Monitoring Turkey: Easing bias remains intact

While acknowledging the strengthening domestic demand in the fourth quarter and the recent acceleration in loan growth despite being at disinflationary levels, the Central Bank of Turkey (CBT) delivered a third 250bp cut earlier this month, highlighting the decline in the underlying inflation trend in February

Turkey's economy at a glance

- Economic data for the fourth quarter of 2024 shows domestic demand recovering despite tight monetary policies. Private consumption reached a record high after declines in mid-2024, while net exports made a negative contribution to growth. Indicators suggest GDP growth will continue to recover in early 2025, though the central bank considers demand conditions to support lower inflation. If demand grows faster than expected, the bank may introduce new measures or slow interest rate cuts.

- February inflation was lower than expected, contributed by both food and non-food items, following a sharp rise in January. The Finance Ministry reversed the increase in hospital copayments, which contributed to last month's better inflation figure. While strong domestic demand has led producers to pass on higher costs to consumers, inflation is expected to continue declining as the central bank maintains tight policies, currency strengthens, and service inflation improves.

- Inflation is likely to fall further in March, allowing for a potential 250bp interest rate cut in April, in our view. Future central bank decisions will depend on factors like foreign currency deposits, exchange rates, and foreign reserve levels. In February, the Central Bank shifted from buying to selling foreign currency due to increased local demand. Sustained pressure on the currency may lead to stricter policies, smaller rate cuts, or a pause.

- The central bank is taking a flexible approach, deciding on interest rates at each meeting and signaling further cuts as inflation declines. We expect inflation to be at 27%, with a policy rate of 29% by the end of 2025, though risks remain on the upside.

- Despite stricter loan growth limits introduced in January, bank lending has accelerated, especially in foreign currency loans. To slow this trend, the central bank reduced the FX lending growth cap further and narrowed exemptions for this type of loan.

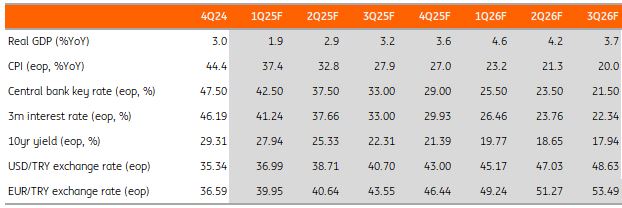

Quarterly forecasts

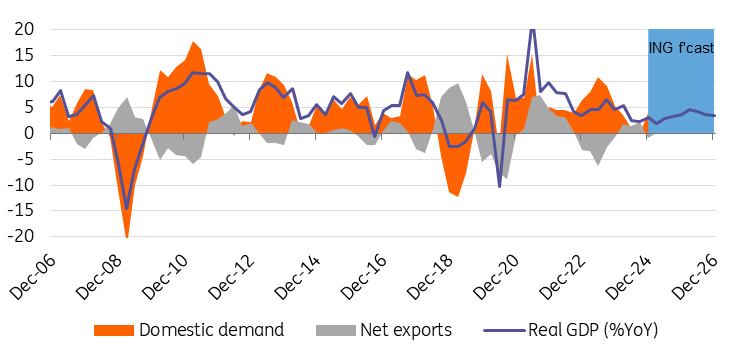

GDP beats expectations on strengthening domestic demand

In the fourth quarter of 2024, Turkey's GDP growth turned out to be 3.0% YoY, surpassing the market consensus of 2.6%. This improvement was driven by a rebound in private consumption and robust investments. For all of 2024, GDP growth was 3.2% YoY, decelerating to its lowest level since 2020 due to weak performance in the second and third quarters.

Fourth-quarter GDP translates into a QoQ growth rate of 1.7% after seasonal adjustments, showing a strong momentum gain and marking the highest quarterly reading since the second quarter of 2023. The accelerating sequential performance is attributed to the turnaround in household consumption, which turned positive after a negative reading in the previous quarter and accelerating investments despite negative contributions from inventory build-up and net exports. The data implies that Turkey, which was in a technical recession as of 3Q 2024 with two sequential contractions, returned to positive quarterly GDP growth in the fourth quarter of 2024.

