Central Banks in 2022

From rate hikes to tapering, we look at what the world's major central banks are likely to do next year

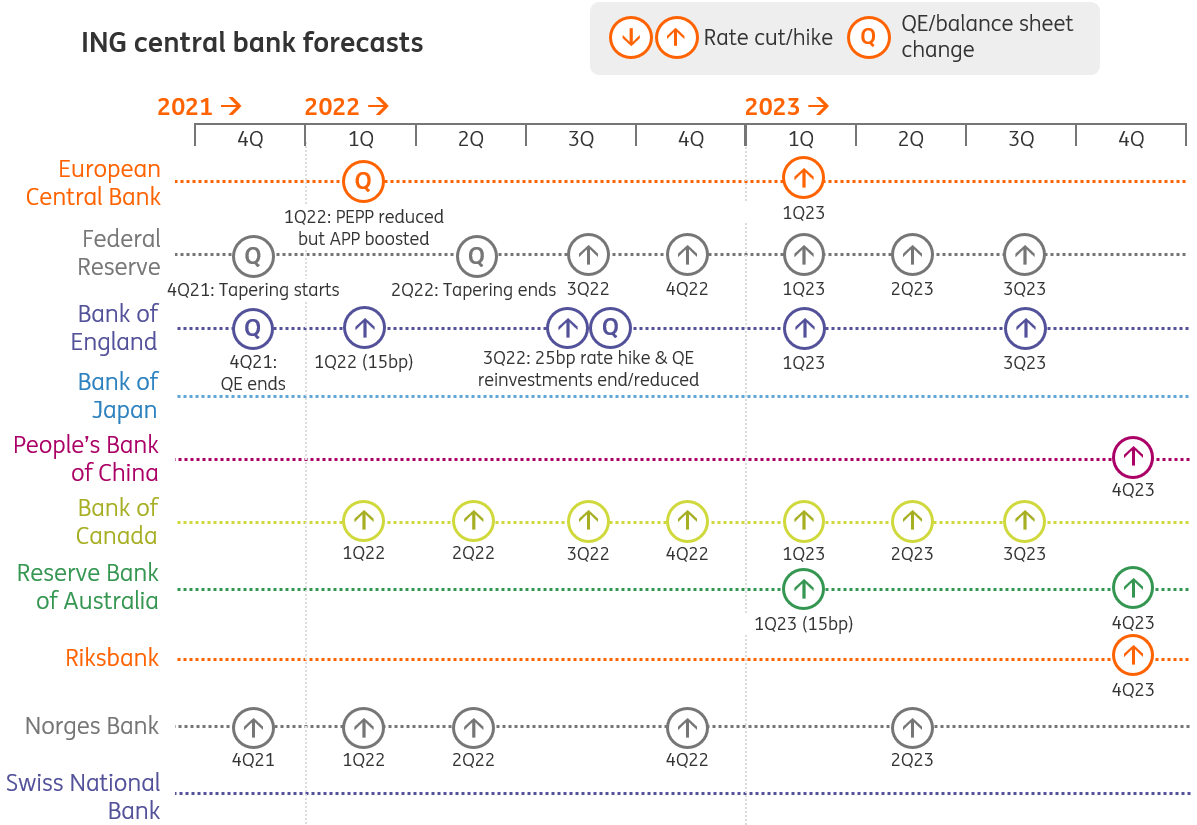

ING's view on central banks in 2022

Federal Reserve

It may seem odd timing given the emergence of the Omicron Covid variant, but Fed Chair Jerome Powell has acknowledged that it is time to retire the “transitory” description of inflation and is now mulling the potential for a swifter conclusion of QE tapering that would also open the door to earlier interest rate increases. There are significant uncertainties presented by Omicron, which could weigh on growth, job creation and inflation, so we narrowly favour the Fed waiting until the 27 January FOMC meeting before accelerating the taper to $30b per month.

Nonetheless, there is clearly the potential for the announcement to come in December if scientific evidence suggests we are not entering a darker period for the pandemic. At present, we are sticking to our two 25bp hike call for the second half of 2022, but if the all-clear is sounded we would imagine three hikes is far more likely.

European Central Bank

The fourth wave and the Omicron variant have complicated the ECB's life and more particularly its path towards the exit from the emergency measures. However, we expect the ECB this time to resist its old reflex to continue or even step up emergency measures, and to replace its Pandemic Emergency Purchase Programme with a new transitory programme starting April 2022. As a result, monthly asset purchases will be gradually reduced and brought to an end before late-2022 as high inflation rates indeed turn out to be transitory but medium-term forecasts point to inflation rates of around or above 2%. These will be the perfect conditions to start talking about a first rate hike to be delivered in early 2023.

