Mexico’s prolonged stagnation

Low inflation and evidence that the prolonged economic stagnation shows no sign of abating should prompt the central bank to commit to a gradual easing cycle this week. The slow pace of rate cuts should keep the Mexican peso well-supported in the near term, but unexpected episodes of excessive FX weakness could bring the easing cycle to a temporary halt

Banxico appears finally resolved to fly solo

This week’s monetary policy meeting in Mexico, on Thursday, should mark the moment in which Mexico’s central bank (Banxico) decided to decouple its monetary policy decisions from the US Fed. In practice, this suggests that, Banxico is likely to cut its policy rate, at gradual 25bp increments, in each of its upcoming policy meetings. This Thursday’s meeting should bring the policy rate to 7.25%, down from 7.5% currently.

For about two and half years, Banxico has been closely following the US Fed, in an effort to keep the US/Mexico rate differential intact, in support of the Mexican peso. The strategy has worked well for the MXN, which has had a stellar performance in recent quarters.

But the strategy has become too hard to justify now, with GDP growth stuck near zero and inflation on target. As it stands, the current monetary policy stance in Mexico, with its overnight rate at 4% in real terms, appears excessively restrictive, when compared to its regional peers (see chart below).

As a result, contrary to the other central banks in the region, where we expect no significant monetary policy shifts in the coming quarters, Mexico stands out for having much to do in terms of monetary easing in the coming years.

Having said that, Banxico does not appear to be in a rush to stimulate the economy through monetary policy and the risk of more aggressive 50bp cuts remains small, as a majority in the bank's board should prefer not to surprise the market on the dovish side.

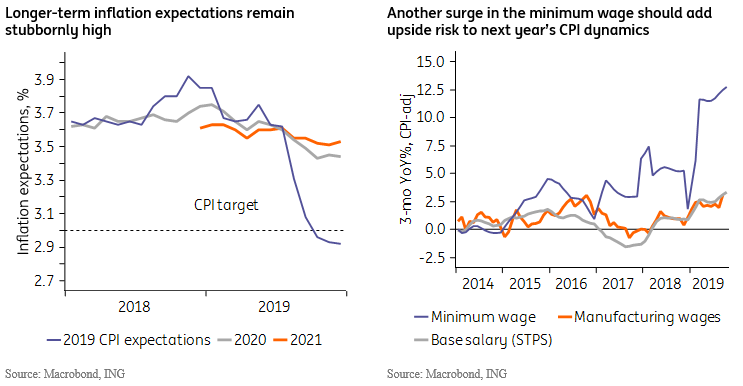

Bank officials continue to worry about high core inflation, higher-than-target inflation expectations (see chart) and, increasingly, the upside risk represented by fast-rising wages (see chart).

The Lopez Obrador (AMLO) administration announced this week that, despite the misgivings voiced by some central bank officials, the minimum wage will be increased by 20% in January, after surging by 16% in 2019. The risk is that such a large wage gain, which officials seem to view as a central pro-growth measure, contaminates other wage negotiations that will take place in 2020 and further weakens Mexico’s productivity metrics.

Banxico’s reaction-function should also continue to be marked by a certain reluctance to cut rates for fear that this could weaken the currency. In fact, should the currency weaken sharply in reaction to events such as a spike in global risk aversion, or local market disruptions caused by credit rating downgrades or controversial policy decisions, Banxico could temporarily pause the cycle.

In any case, the cautious guidance and the measured pace of the cycle, i.e. 25bp, suggests that monetary policy decisions should continue to provide support for the MXN in the nearer term.

How will AMLO react to signs of persistent recession?

Having started his administration with high hopes for launching a fast growth trajectory, the Lopez Obrador administration is probably frustrated with the paltry results seen throughout the past year.

The sense of frustration should have intensified with the latest round of activity data, which displayed broad-based weakness in production data, notably construction and the auto industry. They suggested that the weak momentum extended into 4Q. Retail sales data was a bit firmer, probably reflecting the faster increase in wages that’s helping offset the gradual rise in unemployment seen lately. Overall, however, we’ve updated our GDP growth forecast down about 20bp to -0.1% in 2019 and 0.9% in 2020.

This should represent a wake-up call for the President, especially considering that, given the relatively strong performance of its primary trading partner, the US, this outcome is largely a result of domestic policy implementation issues.

This situation suggests that AMLO’s policymaking should undergo a higher degree of reassessment going forward. And, in our view, any policy changes taken at this juncture should be seen as particularly telling about Mexico’s long-term outlook.

In economic policy terms, the administration could implement changes to monetary and fiscal policies. Monetary policy is conducted independently by the central bank and, as discussed above, the gradual pace of cuts suggests that Banxico’s monetary policy stance should remain restrictive throughout 2020.

AMLO also often emphasizes an intention to uphold Banxico’s independence, but the President will have the opportunity to appoint a majority of the bank’s board at the end of 2020. And, judging by the more dovish stance advocated by the two bank directors that he has appointed so far, a bigger reorientation of monetary policy directives could indeed take place, but only in 2021, potentially exacerbating concern over central bank credibility.

In terms of fiscal policy, limited resources suggest that any effort to boost growth through fiscal stimulus would erode Mexico’s fiscal stance, especially in the context of weak growth/tax collection.

These policy constraints help explain the broad-based scepticism evident in business sentiment surveys and help illustrate how difficult it will be for AMLO to stimulate economic activity without renouncing his signature predilection for a big state presence in the economy, notably evident in the restriction of private sector participation in the energy sector.

Brazil’s left-leaning experiment under Dilma Rousseff represents an extreme version of what could go wrong, as seen in the dramatic deterioration of both monetary and fiscal credibility that took place in Brazil in the Rousseff years.

So far, AMLO has not been inclined to jeopardize policy credibility by following on Rousseff’s footsteps. Instead, if current policy directives stay in place, the base case scenario should continue to depict a scenario of low investment and below-potential GDP growth. Such a scenario would gradually strain the government’s fiscal capacity and increase risk premium incorporated into financial assets, gradually reducing the scope for policy stimulus.

This contrasts with the (less likely) optimistic scenario in which the administration is successful in its effort to boost private investment through its National Infrastructure Plan, to be unveiled early next year, in addition to helping revive the construction sector, in part by overcoming the logistical difficulties to implement regulations, and surprising sceptics by achieving its ambitious oil production targets.

Unlike many, we are also less optimistic about the boost that the eventual approval of the USMCA trade agreement should provide to Mexico’s growth dynamics. In particular, we worry that US tariff policies have become so capricious that trade agreements are no longer sufficient to ensure the needed growth-inducing stability to external trading rules.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article