrial production by 0.3ppt – limited the drop. Among sectors, volatility within transport equipment (dominated by defence industry products) added 0.7ppt to the headline, while motor vehicles and textiles both proved a major drag with -0.5ppt and -0.4ppt respectively.

IP vs PMI

Weakening signals in retail sales

Retail sales volume on a calendar-adjusted basis increased by 17.2% YoY, which was the lowest monthly reading in 2023, while the seasonally and calendar-adjusted index showed a sharp 4.7% MoM drop. The first contraction since February, marked by the impact of the earthquake, signals a moderation on the demand side.

Among sub-groups, non-food (excluding automotive fuel) and fuel sales contracted by 5.6% MoM and 9.0% MoM respectively, while the food group mildly increased by 0.1% MoM. The highest sequential fall in non-food sales was observed in the electrical household appliances and furniture group with 17.2% MoM. On the other hand, the (seasonally adjusted) unemployment rate inched down to 9.2% in August – the lowest rate since January 2014 – from 9.4% a month ago. While male unemployment is close to the lowest point in the current series (which started in January 2015 at 7.5%) the increase in female job generation has been comparatively limited in the recent period. Here, unemployment is at 12.6% vs the series low of 7.8%.

Retail sales vs consumer confidence

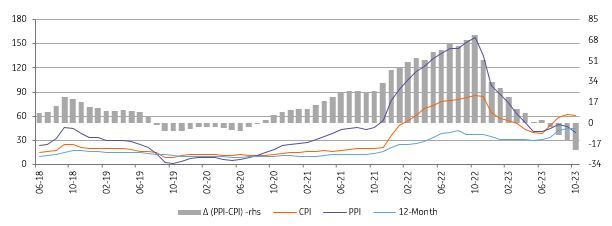

Annual inflation flat in October

With better-than-expected monthly inflation at 3.4%, the annual figure has remained broadly unchanged at 61.4% in October. The data reflects a continuing deterioration in price dynamics with significant pressure in both services and clothing – although the deceleration in food and transportation limited the monthly inflation increase. Core inflation (CPI-C) came in at 3.7% MoM, rising to 69.8% on an annual basis on the back of worsening pricing behaviour and inertia in services prices. However, the underlying trend for not only the core but also the headline rate improved in October, in line with the CBT's expectations as specified in its MPC note. Given that the central bank also pledged that the policy rate would be determined in a way that creates the monetary and financial conditions necessary to ensure a decline in the underlying trend of inflation, we should not rule out the possibility of deceleration in the pace of hikes in the upcoming MPC.

Inflation outlook (%)

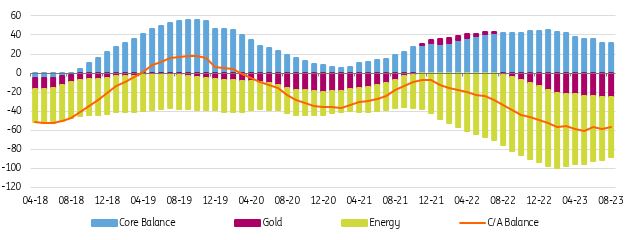

Current account likely initiated a recovery trend

The current account posted another deficit in August at US$0.6 billion, in line with consensus. The 12M rolling deficit narrowed to US$57 billion (which translates to around 5.7% of GDP) from US$59.1 billion a month ago. Early indicators for September hint that we will likely see further improvement that should continue in the last quarter of this year. A quick glance at the data points to the fact that a lower goods balance on the back of declining energy bills is the key reason for the drop in the annual deficit, given that services income remained broadly unchanged in comparison to the same month of last year.

The capital account, on the other hand, witnessed net identified inflows at US$1.2 billion. Net errors and omissions stood at US$4.46 billion (and reached US$16.3 billion in the three months following the elections, more than offsetting the outflows in the three months beforehand). With the monthly current account deficit and large inflows via net errors and omissions, official reserves recorded a US$5.1bn increase. However, given the weakness seen in the flows, the resulting depletion was significant in the first eight months of this year, with US$18.6 billion.

