Mexico’s cautious policy stimulus

Mexico’s central bank should extend the monetary easing this week, with another 50bp cut, and, given the recent rise in inflation, adopt a cautious guidance. Even though Mexico’s policy stance is far tighter than that of its regional peers, Banxico should interrupt its easing cycle soon, possibly after one last 50bp cut, to 4.0%, in its September meeting

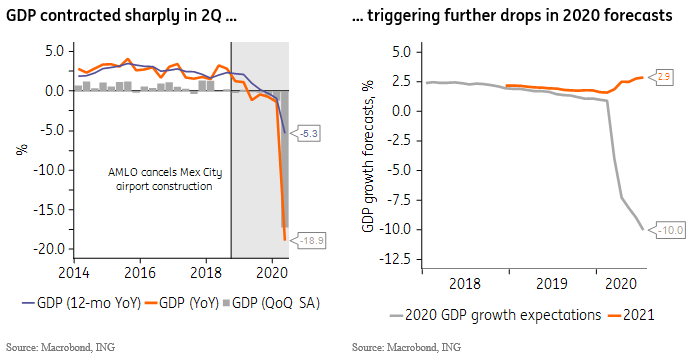

GDP growth expectations turn grimmer

The preliminary 2Q GDP print registered a large 19% YoY contraction, helping trigger another round of revisions in 2020 growth expectations. At -10%, Mexico’s 2020 GDP growth consensus estimate is among the worst in LATAM, even though public records show that the country’s Covid-19 outbreak has been somewhat milder than seen elsewhere in the region.

Poor growth expectations are consistent with the government’s decision to enact an unusually modest countercyclical policy stimulus package, in reaction to the pandemic.

Mexico’s small fiscal stimulus program, at close to 1% of GDP, was substantially smaller than the programs announced by its regional peers and has done little to replace income lost due to the pandemic. This has increased the risk of permanent damage to vulnerable sectors of the economy, and added a more persistent downside bias to economic activity.

Nearing the end of the rate-cutting cycle

Monetary policy decisions have also stood out for their more deliberate pace and a relatively less dovish stance. Despite the dire outlook for economic activity and the rising output gap, central bank officials have refrained from replicating the aggressive rate-cutting cycle seen throughout LATAM.

Tomorrow’s monetary policy meeting should conclude with policymakers, once again, reducing the policy rate by 50bp, to 4.5%. There’s a widespread consensus among analysts about the meeting’s outcome but, with the bank now getting closer to interrupting the cycle, there’s now greater uncertainty about how clearly officials should communicate their appetite for additional cuts.

Headline inflation is still comfortably within the targeted range, at 3.6% year-on-year, but the fact that recent inflation prints have often surprised to the upside should help justify a more cautious monetary policy guidance this week.

Inflation expectations have also risen towards the upper-bound of the targeted range, which could warrant caution, but weak demand suggests that recent price pressures, seen in a relatively narrow segment of the consumer basket, are unlikely to turn into a persistent problem, and probably reflect pandemic-related supply constraints.

Ultimately, however, Banxico’s enduring concerns regarding the impact of rate cuts over local market financial stability, which could be compromised if capital outflows surge, suggest that tolerance for additional cuts is likely nearing a limit.

Monitoring investor outflows

As seen in the charts below, non-residents have already repatriated significant amounts of resources previously allocated to local government bonds. In fact, the current 22.5% share of non-resident holdings of local debt is the lowest in almost a decade.

As the chart below also suggests, those flows have, in the past, broadly coincided with shifts the Mexico/US interest rate differential, and Banxico often cites that rate differential as an important consideration in its reaction function.

Assuming a terminal rate of 4% for the current cycle, that differential would drop 200bp below the level prevailing in the recent 2017-20 period, which was marked but broad stability in non-resident holdings.

That differential is also 50bp below the level that prevailed in the long 2009-13 period that was marked by the initial surge in non-resident public debt holdings in Mexico, from a very low base, but it is still 100bp higher than the level seen in 2014-16 that coincided with a first wave of outflows.

Overall, the perception that rate cuts could exacerbate outflows and compromise local market stability suggests that central bank officials are likely to sound increasingly concerned about their ability to stimulate the economy through rate cuts. Our view is that Banxico should follow the path of least-resistance here, and deliver a result as close to consensus as possible, to avoid market surprises.

We expect one last 50bp rate cut in September to 4.0%

As a result, our expectation is that the bank follows this week’s cut with one last 50bp in September, to 4.0%. A more gradual decline, with two consecutive 25bp cuts, is also a possibility. Beyond that, we suspect that further cuts are likely to be considered only in 2021, after economic activity fails to recover at a satisfactory pace and after the current central bank board composition is altered, at the end of the year.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article