Market reaction to Liberation day - this is just the beginning

Impact effect? Risk-off, and lower Treasury yields. No break of prior ranges on market rates, but it smells like they want to go lower ahead. On FX, the new global trading regime still argues for a stronger dollar, but it won't be easy to convince markets protectionism is here to stay. Overall, it feels like this could unravel further in a negative fashion

Treasuries continue to view tariffs as a bigger immediate risk for activity

Donald Trump spoke of 10% tariff across the board before he was elected president. He’s kept true to that, imposing a blanket tariff. But he’s overlayed that with additional tariffs on a wide group of countries that the US views as already implicitly placing tariffs on US exports. See more detail here. Basically, the 10% tariff gets amplified to something closer to 20-25%, on average. To the extent that this places upward pressure on US domestic prices, there is clear negative tint for bonds. But the dominant reaction is one of apprehension on what this all means for activity, and hence another push lower in market yields has been the main outcome.

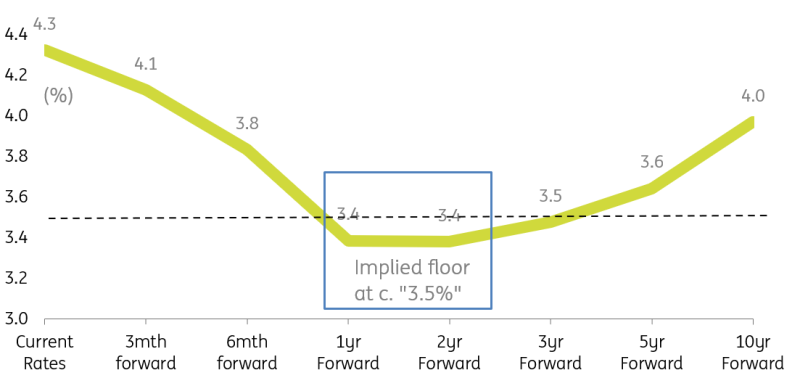

At least for now we're still looking lower in yield. The only caveat is the floor we identify at around 3.5% for front-end rates (e.g. 1mth SOFR). That plus a 50bp 10yr swap spread pitches 4% as something of a floor for the 10yr Treasury yield. If Treasuries really want to rally, that 'floor' needs to be lower. To get lower, we'd need to have a greater recession risk. That's the direction of travel, albeit the case for outright recession has not been fully made as of yet.

The market discount for the path of 1mth SOFR

Risk-off has been a dominant play in recent weeks, and little there to change that

As a one-day trade, we've in part taken our cue from the risk asset space, and in particular equity markets. We don't love doing this as we think the bond market is 'smarter', and more long term in thinking. The impact reaction has been for lower equities, as priced from the futures. That's about the right reaction, but still remarkable as much of what was delivered was in a way anticipated. The picture being painted from a generic market sense is in consequence quite negative.

Anticipate further fallout over coming days. But distilling through the fog, it does feel that Treasury yields are in a mood to test lower still for a bit, trading off the growing recession risk being priced from a whole array of weak-leaning survey evidence, with tariffs acting as a tipping point. This needs to be dis-proved by events before Treasuries can start to latch on to the sticky inflation / elevated fiscal deficit narrative that sustains a bearish tint that can come back into play in due course.

Look for convergence of Treasuries to lower yielders, while higher yielders can ease lower

In terms of the international context, expect a period of reflection. To the extent that US yields fall in consequence, there is a downward effect on global rates, and a tightening versus lower yielders. Versus higher yielders, there is room being made for those rates to ease lower. No new news on Mexican tariffs, and Brazil was listed with a 10% tariff, which in net terms is a positive outcome for Latam.

For Asia, it a more troubling complex. China now averages at a 54% tariff, while Vietnam, Korea, India, Indonesia and Thailand are up for special extra tariffs mostly in the area of 25% to 45%. Then in Europe, a selection of countries are now on a 20% tariff, and we need to await retaliatory measures. Overall, there are negative kick-backs which likely mean a risk-off and lower yields combination dominating. See more detail on the tariff-impacted macro risks for Europe here.

Expect a degree of correlation in terms of performance ahead. So risk-off should be a common theme, and should lower market rates. Europe is the most likely to buck this trend further forward, as fiscal spending plans get fast tracked in the wake of a Trump that's not for changing. This can push yields up in Europe. Similar for Japan in terms of yield. At the other exteme, the likes of Mexico and Brazil can see market rates being pulled lower by lower Treasury yields.

