Markets are overestimating the Bank of England’s inflation challenge

- 18 October 2021

- United Kingdom

Governor Andrew Bailey's hawkish comments this weekend suggest a November UK rate hike is increasingly likely. But the rapid succession of rate hikes being priced by investors looks too extreme, not least because any tightening will also involve reducing the size of the BoE's balance sheet. At most, we expect two rate hikes by the end of 2022

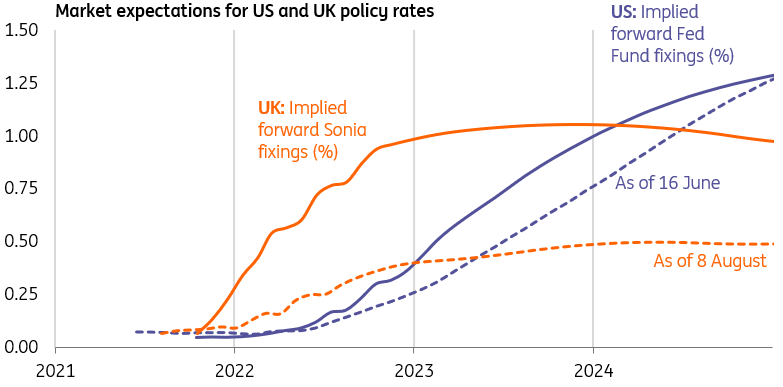

Markets are expecting an ever-increasing amount of tightening in the UK

Bank of England Governor Andrew Bailey this weekend gave his strongest hint yet that markets are right to be pricing a rate rise later this year.

By saying that monetary policy “will have to act”, Bailey has signalled that policymakers don’t see a case for waiting until February or May next year when more information on the ending of the furlough scheme (among other things) will be available.

December’s meeting lacks a news conference and monetary policy report – and don’t forget policymakers put great emphasis on being able to explain their decisions to the public. It’s therefore hard to escape the feeling that a November rate rise is a strong possibility now.

That’s certainly the view of investors, who have also taken Bailey’s comments as a vindication that rates will need to rise several times over the next year. Financial markets are now pricing the Bank rate at 1% by September next year.

Interestingly, this implies that interest rates will need to rise further and faster than at any point in the post-crisis years. Unusually it also signals that investors believe inflation's going to be a much bigger problem for central bankers in the UK than the US – or at least, that the BoE is more likely to do something about it.

There’s little doubting the latter part of that sentence. Not only are UK policymakers talking up the chance of near-term rate rises, but it's also often forgotten that the BoE began tapering back in May and will end QE altogether this December when the Fed will only have just begun slowing purchases.

Markets now think the Bank of England will have to act faster than the Fed

Inflation expectations present less of a challenge in the UK than the US

But there’s a difference between one, or even two, UK rate rises next year, and the rapid succession of hikes that markets now expect. Investors are probably wrong to think the UK is more vulnerable to a longer-lasting inflation problem than the US.

True, UK inflation is going to remain above target for much longer than we’d expected just a few months ago – a by-product of the UK’s particular exposure to higher gas prices. Headline CPI will probably peak at around 4.5-5% next April when the next energy price cap increase comes through. Supply chain issues at home and abroad will maintain the pressure too.

Investors are probably wrong to think the UK is more vulnerable to a longer-lasting inflation problem than the US

Bank of England Governor Bailey has repeatedly said he’s wary of current inflation rates becoming ‘permanently embedded’ – and that’s the lens that markets have been viewing higher electricity prices through too.

But it's worth asking how might that work in practice. Workers could see price rises as an incentive to ask for higher wages, though in practice formal wage bargaining is much less prevalent in the UK than in other parts of Europe.

Another possibility is that consumers start to bring forward spending in anticipation of higher prices, pushing up economic activity today. There's not much evidence (yet) of this in the consumer inflation expectations surveys, which haven't broken as far above pre-crisis averages as we're seeing in some US data. Businesses could also take higher inflation rates as a greater incentive to push up prices. But more likely the dominating effect of the spike in electricity and imported goods prices will be to reduce consumers' spending power on other products. Consumer confidence is already starting to fall noticeably.

Remember too that unlike the US, which has generally seen larger fiscal support through the pandemic (especially for lower earners), the UK government is tightening up - most recently via a sharp cut in welfare payments.

UK household inflation expectations haven't (yet) risen as quickly as in the US

Wage growth may not be as sustained as current shortages suggest

In short, the outlook for interest rates for the next year comes back to wage growth, and whether it stays elevated for a sustained period, akin to what’s starting to happen in the US.

The data is unfortunately not much help right now, though the ONS reckons the underlying trend in pay is consistent with pre-virus levels. There are indeed plenty of stories of worker shortages across the UK economy. Hiring is bouncing back rapidly in sectors hit hard by the Covid-19 crisis.

