Mexico: It’s too soon for a dovish shift at Banxico

This week’s monetary policy meeting will be the first with the two newly-appointed board members. Investors would like to see signs of policy continuity, while any significant dovish departure would be a risk to monitor. Attractive rates, a solid macro stance and a more dovish FOMC suggest, meanwhile, a benign near-term bias for local assets

Banxico has been a chief anchor of market stability

Mexico’s central bank (Banxico) has played a critical and ultimately successful role in the stabilization of Mexico’s local markets in recent years, when policymakers have faced several major shocks that resulted in sharp depreciation and heightened volatility in local assets.

These included the collapse in oil prices at the end of 2014, the election of Donald Trump in 2016, the NAFTA treaty renegotiation and, finally, the election of Lopez Obrador.

Banxico’s success, evident in the superior central bank credibility achieved through pro-active monetary policy decisions, is a critical legacy inherited by the Lopez Obrador administration. It is also, perhaps, the last remaining critical element of the policymaking apparatus that investors should monitor, to try to understand the extent to which policy preferences of the new administration will shape overall policy directives.

The first meeting of the new regime

Mexico’s monetary policy committee meets again this Thursday and there’s a broad consensus that bank officials will keep the policy rate stable, at 8.25%.

We also expect policy guidance to remain relatively hawkish, even if the board should display a much-reduced appetite for further rate hikes, effectively moving the policy guidance closer to a “neutral” bias.

Several considerations could justify a less hawkish bias to the bank’s policy guidance. Chief among them is the recent dovish surprise by the US FOMC, which, in practice, should be seen as a near-term improvement in the risk profile for the Mexican peso.

The second important dovish development seen in recent weeks is the growing evidence that economic activity is moderating. This is evident in several indicators including the weaker-than-expected GDP print for 4Q, declining industrial and investment activities, the surprising uptick in unemployment, and the loss in momentum in bank lending, notably business loans (see chart below).

Recent activity data added a downward bias to 2019’s GDP result

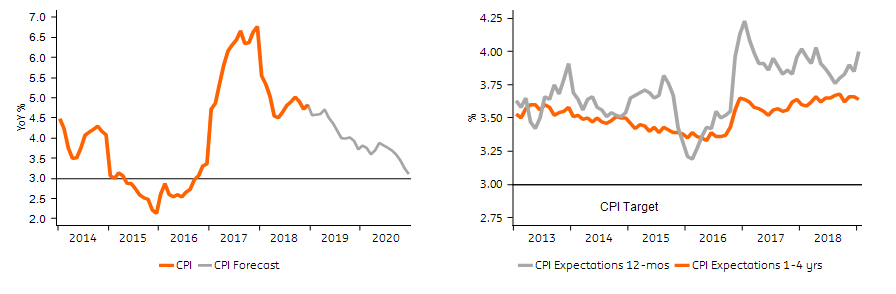

The yearly inflation rate continues to fall, thanks to favourable base-effects and decelerating energy prices, and we expect it to continue falling throughout 2020 (see chart below).

However, at 4.8% YoY (a new print will be published on Thursday, before the policy meeting), inflation remains high, and the pace of convergence towards the 3% target has been slower than expected, which has also contributed to keep inflation expectations meaningfully higher than the target (see chart).

Inflation dynamics remain too high for comfort

Lastly, Banxico’s five-member board makeup has changed with the addition of two Lopez Obrador appointees, Jonathan Heath and Gerardo Esquivel. Both will have their inaugural meeting this week.

In our view, given that monetary policy remains the most important anchor of stability for local financial markets, it would be important for Banxico to signal continuity, rather than a break from past policy preferences. In particular, we suspect that, at this stage, signs of dovish dissent could be damaging.

Rate cuts should be considered later in the year

Inflation will likely re-enter the targeted range at the end of the year, allowing Banxico to start considering rate cuts. It is too soon for Banxico to signal a material dovish shift, however. Given the large presence of non-resident portfolio holdings in the local market, Banxico should proceed with caution, in light of still-unsettled external and domestic uncertainties, and conduct policy with an eye on preventing sustained FX outflows.

Lopez Obrador has repeatedly stated his commitment to respect and uphold Banxico’s independence. However, the recent leftist experience in Brazil is illustrative, and we suspect investors will be closely monitoring the evolution of Banxico’s policymaking in the coming months, looking for signs of political interference.

Another crucial local development that investors will monitor is PEMEX. The large two-notch credit rating downgrade announced by Fitch last week, if followed through by other agencies, adds important downside risk for both financial markets and the economy at large and bears close monitoring.

Despite risks associated with central bank independence and lingering fiscal/PEMEX concerns, we believe that the Lopez Obrador administration is now settling into a more conservative policymaking stage, after having solidified some key controversial “political victories” in recent months.

In particular, the risk of rupture in market credibility in issues like fiscal prudence and central bank independence should take a bit longer to emerge. If Brazil’s recent experience is any indication, that risk would rise specially if economic activity disappoints, as pressure on the administration to find alternative means to boost economic growth would rise, increasing the risk of policy mistakes.

For now, however, the mix of attractive rates, solid macro fundamentals and the relatively benign external environment suggests that a “glass half-full” perspective is likely to prevail, adding a benign near-term bias for local assets.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article