Asia EM FX the biggest loser

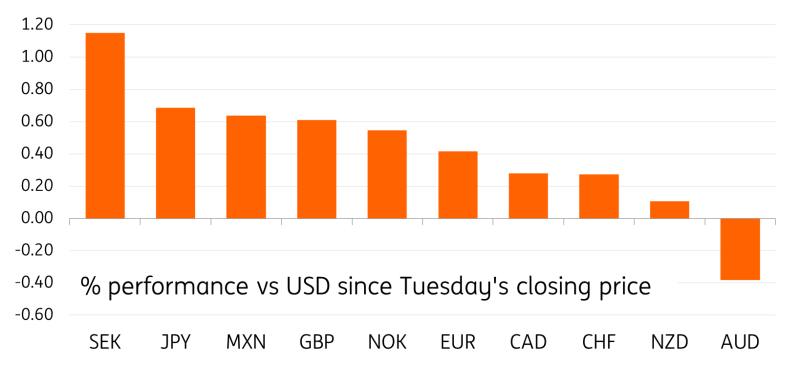

The currency market has faced major volatility around the US tariff announcement. The headlines suggesting the base rate for all countries was set at 10% sent the dollar tumbling, but country details unveiled shortly after triggered a broad rebound of the greenback. CAD and MXN have held up gains better than others thanks to USMCA exemption from reciprocal tariffs, while the yen remained the favourite hedge as risk sentiment soured.

The worst-hit region by this tariff announcement is undoubtedly Asian EM. Some Asian currencies are not trading at the time of writing, and we’ll need to wait a few hours before we can fully assess the fallout in the FX market. USD/CNH has strengthened following China's 34% tariff designation – one of the highest rates imposed and yuan proxies AUD and NZD have shown some weakness, even if modest in magnitude. We anticipate broader Asian EM currencies will face downward pressure as trading resumes.

"Liberation day" FX performance

Tariffs open interesting relative value opportunities

Two critical aspects deserve attention from an FX perspective. First, this represents just the opening chapter of an evolving narrative. The US administration has signalled flexibility in tariff negotiations, and the full width of the currency fallout will primarily depend on individual countries' diplomatic and trade leverage as well as on the US will to tolerate the negative implications and focus on collecting tariff revenue.

This leads to our second takeaway: the focus may well shift from broad dollar movements to relative value opportunities. It is abundantly clear by now that this was not the kind of event that would turn the tide for the dollar, and data can still prove to be the major driver of USD direction. But different countries’ abilities to negotiate away from tariffs can generate compelling relative value opportunities across G10 and EM FX.

We have pointed repeatedly at European currencies as vulnerable, and we still see downside risks as Trump has been vocal about growing hostility towards the EU, which may result in smaller trade negotiation room for the bloc. Yet, pre-tariff-announcement euro strength emerged following reports of EU Commission plans for economic support measures. Thursday's anticipated details – potentially including progress on common debt instruments and reduced intra-EU trade barriers – warrant close attention before confirming our cautious EUR/USD outlook.

What about Trump’s weaker dollar hopes?

From an economic fundamental perspective, “liberation day” is a bullish dollar event. Indeed, the Treasury has indicated this is the peak for tariff threat and things can only improve from here via trade negotiations, but that does not explain by itself the dollar’s inability to rally. The real question is how long tariffs will stay in place, and the currency market retains a sanguine view on that. One way to interpret this optimistic stance is that inflationary pressures from higher import costs might accelerate trade dispute resolutions.

Looking ahead, Trump's well-documented preference for a weaker dollar adds another layer of complexity to future trade negotiations. We answered ten questions on how a Mar-A-Lago accord to devalue the dollar might look like in this note. We’ll see whether once the inflationary tariff shock has been absorbed Trump will turn the focus on weakening the dollar.

We still think the radical change in global trade relationships in the first few months of Trump’s presidency argues for a strengthening of the dollar across the board, but if US data keeps deteriorating and the US is forced to water down its tariff threat, the dollar would weaken without any artificial intervention. In this environment – and given the risks of more equity losses and lower long-end US yields – the yen may well emerge as the most attractive currency in G10 in the near term.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article