Euribor and a global IBOR overview

- 25 February 2021

- Rates

Euribor will continue, but the quest to find appropriate fallbacks for cash products is still underway. There is a desire for forward-looking euro short-term-rates as a fallback for some products, but that hinges on the development of the OIS market. We also provide a broader overview of benchmark reform developments beyond the major Ibors

Euribor stays, but work on required fallbacks continues

The Euribor has been fully reformed to comply with the regulatory requirements of a critical benchmark. There are no plans to discontinue Euribor. However, that does not imply all work is done in the Eurozone. One remaining issue is that even if a benchmark continues to exist, the regulation still requires that contracts and instruments referencing a benchmark need to incorporate fallback provisions.

Regulation still requires that contracts and instruments referencing a benchmark need to incorporate fallback provisions

This week the working group released the responses to the public consultation on a) the events that would trigger the fallback, and b) the €STR based fall back rates to be used in cash products. It was acknowledged that the ISDA IBOR Fallbacks Supplement to the 2006 ISDA Definitions and the IBOR Fallbacks Protocol covers the derivatives.

While a backwards-looking compound €STR will be the ultimate backstop in all cases, for some asset classes there is still a desire to have a forward-looking term €STR as a first fallback instance within a waterfall structure, such as for retail mortgages, consumer and SME loans or trade and export financing products.

Being able to meet the desire for a forward-looking term benchmark hinges on the further development of the €STR OIS market. For all practical purposes, EONIA OIS and €STR OIS already represent the same underlying market given the linear link between the two fixings (EONIA = €STR + 8.5bp). Still, the final transition to €STR has yet to occur. Once also the €STR-linked EONIA is discontinued at the start of 2022 the expectation is that market activity will fully consolidate in the €STR based OIS.

Being able to meet the desire for a forward looking term benchmark hinges on the further development of the €STR OIS market

However, some question marks remain surrounding whether the required level of robustness for a forward-looking term €STR benchmark can be achieved. As has been stressed at the working group meetings, it remained to be seen whether the current liquidity of the OIS market (EONIA and €STR) was sufficient for the calculation of a term rate and whether a methodology based on committed OIS quotes would perform well in periods of market stress.

ECB representatives also expressed concern regarding the high level of concentration observed in the OIS markets. Concentration makes a benchmark more susceptible to the behaviour of individual agents.

A study from 2019 showed strong concentration in terms of counterparties as well as countries out of which participating banks operate. Based on the ECB’s money market statistical reporting data set covering 2018, France accounted for 62% of all reported volumes, followed by Germany with 20%. In terms of counterparty concentration data showed that the ten most active banks represented more than 75% of market turnover.

Overview of the global benchmark landscape

We have covered the major USD and GBP Libors impacted directly by the FCA regulation in previous sections.

Among the other majors, Japan’s JPY Libor will also require a transition as it is also anticipated to be discontinued by the end of this year. For some cash instruments such as loans, the domestically used TIBOR benchmark could still find use as a fallback in a waterfall structure ahead of the designated uncollateralised TONA RFR. This multiple-rate approach differs from Switzerland which has taken the hard line of discontinuing CHF Libor and requiring a full transition to the secured SARON RFR.

In the Eurozone, EUR Libor will come to an end, but it is only a niche benchmark. The main Euribor benchmark will still be around.

In the following sections we provide an overview of the benchmark landscape beyond the majors.

Overview of Ibors in the Americas

In the Americas outside the US, Canada has chosen a multiple-rate approach letting a reformed CDOR exist next to the collateralised CORRA RFR, although the ambition is to have the latter dominate. Note that the 6-month and 12-month CDOR tenors will be discontinued this May.

Mexico also plans to follow a multiple-rate approach by retaining a strengthened interbank TIIE rate and replacing the shortest tenor with the new collateralised Overnight TIIE RFR. Brazil has started a review of the collateralised Selic to ensure its IOSCO compliance. It is already a default fallback of the DI rate which serves as underlying for futures contracts. Based on the latter Term DIs are considered, but also backwards-looking term RFR are being explored.

Overview of Scandinavian Ibors

Scandinavia has or at least plans to follow a multiple-rate approach by keeping the known Ibors.

Norway’s NIBOR was reformed in 2019 and fallback solutions using Nowa RFR are being worked on. Denmark’s CIBOR was strengthened in 2019 and Denmarks Nationalbank is working on DESTR as an unsecured RFR set to be launched at the beginning of 2022 with aims to transition from the current ‘Tom/Next’ short-term reference rate.