Bank of England

We now expect the BoE to hold off on a December rate rise, assuming the uncertainty surrounding Omicron hasn’t materially lifted before the next meeting. But unless the new variant decisively changes the economic outlook, then a rate rise in February looks likely. In November, policymakers implied they wanted to be sure that the end of furlough in September hadn’t triggered a serious rise in redundancies – and all the data so far suggests it hasn’t. However markets, which are still pricing 1% on bank rate next year, are still probably overestimating the pace of tightening in 2022.

We are forecasting a rate rise in February and August, which would imply the Bank also begins reducing the size of its balance sheet by ending reinvestments. A third move – taking Bank rate to 0.75% – is possible in 2022. Remember though, if policymakers are divided on whether to hike rates now, there’s unlikely to be consensus for the sharp adjustment in interest rates that markets have long been expecting.

People's Bank of China

The PBoC did not cut the required reserve ratio when the real estate sector’s default payments triggered a financial market sell-off. The government has recently calmed down its rhetoric on policy, but we would note that the deleveraging reform continues. As the policy tone returns to normal, we expect the central bank to refrain from changing interest rates, e.g. the loan prime rate and the 7D reverse repo. If the government changes to a pro-growth policy direction, the PBoC might cut the RRR by 0.5 percentage points. We expect one rate hike of 25bp in 4Q23 when deleveraging reform should come to an end, and economic growth will be stronger.

Bank of Japan

The Bank of Japan remains locked in an endless loop of low rates and asset purchases that aren’t doing anything particularly helpful, but could pose a risk to the market if they were to be withdrawn. This situation has been going on for years and looks set to persist for years to come, or at least until Governor Kuroda’s term is over in April 2023. Some members of the BoJ have recently indicated some more confidence in the path of inflation. But with core inflation excluding food and energy recording a 0.7% year-on-year decline in October, we don’t share this confidence.

Bank of Canada

The Bank of Canada decided to end QE in October and brought forward its guidance for the timing of the first rate hike to mid-2022. The economy is growing strongly and inflation will soon breach 5%. At the same time, Canada has been far more successful at job creation than the US with employment already above pre-Covid levels. Given less spare capacity than most other economies, we immediately shifted to forecasting four 25bp rate hikes in 2022. We are reluctant to make any changes to this view right now given the uncertainty over Omicron, but the obvious risk is that the BoC ends up delaying the first hike until 2Q should consumer caution kick in on Covid anxiety.

Reserve Bank of Australia

The RBA has been softening its insistence that rates will not be raised until 2024, and this is now wrapped up with various caveats and scenarios that suggest they are working out a way to shift their base case to 2023. The recent Omicron shock may postpone an announcement of any change, but markets have already priced in a very aggressive tightening schedule, that probably goes too far the other way. While wages growth remains fairly benign, and inflation is still not an issue in Australia, the RBA can continue to maintain its dovishness. But we suspect the first rate hike will not come too long after the Fed’s liftoff, so 1Q23, with a possibility of an end-2022 hike.

Swedish Riksbank

The Riksbank won’t be joining others in hiking rates in 2022, though it has inched a little closer to tightening in recent weeks. Policymakers have, for the first time, put a hike into its published interest rate projection, albeit for 4Q 2024. In practice, the first rate rise is likely to come much earlier, perhaps towards the end of 2023.

Where the Riksbank differs from others is that, like the Bank of England, it has begun talking about shrinking its balance sheet. While details are scarce, it looks likely that policymakers will begin reducing the pool of covered bonds accumulated through the Covid-19 crisis under quantitative easing, most likely in 2023. The upshot is that quantitative tightening, as this process is sometimes known, could come well before the first rate hike.

Norges Bank (Norway)

Norway has already hiked rates once, and has hinted at another move in December. That’s a little more uncertain given the Omicron-fuelled decline in oil prices, and the sharp rise in Covid-19 cases domestically. For now, we reckon policymakers will still go ahead with the forecast rate rise – not least because the November statement more-or-less said that this was nailed on. Norges Bank is forecasting another three rate rises next year and we’re not inclined to doubt that, unless of course Omicron turns out to be a significant problem for the world economy.

Swiss National Bank

We do not expect any change in the SNB's monetary policy; it will continue to intervene in the foreign exchange market when it deems it necessary in order to combat an excessive appreciation of the Swiss franc. The more inflationary context makes it less concerned about deflation and should allow it to tolerate slightly higher levels of the franc than in the past, but in a moderate way in order to maintain its credibility. The expected tightening of monetary policy around the world should give the SNB some relief, but not enough to consider starting to tighten itself.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

2 December 2021

ING global outlook 2022 This bundle contains 17 Articles