Less sustainable issuance by banks in 2025

Banks are expected to reduce their issuance in sustainable format next year against the backdrop of overall lower issuance volumes

ESG issuance falls short to last year

For the first time in a decade, the supply of EUR sustainable bank bonds will not surpass the previous year’s volumes. With lending growth stagnating and overall supply activity by banks slowing down, ESG bond issuance by banks in 2024 is likely to end the year close to €75bn.

Banks globally have issued €70bn in EUR-denominated ESG bonds so far this year, down from €74bn last year. Covered bonds and preferred senior unsecured bonds represent 27% and 26% of the year-to-date ESG print, respectively, while bail-in senior issuance makes up 40% of the green and social use of proceeds supply. Subordinated bonds and RMBS have a modest share of 5% and 2%, respectively, in the 2024 ESG print of banks.

Lower issuance by banks will coincide with less ESG supply in 2025

The slower ESG issuance by banks this year has been well spread across the different use of proceeds categories, with green, social and sustainability issuance all three slightly below last year’s YTD print. Green issuance still represents the bulk of the ESG supply with a share of 79%, followed by social issuance with 18%. Sustainability (i.e. a combined green and social use of proceeds) only made up 2% of the ESG issuance.

This shows that social bond issuance continues to struggle to gain momentum following the surge after the Covid-19 pandemic. Part of the reason is the stronger regulatory emphasis on green bonds, as outlined in the EU taxonomy regulation and the EU green bond standard.

In the unsecured segment, the proceeds use remains predominantly green. However, in covered bonds, social issuance is keeping better pace with green issuance. For example, social and sustainable covered bond issuance has reached nearly €8bn YTD, surpassing the €6.5bn in unsecured social and sustainable issuance. In contrast, the €11bn in green-covered bond issuance is only a quarter of the unsecured green supply.

Green will remain the dominant use of proceeds type

The 2025 ESG print by banks will fall to €70bn

We anticipate a slight decrease in ESG supply by banks in 2025 compared to the previous year, with expected ESG issuance around €70bn. Of this, 80% is projected to be in green format. Banks are expected to issue €20bn less in total (including both vanilla and ESG bonds), and lending growth is forecasted to increase only gradually next year. Hence, sustainable loan portfolios will see modest growth.

Banks may find opportunities to further grow their sustainable assets through the criteria set in the EU Taxonomy’s environmental delegated act (e.g. to support the circular economy), but climate change mitigation will remain the key driver of green supply.

ESG redemption payments will rise from €15bn to €34bn. This will also free up sustainable assets for new ESG supply, but probably not for the full amount due to the changes made to some of the green bond eligibility criteria since the bonds were issued.

Banks will repay €34bn in sustainable bank bonds in 2025

Limited issuance expected under the EU green bond standard

As of next year, banks can also opt to issue their green bonds under the EU green bond standard. Considering the low first green asset ratio (GAR) disclosures by banks this year, we doubt we will see a lot of bank bond supply under this standard. Based upon the Pillar 3 disclosures of a selection of 45 banks, the average Taxonomy alignment of bank balance sheets per country varies in a low range of 1% to 8%.

Green asset ratio disclosures point to low Taxonomy alignment

Given the low reported EU Taxonomy alignment of banks’ mortgage lending books, many banks may struggle to assemble a sufficiently large portfolio of Taxonomy-aligned assets to support green issuance under the EU GBS format. This is unless they are confident in the growth prospects of their Taxonomy-aligned assets within five years of issuance, particularly for standalone deals where a portfolio approach is not used.

