Korean won: The benefits of deliverability

Korean officials are planning to open up the Korean won onshore market to Registered Foreign Institutions and extend trading hours. We see this benefiting bid/ask spreads, risk management, and corporate liquidity programmes. These benefits could be with global financial institutions and corporates as early as the second half of 2024

The motives

In a press release earlier this year, Korean officials pointed to the need to correct Korea’s restrictive FX market structure in order to improve the attractiveness of KRW-denominated assets and quicken the overall development of the capital market and financial industry. Many believe that one of the key goals of improving FX accessibility to Korea’s markets is to achieve high-profile inclusions into developed market benchmark indices such as the WGBI bond index and MSCI’s Developed Market equity index.

While acknowledging that improving market access to Korea’s FX market is a necessary but not sufficient condition for entering these indices – for example, another condition for Korea’s inclusion into the WGBI index is that Korean Treasury Bonds (KTBs) be euroclearable – Korean authorities presumably have eyes on the prize of a re-rating of local securities. For example, some regional benchmarks show Korean equities trading at some of the lowest book values in the region – e.g. at sub 1.00 versus levels of around 1.40 for China and Singapore.

Some estimates put potential WGBI-related inflows into KTBs as high as $50bn

And, of course, inclusion into major bond indices can attract huge inflows and help government financing efforts. We assume that if included, Korean Treasury Bonds would join with a WGBI weighting of around 2- 2.5%. Some estimates put WGBI-related inflows into KTBs as high as $50bn. Index inclusion would also attract more long-term investors with the expected benefit of lower KRW volatility.

On the subject of index inclusion, we think WGBI inclusion is likely to happen earlier than MSCI inclusion (a short-selling ban needs to be addressed here) and that the Korean government would no doubt welcome any announcement on WGBI inclusion before the national elections next April.

Looking at this topic from a more macro level, Korea is classified as an advanced economy by the IMF and is suitable for advanced economy classification in terms of per capita GDP, its considerable degree of industrialisation, its various export bases, and its financial sector integration into the global financial system. However, in financial markets, most Korean capital products are classified as emerging markets.

Up until recently, Korea has taken advantage of its open economy to sustain high growth rates, but at the same time, Korean financial markets have been quite sensitive and volatile to external shocks. As a result, government control and monitoring of capital and financial markets has naturally become relatively tight. Also, the experience of the Asian financial crisis in 1997 hampered the structural reforms needed to develop domestic financial markets further.

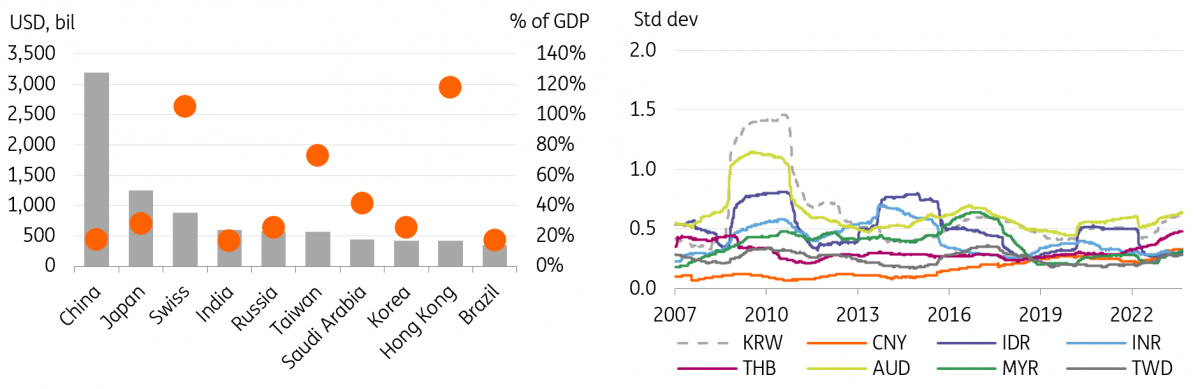

FX reserves for selected countries and historical volatility readings for Asian FX pairs

Looking more closely at the FX market, Korea has seen value in accumulating sizable FX reserves to provide protection against financial turmoil. However, the government has accelerated efforts over the past few years to adopt a more market-friendly approach and to lift restrictive policy measures.