After a review of its STIBOR, Sweden is anticipating a seamless transition to an adjusted STIBOR benchmark after consultations this year. The Riksbank has launched a six-month testing phase for SWESTR last month, the future designated unsecured RFR that will replace the shortest STIBOR tenor (t/n).

Overview of EMEA Ibors

In central Europe, Poland has reformed its WIBOR and is considering using the existing WIBON as a fallback in the context of EU BMR. In many places, benchmark reforms have yet to kick off in earnest, although discontinuation of existing Ibors is also not foreseen. Alternative rates have not yet been designated but there are existing short term rates that could potentially be used.

In the wider region, Israel is seen sticking to TELBOR (based on quoted o/n rates) for now but is exploring ways to fully adapt to global benchmark standards. Turkey pursues to follow global timelines in discontinuing TRLIBOR and transitioning to the collateralised TLREF RFR which has already been widely adopted, including functioning derivatives markets.

South Africa eyes longer-term plans of discontinuing JIBAR. It has identified a set of RFR candidates in a first step but does not exclude the RFR could coexist alongside a new risk-based term rate.

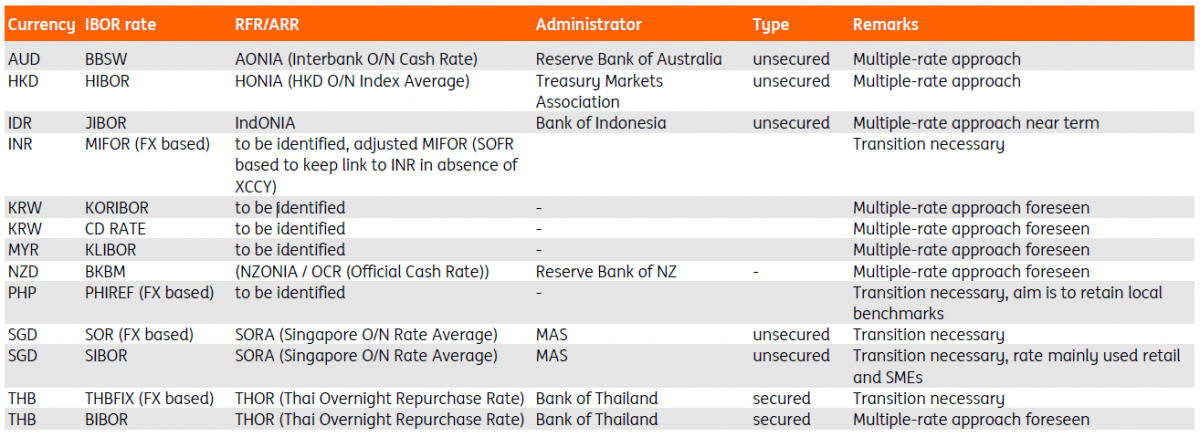

Overview of APAC Ibors

Developed markets are taking the lead in the APAC benchmark reform process.

Australia has domestically adopted a multiple-rate approach, keeping a reformed BBSW rate (the Ibor) alongside the interbank overnight cash rate (AONIA) as RFR. For some tenors, it is assumed that the RFRs may be more suitable, and the global transition may also lead to a corresponding migration away from the BBSW. New Zealand also keeps its Ibor, the BKBM and the compounded Official Cash Rate (NZONIA) will serve as a fallback, but the intention is to develop an RFR and develop a term structure.

A multiple-rate approach is a way forward in Hong Kong, with an unsecured HONIA as the RFR. Singapore is replacing the SOR rate, which has USD Libor as an input, with the unsecured SORA. This will eventually also replace the SIBOR, a benchmark mainly used in retail and by SMEs. Thailand faces a similar issue with THBFIX which uses USD Libor as input. It will be replaced by the THOR repo rate, although a THBFIX fallback calculated from USD Libor SOFR fallback will be available for legacy contracts. Despite its drawbacks, BIBOR is maintained as a forward-looking term rate. Early in its planning, India also faces the issue of USD Libor dependency of its MIFOR rate which will need to be transitioned. The same goes for the Philippines’ PHIREF, but the stated aim is to retain the local benchmark rates.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Libor Transition: No please I insist, you go first

- This bundle contains 3 Articles