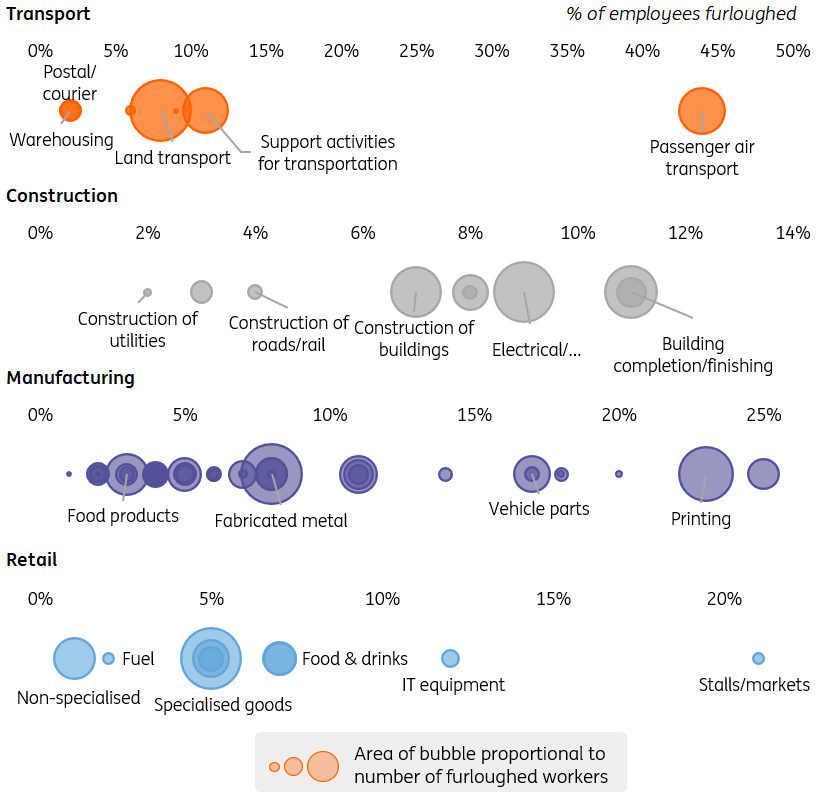

Yet recent data from the now-ended furlough scheme suggests the story is more balanced. It reveals that August's furlough rates were surprisingly high across several sectors, despite many being close to pre-virus levels of activity. That roughly 60% of those furloughed were in small businesses also suggests a lack of confidence among some firms when bringing back employees.

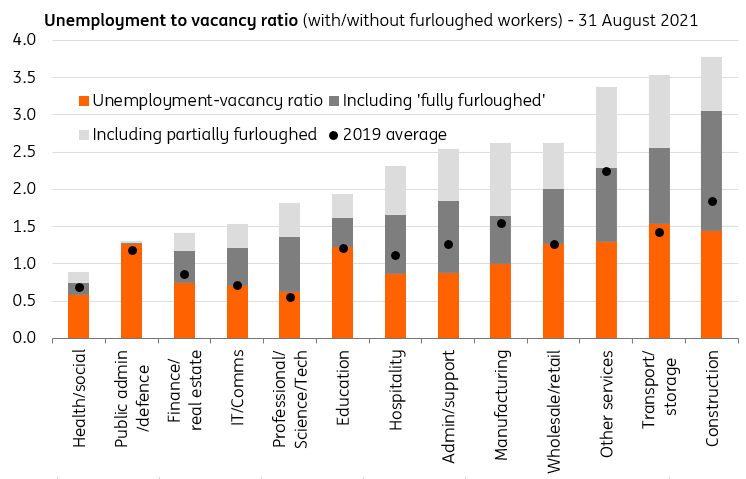

Indeed when you combine the numbers of unemployed and furloughed workers, the number of people theoretically chasing each vacancy is still generally higher than it was before the virus arrived (see chart below).

Unemployment-to-vacancy ratios are often above 2019 levels when furlough numbers are included

Admittedly we don’t expect a huge spike in unemployment now the furlough scheme has ended, and so far there’s been no discernible rise in redundancies. But at the very least, we're likely to see more employees working fewer hours than they’d like.

That doesn’t necessarily ease the shortages being seen elsewhere immediately. What’s interesting from furlough statistics is the stark differences in usage within industries. Take construction, where very few civil engineers were on the scheme over the summer, but it was a very different story for those involved with finishing new buildings.

That mismatch will take time to iron out, but the underlying story is one of some lingering slack in the jobs market. The challenge of raising the UK's mediocre productivity growth also hasn't gone away.

Furlough rates in August were wildly different even within sectors

Furlough rates within sectors (% of eligible employees)

'Quantitative tightening' also means slower rate hikes

There are other reasons to expect caution from the Bank of England too. Brexit uncertainty doesn't help, given the residual risk of some form of trade war, depending on what both sides can agree on the Northern Ireland protocol.

It's worth remembering too that rate hikes are set to come alongside reductions in the size of the Bank of England's balance sheet. Reinvestments of maturing QE bonds are set to end when rates hit 0.5%. And while the initial impact of that may not be huge, it's still a form of tightening that reduces the need for rate hikes. If nothing else, this has never been done before in the UK, and policymakers may decide to tread carefully on rate hikes for at least the first few months.

That markets are now pricing in bank rate at 1% next year is also interesting, because policymakers have indicated that’s the point at which it could accelerate the balance sheet unwinding process by selling gilts back into the market. Whether or not we’ll get to that point is questionable; it would certainly be risky. But it does suggest that 1% is something of a ceiling for the foreseeable future.

Our Bank of England view

The message here is that markets are probably right to price an earlier 15bp rate hike in the UK than the US. Bailey's comments this weekend mean our current forecast of a May 2022 rate rise is probably too late. It's a close call between a November and February move, but we suggest the former is more consistent with the Governor's latest hints.

Still, we don't share the markets' conviction that this will be followed by a series of rate hikes. More likely, the most we'll see next year is a further 25bp hike, taking the Bank rate to 0.5%, followed by the start of balance sheet reduction.

We may even see the BoE hint at this in its November forecasts. Policymakers plug in market-rate expectations into the forecasts, and if the steeper yield curve means inflation is projected to be below target in 2-3 years, it would be an implicit hint that investors are jumping the gun.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more