Mexico: Another (small) emergency rate cut

Mexico’s central bank surprised with an emergency 50bp rate cut today, as expectations of a collapse in economic activity intensified, following a series of credit rating downgrades and a sharp deterioration in the outlook for the oil sector

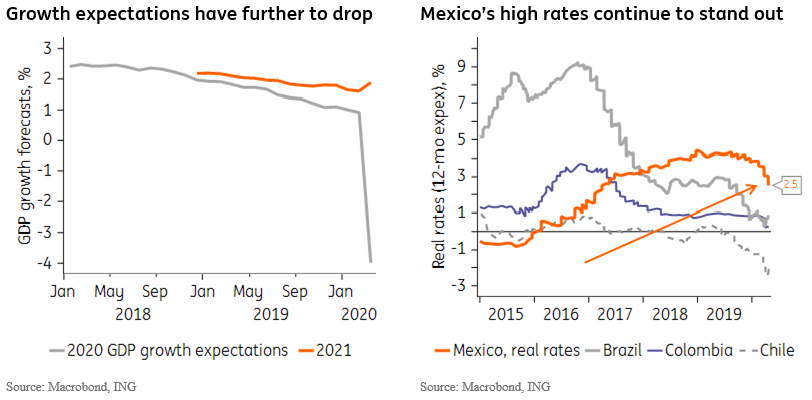

Monetary policy remains unusually restrictive in Mexico

Mexico’s central bank, for the second time in exactly one month, decided to reduce the policy rate during an off-schedule policy meeting. This is an unusual position for this central bank, which is seen as especially conservative, and it is surprising since policymakers have been particularly worried about the risk to financial stability stemming from credit-rating downgrades.

Such worries became reality, over the past month, when three major rating agencies downgraded the sovereign. This series of negative announcements culminated with Moody’s decision, last Friday, to downgrade the sovereign and, more consequentially, move PEMEX into a sub-investment-grade category.

Banxico’s decision is less surprising when considering the fast-deteriorating economic activity outlook, which contrasts sharply with the relatively muted government reaction seen so far. In fact, when compared to its LATAM peers, the Mexican government continues to stand out for its relatively timid economic policy relief effort, both fiscal and monetary, in response to the coronavirus outbreak.

Mexico is likely to suffer one of the most severe recessions in the region. Banxico stated today that it expects economic activity to drop by 5% year-on-year during the first half of the year, but we expect full-year GDP growth expectations to drop further, possibly towards 7-8% in the nearer term.

As seen in the chart above, even after today’s cut, Mexico’s policy rate remains considerably higher than the levels seen elsewhere in LATAM. In their post-meeting statement, policymakers signaled that further cuts are likely, and that other measures to boost local market liquidity would be implemented.

The more clearly dovish stance, which should consolidate following the sharp drop in headline inflation expected to take place this month, suggests that the terminal rate of this easing cycle is likely to be lower than we previously thought. The cycle is likely to be more frontloaded as well, with the policy rate possibly reaching 4.5% in the next few months, from 6% now.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article