Latam FX Talking: The Brazilian real has fared well from the crisis

- 17 April

- FX Argentina Brazil

Of the Latam currencies we cover, the Brazilian real has the most scope to appreciate. A modest net energy exporter, 12% implied yields and perhaps now some political winds of change can all help BRL sustain a break below 5.00/USD. We suspect Banxico may find the peso too strong for its liking, while Chile's peso could be undone by copper later this year

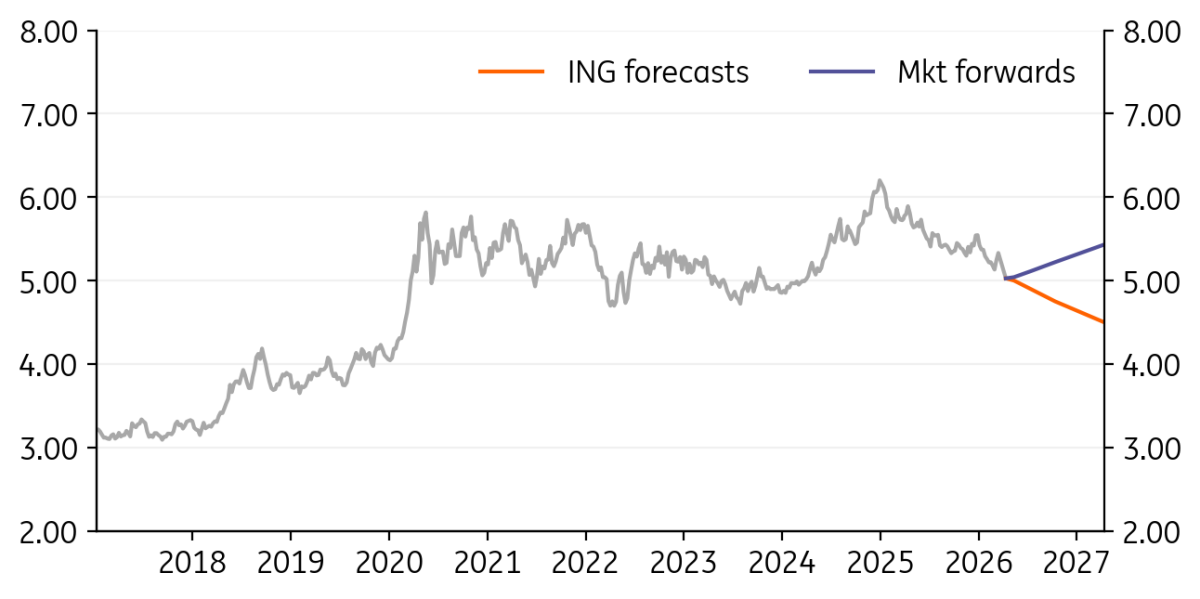

USD/BRL: BRL has room to rally if the pieces fall into place

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/BRL

5.00

|

Neutral | 5.00 | 4.90 | 4.75 | 4.50 |

- Brazil has had a good crisis so far. As a net energy exporter, its terms of trade have actually risen – unlike the big drops seen for currencies in Europe and Asia. That leaves the Brazilian real as one of the market’s favourite high yielders. Here the implied BRL yield through the three-month NDF remains near 13% pa.

- Further strength in BRL requires a further two components to go right. The first is the continuing improvement of Flavio Bolsonaro in the polls such that he beats President Lula in a run-off after October’s election. The second is no fiscal adventure from Lula.

- For reference, on a real effective basis the BRL is still cheap and 40% below 2011 highs. 4.50 is entirely possible for USD/BRL.