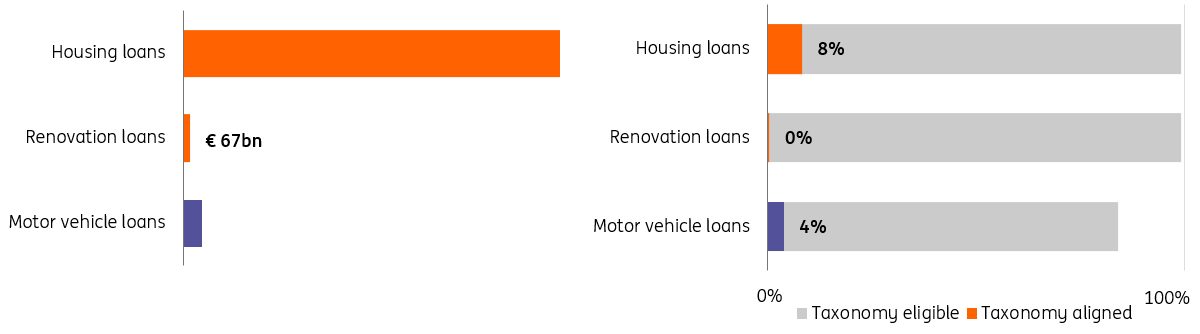

Loans to households have a low Taxonomy alignment

Banks have few renovation loans outstanding and they are almost 0% taxonomy aligned

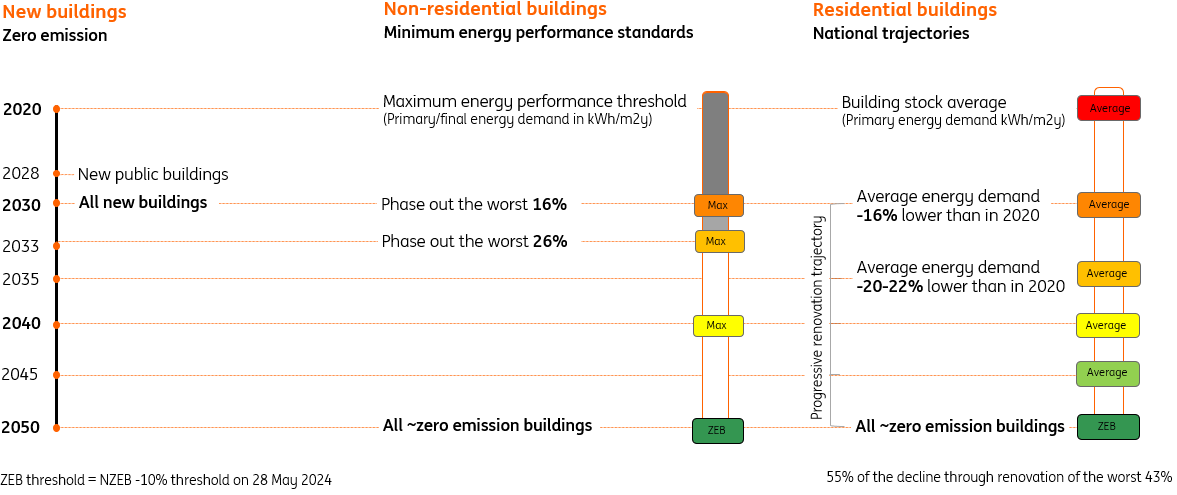

Regulatory initiatives, such as the Energy Performance of Buildings Directive (EPBD), promoting the renovations of buildings within the EU, should in time see the portfolios of Taxonomy-aligned assets grow. Given the timelines set, this will not be a major support in 2025.

To encourage banks to provide lending for the renovation of the worst-performing buildings, the European Commission is working on a separate delegated act for a comprehensive portfolio framework for voluntary use. The response period for the European Commission's call for evidence on the portfolio framework ended on 5 November, with the Commission now aiming to launch a public consultation on this topic before year-end.

Timelines under the Energy Performance of Buildings Directive

Banks with a more balance sheet size and the ability to select enough Taxonomy-aligned assets for a benchmark-sized deal are likely to be among the first to test the waters by issuing bonds under the EU Green Bond Standard.

For the issuance of bonds with a longer maturity, banks may wish to finance a distinct set of Taxonomy-aligned assets rather than allocate their bond proceeds to a portfolio used for multiple European green bonds (ie portfolio approach). If the EU Taxonomy technical screening criteria are amended, assets not meeting the amended criteria can stay part of the green portfolio for seven years at most. Instead, standalone deals will in principle keep their EU green bond status based on the old technical screening criteria if these are amended before the bond's maturity.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

13 November 2024

Bank Outlook 2025: Clearing the fog – bank risks and market shifts This bundle contains 6 Articles