These have improved the efficiency of the capital market along with Korea’s international investment position, which has shifted from a net debtor to a net creditor position amid growing concerns over a rapidly ageing population.

The challenge for Korea is that right after the Asian financial crisis its merchandise surplus drove the current account surplus, but ageing is a potential cause of the decrease in savings and the current account surplus. Given that Korea has been experiencing one of the fastest demographic changes, there is a possibility that the current account balance will turn into a deficit in the near future. It thus becomes more important for policymakers to establish a virtuous circle of a current account surplus and net foreign asset accumulation, which is one of the major motives behind the ongoing FX market reform efforts.

The reforms

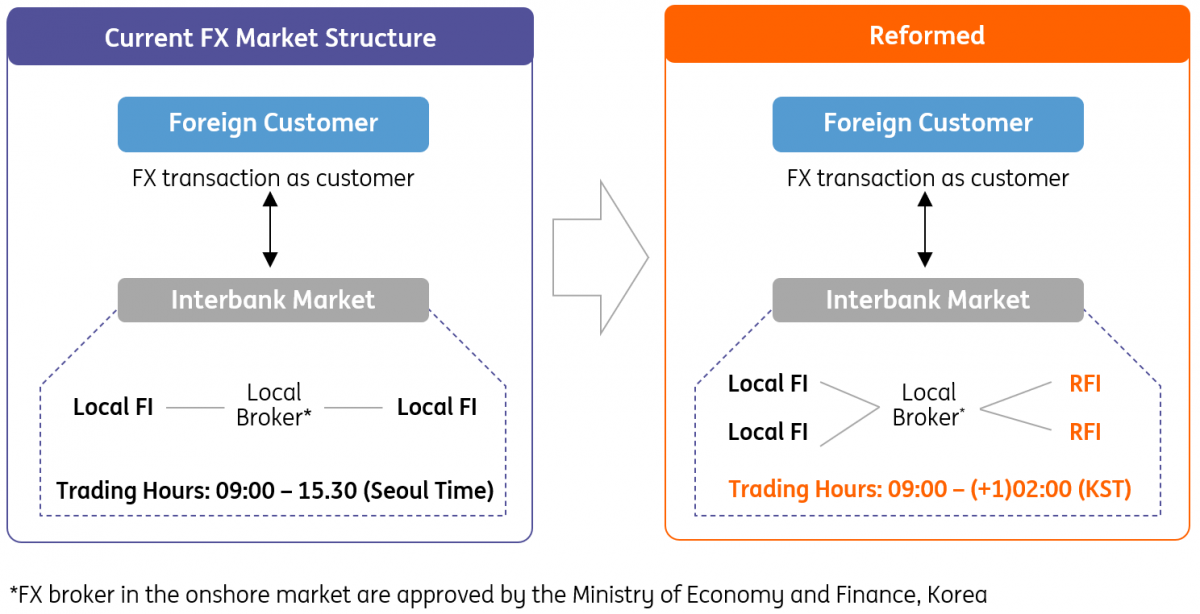

- Starting with a pilot in early 2024, the largest of the proposed FX reforms is to open up the onshore interbank FX market to Registered Foreign Institutions (RFIs). Currently, the onshore KRW market is only open to local institutions based onshore in Korea. These local institutions can also access the offshore Non-Deliverable Forward market. This means that, unlike the curves in Malaysia, the onshore and offshore KRW forward curves trade very close to each other. The biggest benefit here, however, is that RFIs could quote deliverable KRW forwards to their offshore customers and then clear those with an approved local broker in Korea.

- The next biggest reform is the extension of FX trading hours. The current onshore trading hours of 0900-1530 KST will be extended to 0200 KST - a couple of hours after the London close. We hear that local Korean banks in Seoul are preparing to run night shifts to meet this need.

- Further proposals centre on the development of market infrastructure in line with global FX markets (aggregators, third-party settlement), plus administrative measures for the new relationships between RFIs and locals and adjustments to the regulatory system.