Current account (12M rolling, US$bn)

Likely acceleration in spending in the last quarter

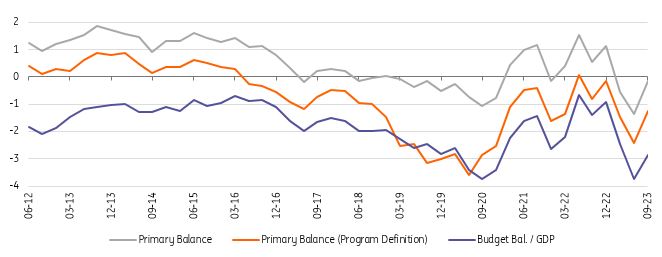

September's budget results reflected a worsening in the budget deficit in comparison to the same month of last year on the back of high non-interest expenditures driven by the acceleration in transfers to SEEs, despite the continued strength of increases in direct and indirect tax collections. Accordingly, the budget posted a deficit of TRT 129.2 billion, worsening from the TRY 78.6 billion deficit in the same month last year while widening to TRY 602.6 billion (2.7% of GDP) on a 12M rolling basis. In the new MTP, the budget deficit forecast for 2023 was revised to 6.4% of GDP. This suggests that a very large deficit of around TRY 1.1 trillion may be recorded in the last quarter of the year. The fiscal stance will remain accommodative in 2024 with another wide deficit at 6.4% of GDP, mainly due to continued earthquake-related spending. The issue here is that the fiscal outlook for next year suggests fiscal policy will not necessarily help the CBT with the disinflation process.

Budget performance (% of GDP)

The Treasury to keep domestic rollover rate high

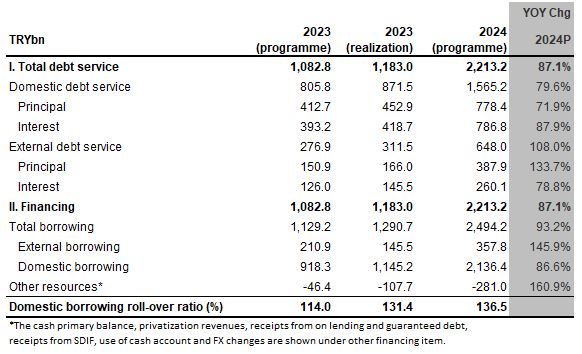

The Treasury announced developments in its 2023 financing program and projections for the next year. While expecting the domestic debt rollover at 131.4% – above that envisaged in the program for this year – it plans to keep the ratio around these levels at 136.5% in 2024. The rise in debt redemptions next year (by around 0.7ppt of GDP) stems from both domestic and external debt.

Out of TRY 1,565 billion domestic debt redemption in 2024, TRY 1,262 billion will be made via the market (with the remaining TRY 303 billion to public institutions via non-competitive sales). Assuming that domestic borrowing from public institutions is completely rolled over (the usual Treasury assumption, as it has to meet total demand from these institutions), TRY 1,833 billion of TRY 2136 billion domestic borrowing may be via the market – corresponding to a market rollover ratio of around 145.3%.

While the Treasury has issued US$7.5 billion in international capital markets this year so far, it plans to raise issuances to US$10 billion next year. As a result, the domestic borrowing requirement seems to be markedly high, which may be attributed to a supportive fiscal stance and adjustment in rates. The rate outlook, given the CBT’s ongoing policy tightening and continuing supportive fiscal stance, will be key for the Treasury’s programme.

According to the sensitivity analysis based on the 2022 stock, a change in the real exchange rate app/dep by 5ppt will lead to +/-0.9ppt on the EU-defined general government debt stock to GDP ratio. Meanwhile, a change in the TL interest rate by 500bp and a change in GDP growth rate by 2ppt will impact the same variable by +/- 0.6ppt and +/- 0.5ppt respectively.

Treasury’s financing programme

Central bank opts to continue on at the same pace

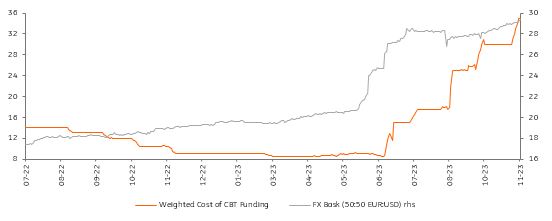

By opting for another 500bp hike at its October rate-setting meeting, the Central Bank of Turkey has pulled the policy rate to 35% and repeated its signal for further tightening steps in rates and macroprudential instruments to achieve disinflation. According to the bank, the persistence of upward pressures, risks to the inflation outlook and the alignment of the disinflation course with the forecast path in 2024 were the major driving factors.