Real GDP (%YoY) and contributions (ppt)

PMIs remain weak in February

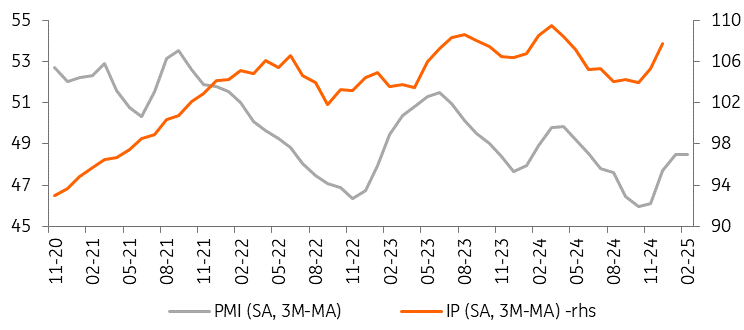

The manufacturing PMI index has remained in contraction, showing a continuation of challenging business conditions, though its average in the first two months of this year at 48.2 turned out slightly above the level realised in 4Q24 at 47.7. In the breakdown, sluggish demand, as observed by slower new orders, contributed to weakness in output and employment. As an additional note, rates of both input cost and output price inflation recorded an acceleration compared to a month ago.

The sectoral PMIs released by the Istanbul Chamber of Industry align with the manufacturing PMI data, indicating widespread declines in production and new orders due to ongoing demand challenges and persistent inflationary pressures. Out of 10 sectors, only food has a PMI above the 50 threshold, suggesting continued weakness in economic activity.

IP vs PMI

Headline unemployment rate remains low

According to seasonally adjusted results, despite a decline in employment in January, the labour force participation rate also dropped. As a result, the headline unemployment rate decreased slightly to 8.4%. Historically, the lowest unemployment rate was 8.0% in July 2012, while the highest was 14.1% in September 2019. In the first month of this year, the employment rate fell to 49.2%, while the labour force participation rate stood at 53.7%.

On the other hand, the seasonally adjusted average weekly actual working hours increased by 0.8 compared to the previous month, reaching 43.4 hours in January. One of the broader unemployment indicators, the underutilisation rate – which combines time-related underemployment, potential labour force, and the unemployed – increased by 0.1ppt over the previous month to 28.1%. This rate, which reached a historical peak of 30.2% in January 2021, fluctuated within the 20-25% range in subsequent years but recently showed an upward trend.

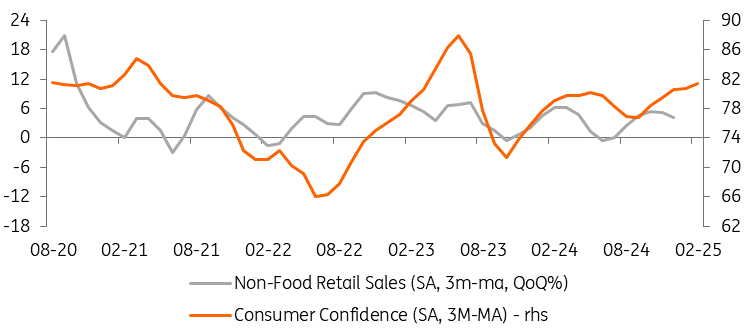

Retail sales vs consumer confidence

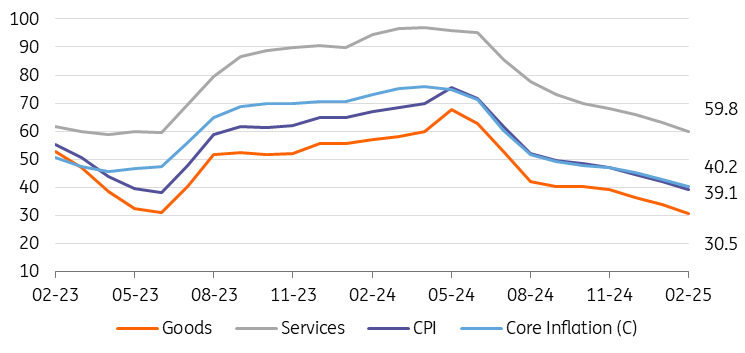

Benign inflation led by food and health costs

In February 2025, monthly inflation stood at 2.3% MoM, coming in below the consensus of 2.9% and our forecast of 3.0%. As a result, annual inflation continued its downtrend, falling to 39.1% YoY from 42.1% a month earlier, though it remained well above the Central Bank of Turkey's forecast of 24%.