Structural reforms of Korea’s FX market

The won’s FX peer group

Before looking at the benefits of these proposed reforms, perhaps we should be asking what success would look like. For example, the Korean won already sees the largest NDF trading volumes in London, but as a deliverable currency, what should it be aiming for?

Daily trading volume by FX product and average daily trading volume (US$m of NDF mkt in London)

If developed market status is the ambition, then the APAC members of the MSCI Developed Market index are Australia, Hong Kong, Japan, New Zealand and Singapore. Korea is roughly a similar-sized economy to Australia, while its economy is around three times larger than Singapore. Yet, Asian countries are quite heterogeneous in terms of economic structure, trade dependence, and capital market size, although they are all quite dependent on trade with China.

If we narrow our focus more to the FX trading side, we can see from Bank of International Settlement (BIS) data that the average daily trading volumes for all KRW FX instruments (spot, FX swaps, outright forwards, and options) was $142bn per day in 2022. Korea could well be setting its sights on the sort of total FX volumes being enjoyed by Singapore ($182bn) or Hong Kong ($193bn). For reference, CNY daily FX volumes were $526bn in 2022.

The benefits

The first obvious benefit of these reforms would be the expected narrowing in bid/offer spreads. We see two paths here. The first is that the extension of onshore KRW trading hours should reduce the illiquidity premia currently embedded in the out-of-hours bid/offer spread. The second path is higher trading volumes driving USD/KRW bid-offer spreads narrower towards those potential targets such as USD/SGD, USD/HKD, or even USD/CNH.

In the chart below, we look at the average bid/offer spreads to mid-price for selected pairs between 2 June and 23 August. The data has kindly been provided by ING’s eFX team. The two standouts here: USD/KRW bid/offer spreads are nearly double when the onshore market is closed and USD/KRW onshore spreads are around 11 times wider than for the likes of USD/SGD, USD/HKD, and USD/CNH. Clearly, there is plenty of room for narrower spreads here.

Average bid-offer spread to mid-price of USD/KRW and selected Asian pairs

1m KRW NDF Asia hours spread = 100

The second benefit involves the risk management of positions. Currently, offshore entities are hedging exposure to the KRW by using the NDF market. This is cash-settled, usually in dollars, against an official NDF fixing provided by local authorities. Presumably, the liquidity of using a more widely traded FX-swap market to hedge positions will reduce slippage. There have also been extreme cases in Argentina and Ukraine where the local NDF fixings have failed to reflect market developments – effectively undermining the NDF contract as a hedging product.

Other potential benefits for multinationals include the hedging of KRW at the global, not local level and also cash pooling

Also under the potential benefits of risk management, we would put the topic of global corporates being better able to hedge KRW at the central treasury rather than at the local level. For example, KRW being non-deliverable, central corporate treasuries may be invoicing the local Korean treasury centre in USD, leaving the local Korean treasury to manage the FX risk of KRW receivables against USD payables. The move to deliverability would allow the central treasury to switch to KRW invoicing and manage the KRW risk at the central treasury as part of a more coordinated and value-adding hedging programme.

And finally, we should discuss the benefits from a cash management perspective. The deliverability of the KRW would allow surplus KRW funds to be swept into regional cash management pools to lower overall borrowing costs. Solutions to KRW funding deficits could also be examined from a global and not just a local perspective. And the reforms in theory should allow more flexible repatriation of KRW dividends, where the current market structure means that some corporates can only remove dividends once per year.

The 'long journey'

Most corporates we spoke to tended to talk of the ‘long journey’ of ‘going onshore’. And it certainly looks like Korean authorities are pursuing an ambitious timeline of a six-month pilot at the start of 2024, with the aim for these reforms to be fully implemented by the summer of 2024 at the earliest. Whether Korean authorities are prepared to unwind their ‘closed and restrictive FX structure’ (their words) remains to be seen. If not, the new deliverable KRW market may not gradually absorb all of the NDF market as intended and Korea could be left with its two-tier market.

Yet, as we outline above the benefits are plentiful and there are many incentives for all parties to make these reforms work.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article