Mexico: Mixed signals for monetary policy

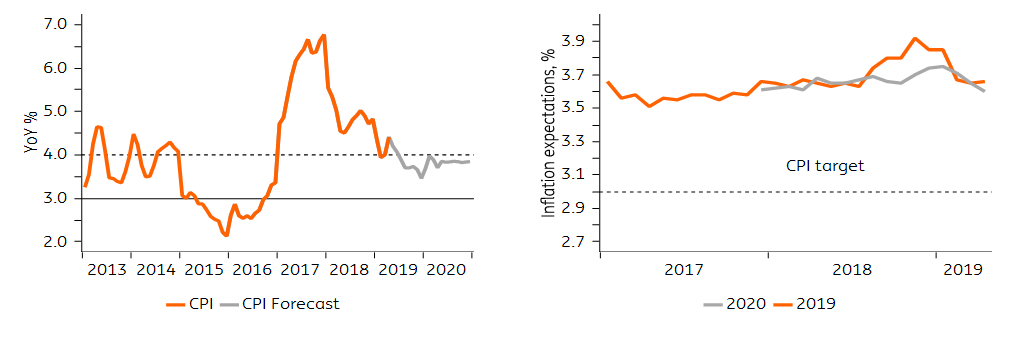

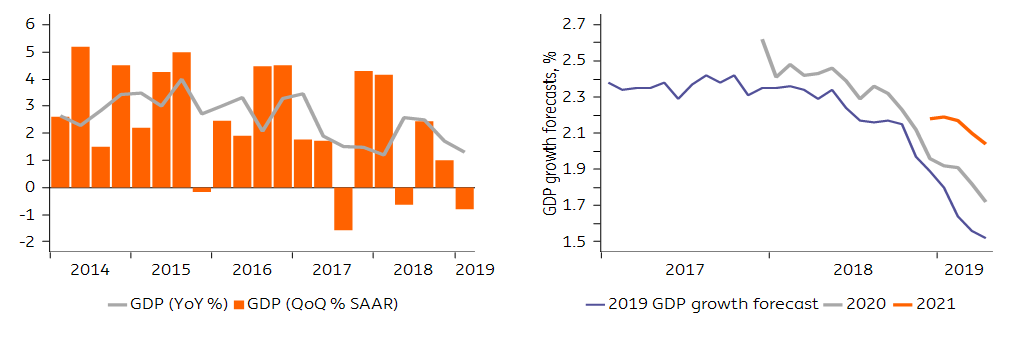

Economic activity data has disappointed sharply, with GDP printing a surprise contraction in 1Q. But the temporary spike in the inflation rate, to 4.4% YoY, should delay slightly the emergence of a more dovish consensus inside the central bank’s board. We still expect 3 rate cuts this year, with the policy rate ending the year at 7.5%

Temporary spike in inflation adds uncertainty to near-term rate outlook

Economic data released in recent weeks suggest that this week’s monetary policy meeting, on Thursday, should provide little additional definition about the near-term path for the policy rate.

A firmer definition could have been expected after the revelation, in the minutes of the latest meeting, that one board member (Gerardo Esquivel) opted to write a dovish dissenting opinion regarding the official characterization of the inflation outlook.

The emergence of a clearer split in the board, towards a more dovish consensus, could have gained momentum following the surprise contraction in GDP seen in 1Q, released 2 weeks ago, which displayed broad-based weakness across the industrial and service sectors. But the recent deterioration in near-term inflation dynamics, together with the ongoing spike in risk aversion, suggest that a more cautious policy consensus should prevail this week, once again.

As a result, we expect Banxico to keep the policy rate stable at 8.25% and do not alter materially the slightly hawkish/neutral policy guidance that has prevailed in recent meetings.

A temporary spike in inflation

The rise in inflation is broadly expected to be short-lived, resulting from the strong seasonality in Mexico’s CPI, notably on travel-related activities, to the calendar shift in the Easter holiday this year, versus 2018.

The yearly inflation rate should return to a declining path starting next month, and re-enter the targeted range at the end of July or August. But the current high print, at 4.4% YoY, ie, far above the 2-4% targeted range, should increase policymakers’ resistance to implement, already at this meeting, a firm dovish shift in the policy guidance.

Growth headwinds should prove more persistent than inflation worries

Our fundamental assessment that Mexico’s monetary policy should be eased in the coming quarters has not changed. But the higher-than-expected inflation suggests that Banxico is less likely to signal a willingness to cut the policy rate at its following meeting, on June 27. As a result, the August 15 meeting is now the earliest opportunity, in our view, for a rate cut this year.

In our base-case scenario, Banxico will implement 3 rate cuts this year, bringing the policy rate to 7.5% by year-end, and to 6.5% by the end of 2020.

The return of the yearly inflation rate to the targeted range, along with the perceived dovish shift in the US Fed’s monetary policy outlook seen in recent months, should help pave the way for the cuts. But, we suspect, the significant slowdown in economic activity, which intensified in 1Q after an already weak 4Q18, should become the primary motivating factor for Banxico to opt to reduce the contractionary impulse implied by its current monetary stance.

In its 4Q18 Quarterly Report released at the end of February, Banxico announced a sharp drop in the bank’s forecast for GDP growth. The bank’s 2019 GDP growth forecast dropped 0.6ppt, and is now centered at 1.6%. The 1Q19 report, to be published at the end of this month, should lower further those projections, possibly towards our own 1.3% forecast for 2019.

Recessionary momentum building as GDP consensus forecasts fall sharply

At 8.25%, the policy rate remains quite restrictive and far above neutral, which is closer to 6% than 7%. As a result, the case for some monetary easing should become increasingly persuasive in light of the widening output gap and the incipient deterioration in labor indicators, and it should strengthen especially as inflation is firmly consolidated inside the targeted range in the coming months.

The two biggest risks to our call are 1) higher-than-expected inflation and 2) a sharp determination of the global risk environment, triggered for instance by the escalation of trade-war concerns, that results in a sustained sell-off in the MXN.

FX has, traditionally, played a crucial role in Banxico’s reaction function and such an event could tip the balance in favour of a delay in rate cuts.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article