While there was an increase of 4.5% in February 2024, the average of February months of the 2003-based index for the last 10 years was 1.6%, indicating that the base effect was favourable for this year. Core inflation (CPI-C) came in at 1.8% MoM, moving down to 40.2% on an annual basis, supported by the relatively slow-moving FX basket (despite an acceleration in February to 2% MoM) and benign PPI outlook.

Going forward, pricing behaviour and inertia in services have remained key risk factors for the pace of the current disinflation process. An analysis of seasonally adjusted figures reveals that the underlying trend, which CBT monitors closely, seems to have improved significantly after a jump in January.

Inflation outlook (YoY%)

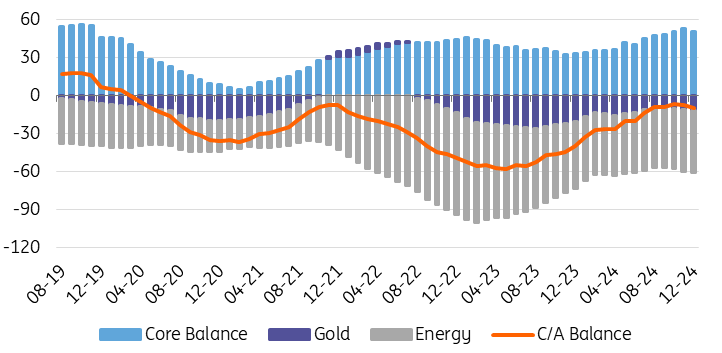

Significant improvement in the current account balance last year

In December, the current account posted a deficit of $4.7bn, exceeding the market consensus of $4.0bn. The monthly data breakdown reveals that the widening trade deficit – driven by energy, gold, and core (excluding gold and energy) – and a sharp deterioration in primary income were the major factors.

The 12-month rolling current account balance, however, stood at $10bn (approximately 0.7% of GDP) at the end of 2024, compared to a deficit of $39.9bn in 2023. The capital account saw inflows of $3.0bn, albeit lower than the current account deficit.

With almost flat net errors and omissions, official reserves contracted by $1.6bn in December. Monthly data breakdown shows residents' movements led to $5.3bn outflows through outward FDI, portfolio investments, increased deposits abroad, and extended credits. Non-resident flows, on the other hand, amounted to $8.4bn, mainly driven by debt-creating flows.

Current account (12M rolling, US$bn)

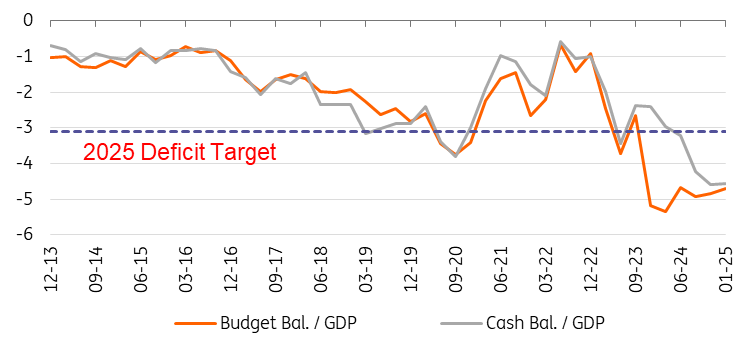

Narrowing budget deficit in January

According to January's budget results, the slowdown in non-interest expenditures brought a slight improvement in the budget balance compared to the same period last year. In January, tax revenue growth slowed to 53.3% year-on-year. While corporate tax revenues declined, the growth rate of VAT and SCT revenues also slowed.

At the same time, the growth rate of non-interest expenditures eased to 38.1%. This deceleration was mainly driven by a slowdown in healthcare, retirement, and social welfare spending, with their growth rate dropping to 34.2%. Similarly, the growth in current transfers and personnel expenses also lost momentum.

As a result of these developments, tax revenues saw real growth on an annual basis, while both interest and non-interest expenditures declined in real terms. Accordingly, the ratio of the last 12 months' budget deficit to GDP decreased to 4.6%. Meanwhile, the primary balance recorded a deficit of 1.7%.

