Latin America: Recession deepens fiscal challenges

Covid-19 continues to spread across Latin America but, given the mounting economic costs of stay-at-home orders, governments are easing social isolation guidelines. Robust economic policy responses should help soften the recession but will leave behind severe fiscal challenges that should alter intra-region relative performance post-pandemic

Deep uncertainties and uneven recovery paths

Latin American countries continue to struggle to control the spread of Covid-19, exacerbating uncertainty about the future of stay-at-home measures and complicating any assessment of the depth of the recession that regional economies will suffer this year.

The health crisis is unlikely to abate soon given the inherent difficulties in combating the spread of Covid-19 in less developed countries. Dense living arrangements together with widespread labour informality complicates the region’s ability to enforce mandatory social-isolation procedures.

Dense living arrangements, widespread labour informality along with the prevalence of weaker health-system infrastructures across the region, help explain the emergence of regional hotspots in Lima, Santiago, Guayas and Manaus

Moreover, unless governments have the ability and logistical capacity to transfer vast amounts of resources to businesses and households, which is not the case for most of Latin America, returning to work becomes imperative sooner or later. These vulnerabilities, together with the prevalence of weaker health-system infrastructures across the region, help explain the emergence of regional hotspots such as Lima, Santiago, Guayas and Manaus.

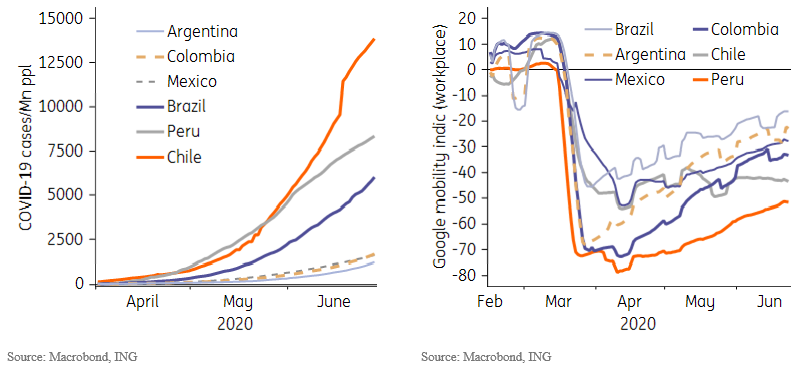

As the graphs below suggests, even though confirmed Covid-19 cases continue to rise across the region, workplace mobility is also gradually rising. Chile and Peru are notable exceptions, as the greater severity of the virus spread have resulted in a delayed return to work.

Continued rise in Covid-19 has not prevented gradual return to work

This gradual return to normalisation suggests that, perhaps with the exception of Chile, April likely marked the bottom for economic activity. The collapse in activity varied materially across countries, with Peru’s massive 40% year-on-year drop standing as a clear outlier when compared to the smaller drops seen in Brazil and Chile, of 15%, Colombia and Mexico, 20%, and Argentina's 26%.

The recovery should also be uneven, with the path likely influenced by the trajectory of the health crisis, the pace of the reopening and by the economic policy decisions taken place over the past few months.

Recession and fiscal stimulus raise questions about fiscal sustainability

Policymakers have, with the notable exception of Mexico, responded with vigour to the crisis. Aggressive monetary policy easing was adopted throughout the region, with the policy rate now set at, or very near, their “technical lower bound” in most places. This likely means near 2% in Brazil and Colombia, and at 0.25-0.5% in Peru and Chile.

Aggressive rate-cutting cycles, together with the rise in risk aversion, resulted in widespread FX weakness across the region. Brazil’s FX weakness stands out but appears consistent with the fact that Brazil also saw the greatest reference-rate drop when compared to historical averages. Overall, however, FX weakness may have increased business uncertainty, but it is not a binding constraint to monetary policy right now, given that inflation is low throughout the region.

Policymakers have, with the notable exception of Mexico, responded with vigour to the crisis

Fiscal policy was also adjusted, to help mitigate the collapse in household and business income resulting from the interruption in economic activities. The amounts involved appear commensurate with the dimension of the health crisis seen in each country, with Chile and Peru leading with the most generous fiscal packages, followed by Brazil, and Colombia.

Mexico, once again, stood out for its unusually modest counter-cyclical policy effort, which contrasts with the fact that Mexico’s GDP is likely to face one of the deepest slumps in Latin America this year.

The different policy choices adopted in each country should result in different challenges and recovery paths over the coming months. Despite the ample policy stimulus adopted in Peru and Chile, it’s hard to be optimistic about faster recovery prospects given the severity of the health crisis still faced by these two countries.

The economic paths adopted by Brazil, Colombia and Mexico should provide especially interesting comparison opportunities, however. The larger stimulus adopted by Brazil, followed by Colombia (medium), and Mexico (small) should help provide important contrasts about the policy choices adopted.

In contrast to Mexico, Brazil’s (and Colombia’s) more generous fiscal package should help expedite the recovery but create severe fiscal challenges in the future. But we also worry that Mexico’s “fiscal prudence” may exacerbate the risk of greater permanent damage to the economy, delay the eventual recovery and, ultimately, create more lasting damage to its fiscal trajectory, while keeping the risk of credit-rating downgrades elevated.

Overall, it’s still too soon to state with great conviction which policy path will prove most effective in the current context. And this should provide much room for performance differentiation in the coming quarters, especially as each country will have to make difficult fiscal policy choices ahead.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

2 July 2020

July Economic Update: From yesterday to tomorrow This bundle contains 10 Articles