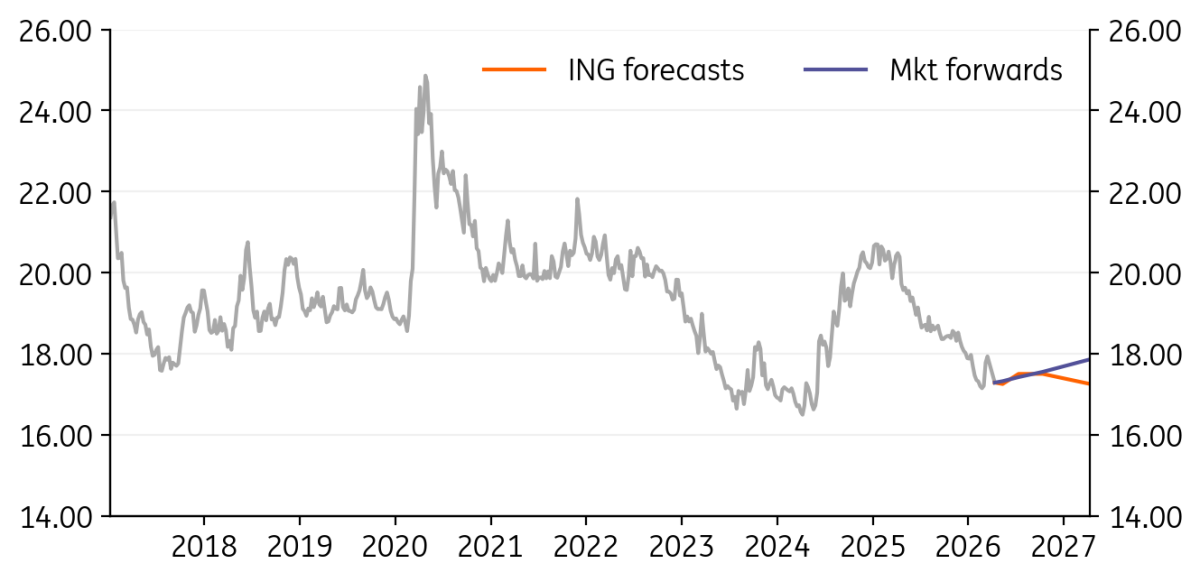

USD/MXN: A much stronger peso won’t be welcome

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/MXN

17.28

|

Neutral | 17.25 | 17.50 | 17.50 | 17.25 |

- In late March, Banxico cut rates 25bp to 6.75%. Even though both headline and core inflation forecasts were revised higher, Banxico still felt that the risk of second-round inflation effects was low and that it would still hit its 3% CPI target in early 2027. Its dovish bias is driven by forecasts for weak GDP growth sub 2%.

- But given a dovish outlook, Banxico will not welcome a stronger MXN. The real, trade-weighted peso is close to its 2024 highs, and the macro backdrop is far less peso bullish. Note also that monthly remittances from the US have dropped to $4.5bn per month from a peak of $6.2bn in 2024.

- We struggle to see USD/MXN sustaining a break of 17.00.

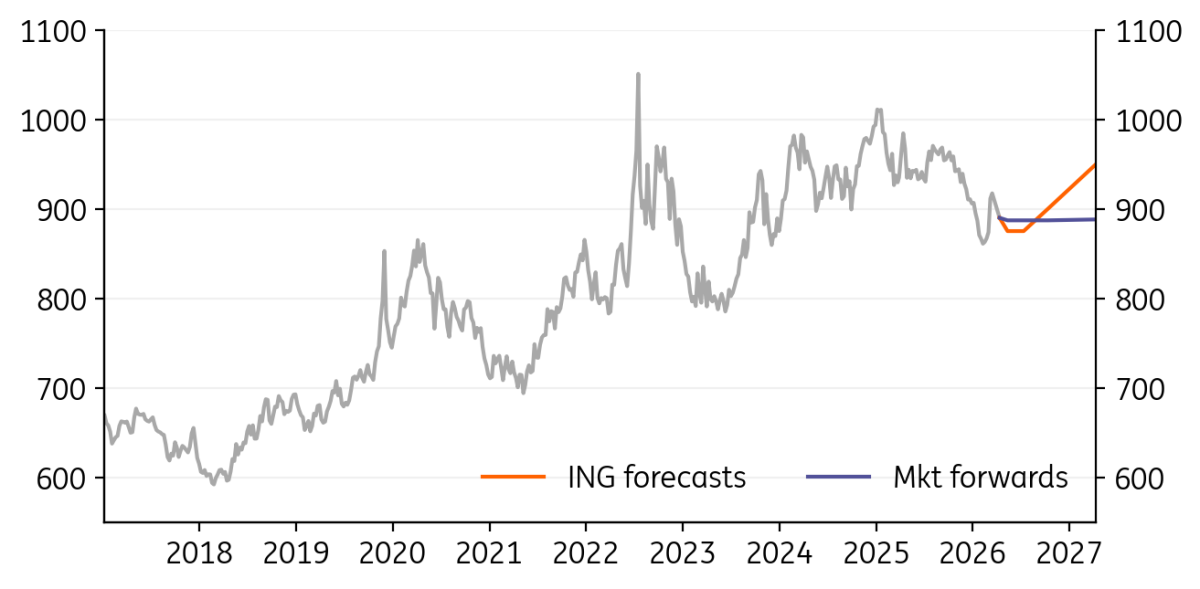

USD/CLP: Copper rebound helps out

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/CLP

887.25

|

Mildly Bearish | 875.00 | 875.00 | 900.00 | 950.00 |

- De-escalation trades dominate, which have allowed both copper and CLP to rebound. However, we doubt USD/CLP will be pressing 850 again. Higher energy prices will damage Chile’s external position and Chile’s copper producers face challenges (and higher prices) of sulfuric acid used in the leaching process. China has banned sulfuric acid exports.

- As mentioned previously, we also think Chile’s producers face more competition and lower copper prices as production restarts later this year in Malaysia. That could send copper to $11k/MT.

- While the external environment (including a softer $) can help EM this year, we think copper could send USD/CLP to 950 in late 2026

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Bundle

17 April

FX Talking: A trip down the de-escalator

- This bundle contains 6 Articles