Budget performance

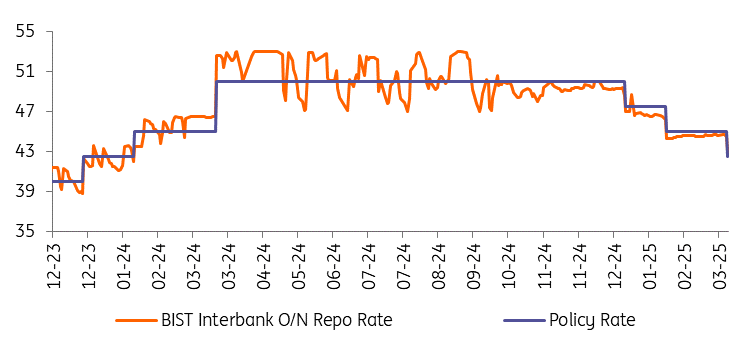

CBT cut by 250bp in March, signals more to come

The Central Bank of Turkey (CBT) continued its rate-cutting cycle in March, following the easing trend it initiated in December. In its March meeting, the CBT reduced the policy rate by 250bp, bringing it to 42.5% as expected. Alongside its decision, the CBT noted that core goods inflation remained relatively low, services inflation showed signs of slowing, and there was a general decline in inflationary trends.

The CBT still sees current domestic demand conditions as disinflationary. Should domestic demand recover more quickly, the bank may implement additional macroprudential measures or slow the pace of rate cuts.

After the meeting, the policy rate adjusted for current inflation now stands at 3.4ppt. Based on market participants' inflation expectations, the real policy rate is 17.2ppt, compared to 0.6ppt using firms’ forecasts. Despite recent progress, the CBT reiterated that inflation expectations and pricing behaviour continue to pose risks to the disinflation process.

The Policy Rate vs. Interbank O/N Rate

FX and rates outlook

The Turkish lira (TRY) seems unconcerned with the start of the CBT cutting cycle despite three 250bps rate cuts since last December. Our baseline remains that the lira will continue to appreciate in real terms, however the trend sees some cracks with shrinking carry and harder to beat forwards. Despite this, we believe the Turkish lira remains the most favourable carry trade in the emerging market space for now, and it's too soon to alter this perspective.

Despite heavy long positioning on the foreign investor side, the main risk to TRY is actually the local market and its demand for FX. Yet, February's central bank data showed some shift from buying to selling FX due to increased local demand. For now, this can be seen as more of a market normalisation, however, if the pressure continues, we could see a more cautious approach from the central bank, which we believe is risk aware of the sudden outflow of domestic holders from TRY into FX, threatening the market stability of the local currency. Overall, as a baseline, we expect a continued USD/TRY uptrend in the coming months with 38.71 mid-year and 43.00 year-end.

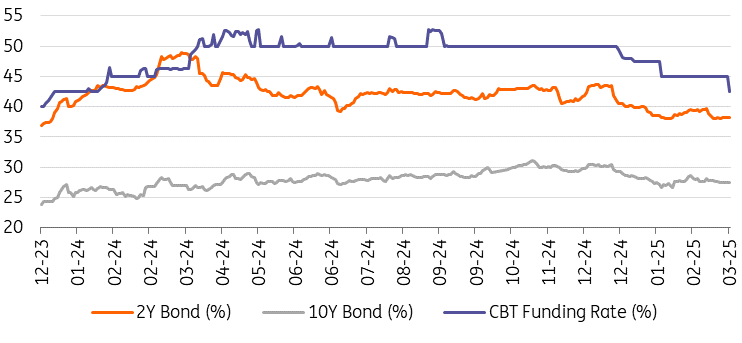

Rates in the OIS curve are currently trending downward, reaching new lows. We believe market expectations for this year are more or less fair vs our forecast and we see more room for a decline in next year's pricing where the market remains more on the hawkish side vs our expectations. Overall, we should see a further steepening of the OIS curve.

In the TURKGB's space, MinFin covered roughly 18% of this year's supply with mute activity in February, according to our estimates. However, March should bring several auctions in the coming days, especially in the belly curve, while the long-end supply remains light. February's lower-than-expected inflation brought a short-lived rally and yields have stabilised after the February sell-off well above January lows. We still believe bond valuations remain attractive, especially when we look at the 2y-5y part of the curve in the context of our inflation profile for next year and current direction. Foreign holdings have jumped back above 10% after some downside in December and visible interest in TURKGBs is gradually increasing, but still, foreign demand is mainly directed to the short end of the curve, betting on an imminent rate cut story.

Local bond yields vs CBT funding rate

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article