In a note explaining the rate decision, the bank reiterated that it will continue with monetary tightening steps in a "timely and gradual manner" until it achieves a significant improvement in the inflation outlook. In this regard, the CBT acknowledged that the pass-through from the post-election adjustment in FX, wages and taxes has been “largely completed”. It pointed again to strong domestic demand, stickiness in services prices and a jump in inflation expectations as the key factors putting upward pressure on the inflation outlook, while also mentioning the upside risk to oil prices due to geopolitical developments. Finally, to support its monetary policy stance, it pledged the continuation of quantitative and selective credit tightening moving at a gradual pace.

CBT funding rate (%) vs FX basket

FX and rates outlook

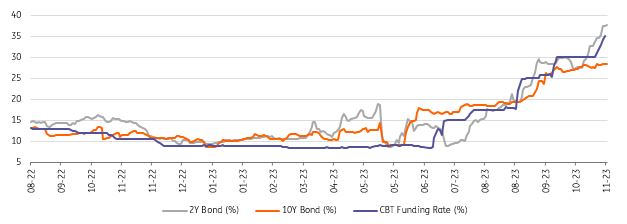

Despite some economists' expectations and market pricing of a slowdown in rate hikes, the CBT delivered another 500bp in October and maintained its commitment to monetary policy normalisation. Accordingly, the carry to be short remains high. Fundamentals on the balance of payments side are expected to improve in the coming period, given that the policy-induced slowdown in the economy will lead to a correction in the trade deficit and therefore in the current account balance. On the financing side, an increase in capital inflows would support the soft-landing scenario, helping with reserves and the currency. Relatively higher external debt repayments in the last two months of the year will be under watch.

In line with its signal to take steps on quantitative and selective tightening to reinforce rate hikes, the CBT has come up with a set of new actions including broader adjustments to its security maintenance framework. The central bank has already cut auctions to buy bonds in the secondary market, which led to a marked drop in the share of government securities also attributable to an expansion in the balance sheet, with an inflating effect from the recent currency adjustment and upward pressure on yields – especially in the back-end. The regulatory impact on the bond pricing should further decline following the latest changes, with further support to the recent normalisation in yields. Higher inflation expectations and continuing upward adjustment in policy rate expectations also weigh on bond yields.

Local bond yields vs CBT funding rate

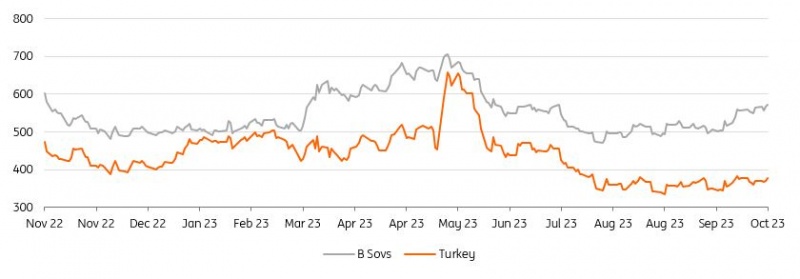

Sovereign credit spreads remain well anchored

Performance has been robust for Turkey's dollar bonds over the past month, with spreads mostly continuing to tighten relative to its ratings peers. 5Y CDS spreads briefly touched the lowest level since 2021, while cash bond spreads at the index level (as per the JP Morgan EMBI-GD index) have squeezed tighter than their early 2020 lows.

Sentiment has continued to improve for Turkey, with more investors starting to believe in the durability of the shift to more orthodox monetary policy, while limited supply from the sovereign (before this week at least) has also been a technical tailwind. As a negative factor, current spread levels already imply investors pricing in a one or two-notch rating upgrade across the board, while headline risks remain around next year's local election and ongoing developments in the Middle East, as well as with plans for significant external bond issuance next year. However, with Turkey's conventional Eurobonds rallying, the nation's Islamic sukuk curve now offers an interesting pickup over the conventional curve, in part due to the recent announcement of new supply. Both the outstanding sukuk securities and this week's new issue could offer more downside protection in the event of a broader market selloff, due to their generally more stable investor base.

ICE US$ Bond Sub-Index Spreads vs USTs

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article